The North American Deep Value Week – 2026/07

Reports, Dividends & Major Shareholder Notifications

Companies mentioned:

· Natural Alternatives International, Inc. – Q2 FY2026 Results and Full-Year Loss Expected

· The Manitowoc Company – Q4/FY2025 results and FY2026 guidance issued

· Hooker Furnishings – Donald Smith & Co increases stake to 9.9%

· LGI Homes – Q4/FY2025 Results and 2026 Outlook

· Tronox Holdings – Board Change and $0.05 Quarterly Dividend Declared

· Century Communities – Robert J. Francescon Files Amended 13G Reporting 6.5% Stake

· Century Communities – Dale Francescon Files Amended 13G Reporting 7.5% Stake

· AdvanSix – Victory Capital Files Amended 13G Reporting a Decrease to 0.51%

· Mercer International – Q4/FY2025 Results, Large Impairments and Near-Term Market Outlook

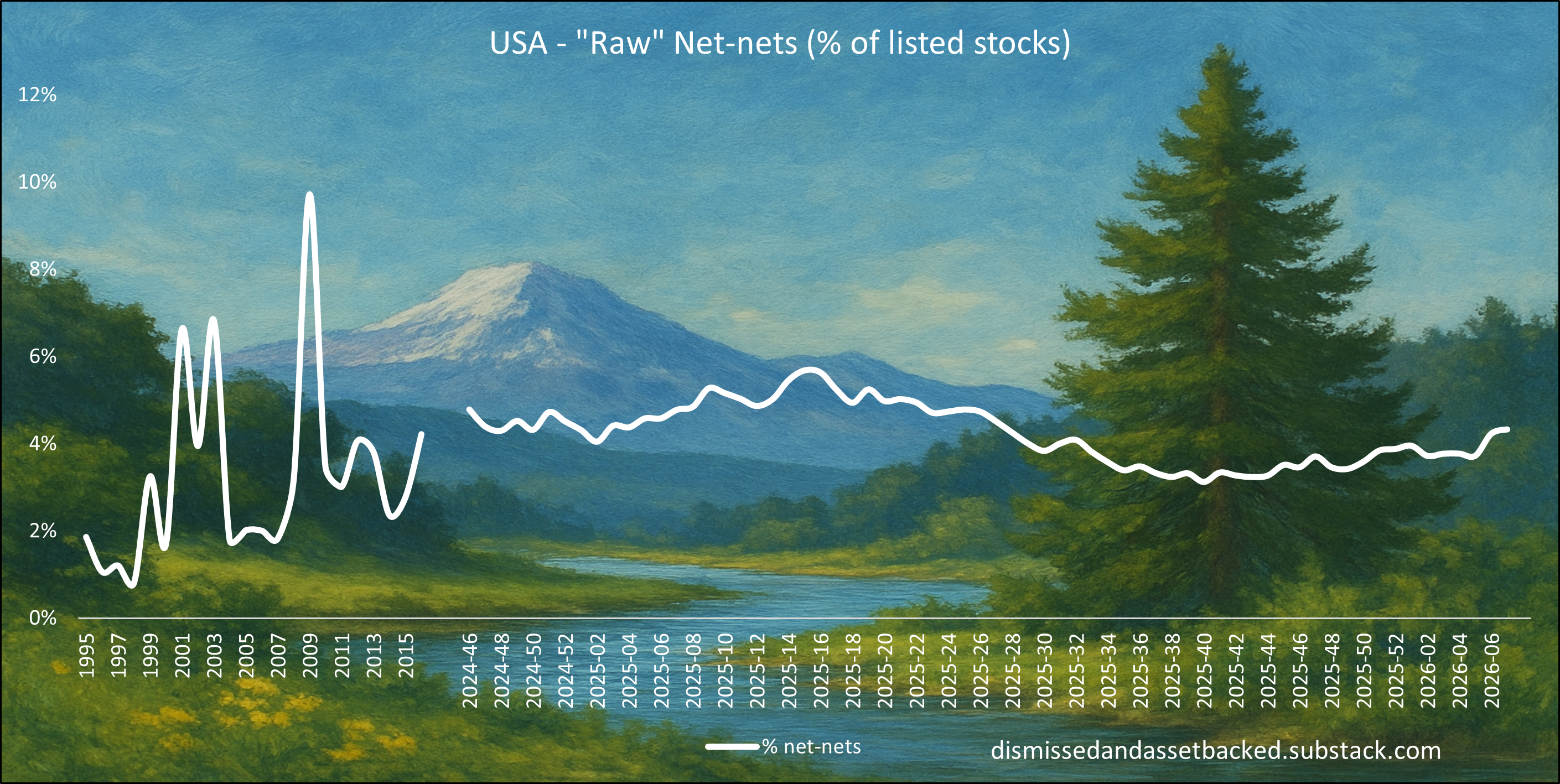

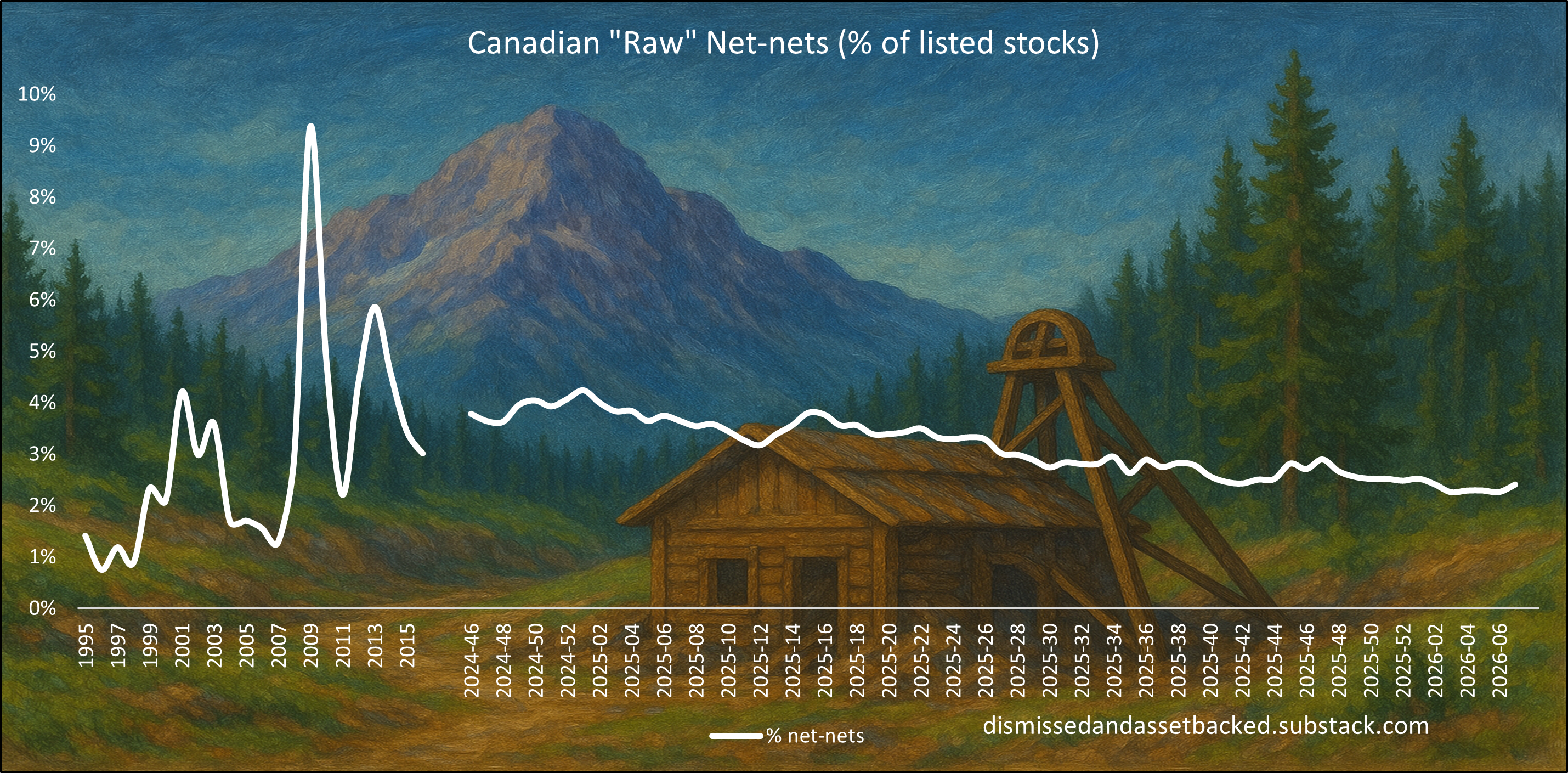

“Graham’s Geiger counter”

Benjamin Graham suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive. Today’s net-nets, however, are not the same as Graham’s net-nets. Many are un-investable being Chinese RTO’s, loss-making biopharma’s etc. But we do think it is interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable.

Natural Alternatives International, Inc. – Q2 FY2026 Results and Full-Year Loss Expected

2026-02-13 │ P/TB 0.31 │ URL

February 13, 2026 – Natural Alternatives International, Inc. reported a net loss of $2.6m ($0.42 per diluted share) for Q2 FY2026 on net sales of $34.8m, up 2% y/y, compared with a net loss of $2.2m in the prior-year quarter. Growth was driven by a 2% increase in private-label contract manufacturing sales to $32.8m, reflecting higher orders from existing and new customers, while CarnoSyn® beta-alanine royalty, licensing and raw material revenue rose 13% to $2.0m, mainly due to increased raw material orders. Gross margin improved to 7.2% (4.9%), supported by better factory utilization, and SG&A declined slightly, narrowing operating losses. For the first six months of FY2026, net sales increased 8% to $72.5m, with private-label sales up 9% to $68.9m, while CarnoSyn® revenue declined 15% to $3.7m; net loss improved to $2.8m from $4.2m a year earlier. Cash totaled $3.8m at December 31, 2025 (June 30, 2025: $12.3m), with $5.8m drawn on the credit facility and $10.0m available capacity. Despite revenue growth and improved margins, management cited underutilized factory capacity and weaker demand visibility among multi-level marketing and direct selling customers in China, Europe and parts of North America. The company expects sales to increase in the remaining two quarters versus both the prior year and H1, but now anticipates a net loss in H2 FY2026 and for the full fiscal year due to reduced customer forecasts and delayed product launches.

The Manitowoc Company – Q4/FY2025 results and FY2026 guidance issued

2026-02-10 │ P/TB 1.03 │ URL

February 10, 2026 – The Manitowoc Company reported Q4 2025 net income of $7.0m ($0.19 diluted EPS) and adjusted net income of $9.5m ($0.26), on net sales of $677.1m (+13.6% y/y), with non-new machine sales of $190.9m (+14.0%) and adjusted EBITDA of $39.6m (+13.5%). Orders surged to $803.4m (+55.8% y/y), lifting backlog to $793.5m (+22.0% y/y). For full-year 2025, net sales rose 2.9% to $2,240.9m, non-new machine sales increased 9.8% to $690.5m, and adjusted EBITDA was $121.7m (vs $128.4m), while operating cash flow in Q4 was $91.1m and free cash flow was $78.3m (FY free cash flow: -$15.3m). Management highlighted a strong finish to a challenging year and continued execution on its CRANES+50 strategy, including expanding non-new machine sales and ongoing lean initiatives. Looking ahead, the company guided FY2026 net sales to $2.25bn–$2.35bn, adjusted EBITDA to $125m–$150m, adjusted diluted EPS to $0.45–$0.90, and free cash flow to $40m–$65m, and noted a January restructuring intended to deliver ~$10m in annualized savings during 2026, while flagging steady U.S. conditions but improving optimism in Europe and planned new locations in Chile, Mexico, France and Portugal.'

Hooker Furnishings – Donald Smith & Co increases stake to 9.9%

2026-02-11 │ P/TB 1.04 │ URL

February 11, 2026 – Hooker Furnishings Corp disclosed via a Schedule 13G filing that Donald Smith & Co., Inc. (together with DSCO Value Fund, L.P. and John Piermont) beneficially owned 1,066,754 common shares, representing 9.9% of the company’s outstanding class, based on ownership as of December 31, 2025. The filing reports sole voting power over 1,009,496 shares for Donald Smith & Co., with smaller positions attributed to DSCO Value Fund (9,858) and John Piermont (2,000), and sole dispositive power totaling 1,054,896 shares for Donald Smith & Co. (plus 9,858 and 2,000 respectively), with no shared voting or dispositive power reported. The stake is reported under Rule 13d-1(b) as an investment adviser filing, and the filer certified the shares were acquired and are held in the ordinary course of business without intent to influence or change control of the issuer.

LGI Homes – Q4/FY2025 Results and 2026 Outlook

2026-02-17 │ P/TB 0.68 │ URL

February 17, 2026 – LGI Homes, Inc. reported Q4 2025 home sales revenues of $474.0m on 1,301 closings (1,362 total including leased homes), with an average sales price of $364,310 and gross margin of 17.7% (adjusted gross margin 22.3%). Net income was $17.3m ($0.75 diluted EPS), while adjusted net income was $22.4m ($0.97 adjusted diluted EPS). For full-year 2025, home sales revenues were $1.71bn on 4,685 closings (4,788 total), with an average sales price of $364,035 and gross margin of 20.7% (adjusted 24.0%); net income totaled $72.6m ($3.12 diluted EPS) versus $196.1m in 2024. Ending backlog increased to 1,394 homes valued at $501.3m (vs 599 homes/$236.5m), supported in part by a 480-home wholesale agreement for 2026 delivery, while total owned and controlled lots reached 60,842 and active selling communities stood at 144. Liquidity at year-end was $334.8m, including $61.2m cash, with net debt to capital of 43.2%. For 2026, management guided to 4,600–5,400 home closings, an average sales price of $355,000–$365,000, gross margin of 18.0%–20.0% (adjusted 21.0%–23.0%), SG&A at 15.0%–16.0% of revenues, an effective tax rate of ~26.5%, and 150–160 active communities by year-end, assuming market conditions remain broadly consistent with those seen to date in 2026.

Tronox Holdings – Board Change and $0.05 Quarterly Dividend Declared

2026-02-11 │ P/TB 0.93 │ URL

February 11, 2026 – Tronox Holdings plc filed a Form 8-K reporting that board member Lucrece Foufopoulos-De Ridder will not seek re-election at the company’s 2026 annual meeting due to time commitments related to other public company directorships, with the company noting no disagreement regarding operations, policies, or practices. Separately, the board declared a quarterly cash dividend of $0.05 per share, payable April 2, 2026, to shareholders of record as of February 23, 2026.

Century Communities – Robert J. Francescon Files Amended 13G Reporting 6.5% Stake

2026-02-13 │ P/TB 0.85 │ URL

February 13, 2026 – Century Communities, Inc. disclosed via an amended Schedule 13G (Amendment No. 9) that Robert J. Francescon beneficially owned 1,903,983 shares of common stock, representing 6.5% of the outstanding class, based on holdings as of December 31, 2025. The filing reports sole voting and dispositive power over all 1,903,983 shares and notes the position includes shares held directly and through affiliated entities and accounts, including RJF Century, LLC and the Nicholas R. Francescon 2020 Trust, as well as 190,056 shares issued on February 4, 2026 following the vesting and settlement of performance share units tied to a three-year cumulative adjusted pre-tax income target (2023–2025) plus 7,717 shares from related dividend equivalent rights. The amendment is filed under Rule 13d-1(d) and is described as ordinary ownership reporting rather than a control-oriented filing.

Century Communities – Dale Francescon Files Amended 13G Reporting 7.5% Stake

2026-02-13 │ P/TB 0.85 │ URL

February 13, 2026 – Century Communities, Inc. disclosed via an amended Schedule 13G (Amendment No. 9) that Dale Francescon beneficially owned 2,201,957 shares of common stock, representing 7.5% of the outstanding class as of December 31, 2025. The filing reports sole voting and dispositive power over 2,170,957 shares and shared voting and dispositive power over 31,000 shares held by the DCF Family Foundation. The holdings include shares owned directly and through affiliated entities and trusts, including DF Century, LLC and the James R. Francescon 2020 Trust, as well as 190,056 shares issued on February 4, 2026 upon vesting of performance share units tied to a three-year cumulative adjusted pre-tax income target (2023–2025) and 7,717 shares from related dividend equivalent rights. The amendment was filed under Rule 13d-1(d) and reflects beneficial ownership reporting rather than an activist or control-related filing.

AdvanSix – Victory Capital Files Amended 13G Reporting a Decrease to 0.51%

2026-02-11 │ P/TB 0.69 │ URL

February 11, 2026 – AdvanSix Inc disclosed via an amended Schedule 13G (Amendment No. 2) that Victory Capital Management, Inc. beneficially owned 137,620 shares of common stock as of September 30, 2025, representing 0.51% of the outstanding class. The filing reports sole voting power over 124,958 shares and sole dispositive power over 137,620 shares, with no shared voting or dispositive power. The amendment was filed under Rule 13d-1(b) by the investment adviser and includes a certification that the shares were acquired and are held in the ordinary course of business and not for the purpose of influencing or changing control of the issuer.

Mercer International – Q4/FY2025 Results, Large Impairments and Near-Term Market Outlook

2026-02-12 │ URL

February 12, 2026 – Mercer International Inc. filed an 8-K furnishing its Q4 and full-year 2025 earnings release, reporting Q4 2025 Operating EBITDA of -$20.1m versus $99.2m a year earlier, with a net loss of $308.7m (-$4.61/sh), driven by $238.7m of non-cash impairments primarily related to the Peace River mill (long-lived assets) and pulp inventory, reflecting the down-cycle in hardwood pulp pricing and high fiber costs. Q4 revenues declined 8% y/y to $449.5m, while full-year 2025 revenues fell 9% to $1,868.1m and Operating EBITDA moved to -$22.0m from $243.7m in 2024; FY net loss widened to $497.9m versus a net loss of $85.1m in 2024. Management highlighted progress in its “One Goal One Hundred” program, citing roughly $30.0m of cost savings and operational efficiencies achieved in 2025 toward a $100m target by end-2026, and noted that operating cash flow improved sequentially in Q4. Liquidity at December 31, 2025 was ~$430.4m, including $186.8m cash and ~$243.6m available under revolving credit facilities, while total shareholders’ equity fell to $68.1m from $429.8m at year-end 2024. Looking ahead, the company said it currently expects pulp prices to modestly increase across its markets in Q1 2026 on stable demand and global supply constraints, and also expects U.S. and European lumber prices to modestly increase in Q1 2026, while flagging rising near-term fiber costs due to supply constraints.

The writer may own shares of the companies mentioned. This communication is for informational purposes only. AI helped us with this. Check important info.