The European Deep Value Week – 2026/10

Companies mentioned:

· HERIGE – FY2025 Revenue Declines 5.9% Amid Weak Construction Market

· Cogra – Strong H1 2025/26 Recovery as Pellet Sales and Profitability Rebound

· DATRON AG – Related Party Purchase Shares in Directors’ Dealing

· Arbonia – Revenue and Adjusted EBITDA Grow in 2025; Board Proposes New Chairman

· Iberpapel – Board Proposes €0.86 per Share Total Shareholder Remuneration for 2025

· Nabaltec – 2025 EBIT Guidance Achieved Despite Revenue Decline; Sees Growth Returning in 2026

· Headlam – Appoints Rob Barclay as CEO Designate and Richard Jones as Interim CFO

· IG Design Group – UK Court Approves Capital Reduction

· IG Design Group – Octopus Investments Reduces Stake to 7.99%

· Robinson – Underlying Profit Improves in 2025; 2026 PBT to Benefit from Property Disposals

· Duell – CEO Magnus Miemois Steps Down, Interim CEO Appointed

· Energy Save – Delivers First Heat Pump Order to Saudi Arabia

· Hydrotor – Fire at Subsidiary Paint Shop May Cause PLN 2.5m Revenue Loss

· Remak-Energomontaż – Reports Preliminary FY2025 Net Loss on Lower Revenue

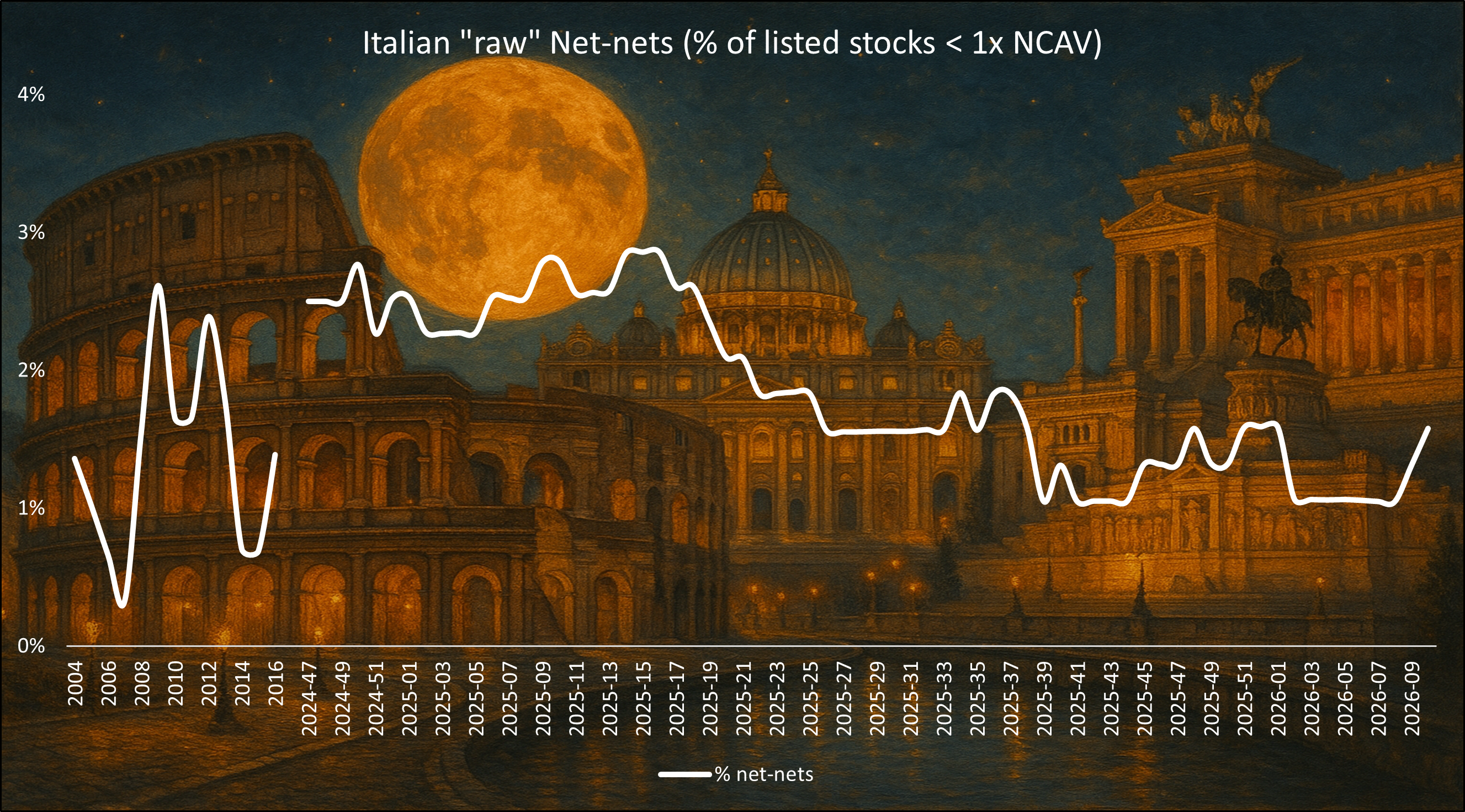

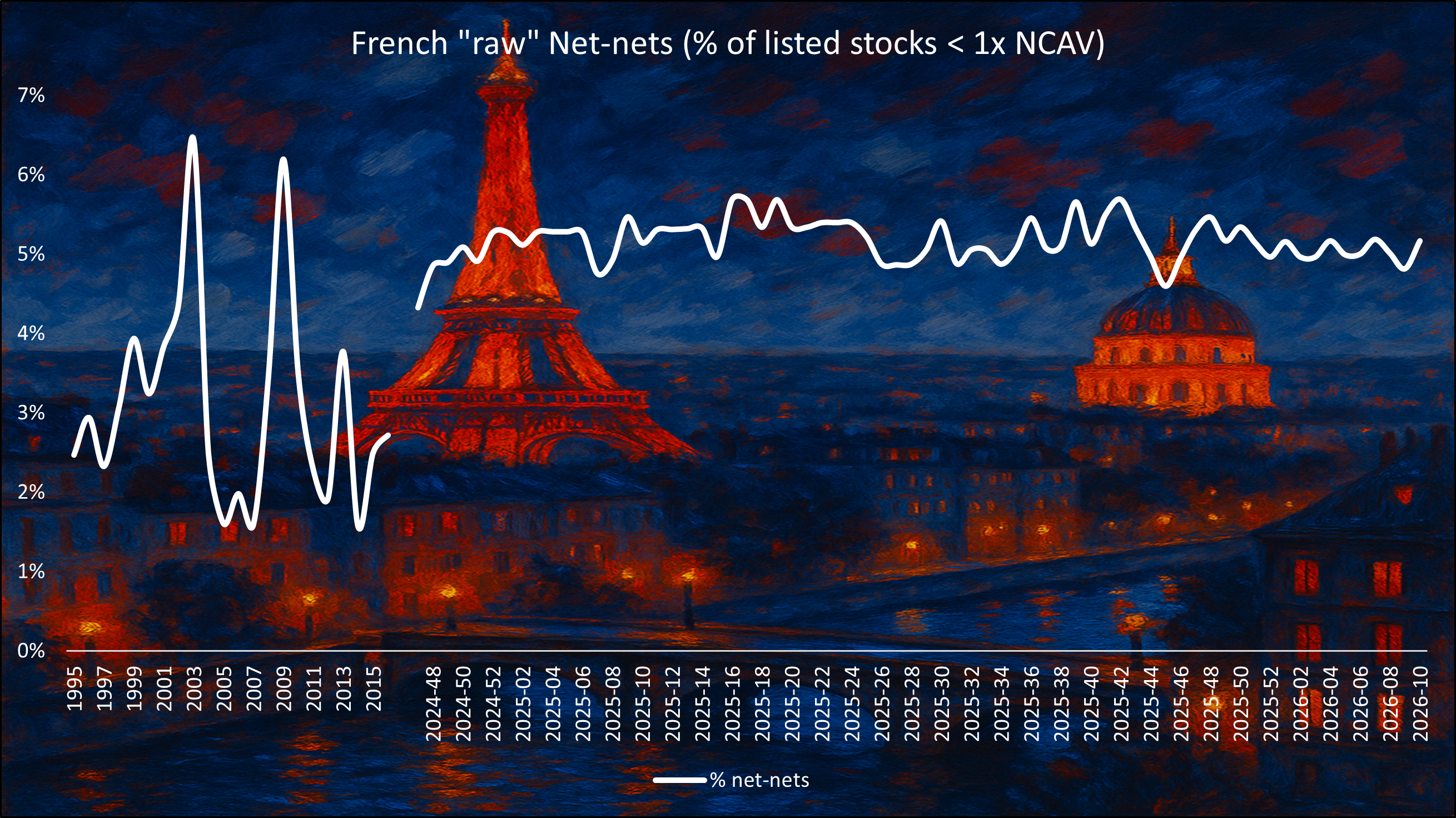

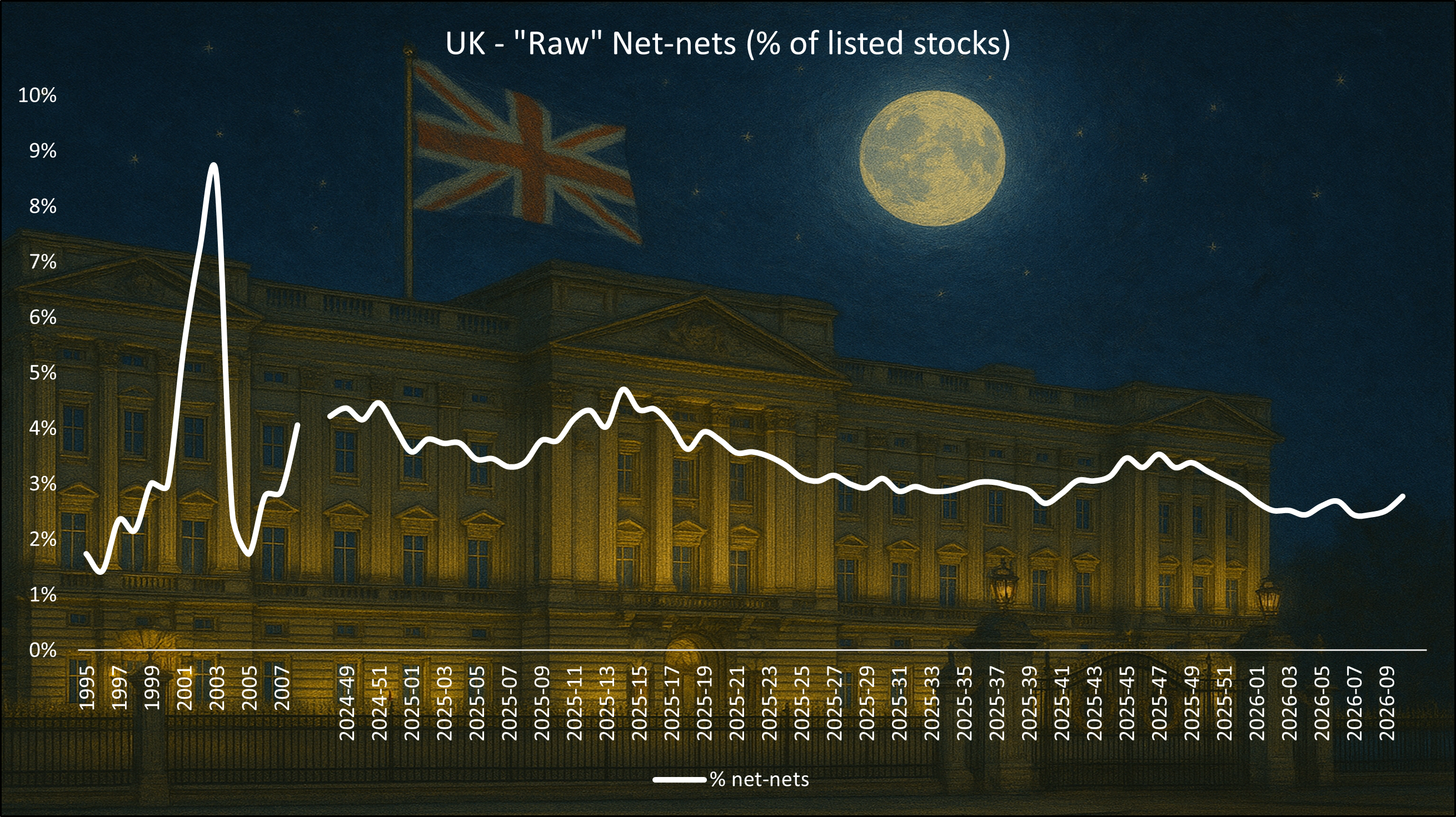

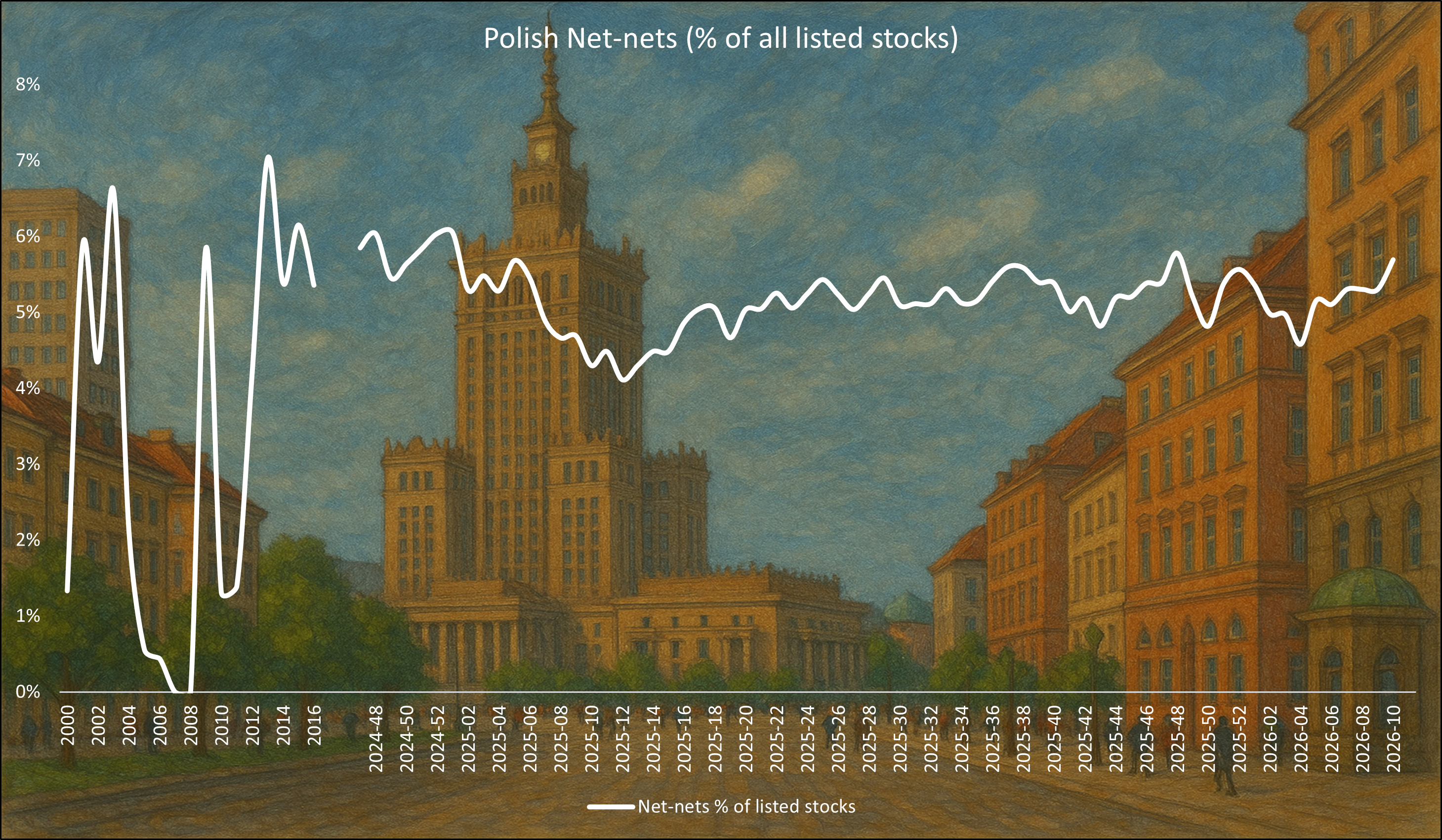

“Graham’s Geiger counter”

Benjamin Graham suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive. Today’s net-nets, however, are not the same as Graham’s net-nets. Many are un-investable being Chinese RTO’s, loss-making biopharma’s etc. But we do think it is interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable.

HERIGE – FY2025 Revenue Declines 5.9% Amid Weak Construction Market

2026-02-03 │ P/TB 0.57 │ URL

3 February 2026 – HERIGE reported FY2025 revenue of €379.4m, down 5.9% year-on-year (€403.2m in 2024), reflecting continued weakness in construction markets but with relatively resilient performance. Q4 revenue amounted to €96.2m, declining 2.4% year-on-year, though benefiting from a favorable calendar effect (-6.9% on a comparable-day basis). The Industrial Joinery division generated €219.2m in revenue for the year (-7.0%), with activity affected by uncertainty around renovation support schemes despite relatively better trends in installer networks and construction-site projects. The Concrete Industry division showed greater resilience, with FY revenue of €132.8m (-1.8%), supported by ready-mix and precast segments, a favorable product mix, and growth in specialty and lower-carbon concrete products. Overall, the group noted that market conditions remained fragile throughout 2025 but that activity demonstrated solid resilience given limited visibility in the sector. Looking ahead, management said short-term visibility remains constrained due to political and regulatory uncertainty and the sector’s reliance on stable policy measures supporting energy renovation and regulatory simplification. HERIGE will continue focusing on operational performance initiatives while positioning itself to benefit from a gradual recovery in the construction market.

Cogra – Strong H1 2025/26 Recovery as Pellet Sales and Profitability Rebound

2026-03 │ P/TB 1.20 │ URL

Cogra reported a strong recovery in H1 2025/26, with revenue rising 21% year-on-year to €22.6m as the group moved beyond the energy-market disruption of the prior two years and benefited from a normalized market environment. Pellet sales increased 20% to €19.9m, stove and boiler sales rose 13% to €2.4m, and services grew 36%, while the company continued its inventory reduction program, with negative inventory production of €2.9m, alongside adjustments to sourcing and industrial capacity through the heating season. Improved operating discipline and cost control drove EBITDA to €2.6m, equivalent to an 11.5% margin, versus -€0.3m a year earlier, while operating profit reached €1.1m and net profit also came in at €1.1m, equal to a 4.8% net margin. The balance sheet also improved materially, with inventories down to €8.2m from €12.5m a year earlier, cash up to €4.5m from €2.6m, financial debt down 25% year-on-year to €6.5m, and gearing reduced to 9% from 25%. Management also highlighted the appointment of François Chapon as CEO from 1 January 2025 and disclosed that TEXI SAS increased its stake to 29.75% of the capital in November 2025. Looking ahead, the company said FY2025/26 started on a healthier footing, supported by stabilized pricing, rising pellet volumes, normalized inventory levels and continued deleveraging. Cogra expects the more favorable pricing environment, better industrial utilization and a controlled cost base to support a marked recovery in operating performance and a return to profitable growth and sustainable value creation in 2025/26.

DATRON AG – Related Party Purchase Shares in Directors’ Dealing

2026-03-03 │ P/TB 0.69 │ URL

3 March 2026 – DATRON AG disclosed a directors’ dealing notification stating that PCI Private Capital Investment GmbH, a party closely associated with Management Board member Michael Daniel, purchased DATRON shares on 2 March 2026. The transaction was executed on Xetra at a price of €7.40 per share, with two individual purchases amounting to a combined volume of €29.6k.

Arbonia – Revenue and Adjusted EBITDA Grow in 2025; Board Proposes New Chairman

2026-03-03 │ P/TB 0.81 │ URL

3 March 2026 – Arbonia reported FY25 revenue of CHF 624.5m, up 12.3% YoY, with organic growth of 3.7% driven by the wood segment (+6.1%) while glass declined (-4.0%) amid continued weak residential construction activity in several core markets. Adjusted EBITDA increased to CHF 57.3m, representing a 9.2% margin and a 15% operational increase versus the prior year, supported by price adjustments, slightly higher volumes and efficiency gains in production and processes, partly offset by wage inflation, structural cost pressures and negative FX effects. Reported EBITDA was CHF 56.3m compared with CHF 66.3m in 2024, which had benefited from one-off gains from a property sale, while EBIT amounted to CHF –2.4m and adjusted EBIT reached CHF 2.8m.

The company continued its strategic focus on the doors business, achieving sequential EBITDA improvement throughout the year. Net debt declined significantly to CHF 149m from CHF 357m following the sale of the Climate division, which also drove free cash flow to CHF 605m. Arbonia is progressing with further portfolio streamlining, including the expected closing of the sale of its Russian radiator activities by end-March 2026 and ongoing negotiations to divest the Polish roof-window business Skyfens. The board also proposed Christoph Ganz, currently a senior executive at Sika, as the new chairman to succeed Alexander von Witzleben at the April 2026 AGM.

Looking ahead, Arbonia expects a challenging market environment in 2026, particularly in Germany, though early signs of recovery are emerging as building permits increase and investment sentiment improves. For 2026, the company guides for revenue growth of 3–5% and adjusted EBITDA growth of 15–20%, alongside free cash flow of CHF 15–20m, assuming stable exchange rates and normal material cost development.

Iberpapel – Board Proposes €0.86 per Share Total Shareholder Remuneration for 2025

2026-03-02 │ P/TB 0.67 │ URL

2 March 2026 – Iberpapel announced that its board has approved the financial statements for FY2025, reporting net profit of €6.06m, and will propose total shareholder remuneration of €0.86 per share from 2025 earnings. The proposal includes a final dividend of €0.18 per share to be submitted for approval at the upcoming AGM, in addition to the interim dividend of €0.43 per share paid in December 2025 and a planned €0.25 per share distribution from the share premium account. If approved by shareholders, the combined payout would correspond to a dividend yield of approximately 4.3% based on the year-end share price. The proposed distributions remain subject to approval at the AGM, which has not yet been formally convened.

Nabaltec – 2025 EBIT Guidance Achieved Despite Revenue Decline; Sees Growth Returning in 2026

2026-03-05 │ P/TB 0.62 │ URL

5 March 2026 – Nabaltec reported preliminary FY25 revenue of €197m, down 3.2% from €203.6m in 2024, reflecting weak demand in the refractory and e-mobility markets as well as market uncertainty linked to U.S. tariff policy, with Q4 revenue falling 7.7% year-on-year to €41.9m due to short-term order cancellations and particularly weak December activity. The Functional Fillers segment generated €144.1m in revenue (-2.7%), while Specialty Aluminas declined 4.7% to €53.0m. EBIT amounted to €15.2m compared with €22.3m in the prior year, corresponding to an EBIT margin of 7.7%, which remained within the company’s guidance range of 7–9%. Management noted that despite the volatile market environment the company achieved its earnings forecast, highlighting the resilience of its business model. For 2026, Nabaltec expects revenue growth of 4–6% and an EBIT margin of 5–7%, with the lower margin primarily reflecting higher material costs and increased depreciation and amortization, while geopolitical risks, including tensions in the Middle East, could add further uncertainty to the outlook.

Headlam – Appoints Rob Barclay as CEO Designate and Richard Jones as Interim CFO

2026-03-03 │ P/TB 0.24 │ URL

3 March 2026 – Headlam Group announced two senior executive appointments as part of its leadership transition. Rob Barclay will join the board as Chief Executive Officer designate on 9 March 2026 and will assume the full CEO role on 27 April 2026, when Stephen Bird steps down from his interim executive position to resume his role as Non-Executive Chair. Barclay brings more than 25 years of experience in building products manufacturing and distribution, including senior roles at SIG plc, National Timber Group and most recently Batt Cables, with a background in transformation programs and operational improvement. In addition, Richard Jones will join the group as Interim Chief Financial Officer on 12 March 2026, succeeding Adam Phillips following a transition period. Jones previously served as Interim CFO at HSS Hire Group (now ProService Building Services Marketplace) and has held senior finance roles at Medica Group, Mereo Biopharma and Shield Therapeutics. The appointments are intended to strengthen leadership and support the next phase of Headlam’s strategic development and operational improvements.

IG Design Group – UK Court Approves Capital Reduction

2026-03-04 │ P/TB 0.66 │ URL

4 March 2026 – IG Design Group announced that the High Court of Justice of England and Wales approved the company’s capital reduction on 3 March 2026, enabling the cancellation of the Capital Reduction Shares as well as the share premium and capital redemption reserve. The court order and related statement of capital will now be filed with the Registrar of Companies, after which the capital reduction will become effective upon registration. The transaction will not change the number of ordinary shares in issue or their nominal value and will not affect shareholder rights. The capital reduction is intended to provide the company with greater flexibility to potentially make shareholder distributions in the future.

IG Design Group – Octopus Investments Reduces Stake to 7.99%

2026-06-06 │ P/TB 0.66 │ URL

6 March 2026 – IG Design Group disclosed a major holdings notification indicating that Octopus Investments Limited reduced its stake in the company to 7.99% of voting rights, equivalent to 7,852,065 shares. The threshold was crossed on 4 March 2026 and the company was notified on 5 March 2026. The position declined from a previously reported 8.99% stake, reflecting a disposal of voting rights. The holding is controlled through Octopus Capital Limited, which is the ultimate controlling entity. No financial instruments linked to voting rights were reported as part of the position.

Robinson – Underlying Profit Improves in 2025; 2026 PBT to Benefit from Property Disposals

2026-03-05 │ P/TB 0.83 │

5 March 2026 – Robinson reported FY2025 revenue of £56.2m, down 0.4% year-on-year, but delivered improved profitability with underlying operating profit rising to £3.6m from £3.2m and gross margin increasing to 22% from 20%. Performance was supported by strong volume growth in the UK plastics and paperbox businesses, improved operational efficiency and better material utilisation, partly offset by weaker demand, contract losses and ongoing challenges in Denmark and Poland. Reported profit before tax improved to £3.0m from a £3.8m loss in 2024, helped by the absence of large prior-year exceptional costs and supported by a small net gain from other items. Net debt declined to £5.4m from £5.9m, while the company generated £1.0m of cash proceeds from surplus property disposals and made further progress on additional sales. The board proposed an unchanged final dividend of 3.5p per share, taking the total dividend for 2025 to 6.0p. Looking ahead, Robinson said underlying operating profit in 2026 is expected to be in line with current market expectations, with growth in its UK businesses supported by known new customer projects, although Poland and Denmark are expected to remain challenging. The company also expects 2026 reported profit before tax to benefit materially from property disposals, while underlying operating profit is likely to be slightly below 2025 due to higher investment in capabilities and lower rental income.

Duell – CEO Magnus Miemois Steps Down, Interim CEO Appointed

2026-03-04 │ P/TB 0.44 │ URL

4 March 2026 – Duell announced that CEO Magnus Miemois will step down from his position following a mutual agreement with the board, ending a tenure that began in January 2024. The board has launched a recruitment process for a new chief executive and appointed Tomi Virtanen, currently a manager in Supply Chain Management, as interim CEO effective 5 March 2026. The announcement concerns a management change only and did not include any financial update, outlook or guidance.

Energy Save – Delivers First Heat Pump Order to Saudi Arabia

2026-03-04 │ P/TB 0.74 │ URL

4 March 2026 – ES Energy Save announced it has delivered a heat pump (ES M40 R290) controlled by its NordFlex system to a customer in Saudi Arabia as part of a test order to be installed in a firefighter equipment factory. The project marks the company’s first delivery to Saudi Arabia and will serve as a pilot phase after which the parties will evaluate potential further collaboration. Management highlighted growing interest in Energy Save’s commercial heat pump solutions from markets outside Europe, following a recent 500 kW project in Chile. The company noted that the order will have a limited impact on revenue and cash flow but is strategically important as it represents entry into a new geographic market.

Hydrotor – Fire at Subsidiary Paint Shop May Cause PLN 2.5m Revenue Loss

2026-03-02 │ P/TB 0.40 │ URL

2 March 2026 – Przedsiębiorstwo Hydrauliki Siłowej Hydrotor reported that a fire broke out on 27 February 2026 in the paint shop area of its subsidiary Agromet ZEHS Lubań in Lubań, Poland. The local fire brigade extinguished the fire and the company stated that the extent of the material damage is still difficult to estimate, though the facility is covered by insurance and a claim has been filed. Due to the temporary shutdown of the painting facility, expected to last around two weeks while repairs are completed, the company estimates lost revenue of approximately PLN 2.5m net. Hydrotor is working to mitigate the impact by cooperating with external providers of cylinder painting services and by seeking customer approval to deliver hydraulic cylinders without painting where possible.

Remak-Energomontaż – Reports Preliminary FY2025 Net Loss on Lower Revenue

2026-03-03 │ P/TB 0.53 │ URL

3 March 2026 – Remak-Energomontaż reported preliminary FY2025 financial results indicating revenue of PLN 177.0m and a net loss of PLN 10.8m. The figures represent a significant deterioration compared with 2024, when the company generated revenue of PLN 237.4m and net profit of PLN 5.0m, with operating profit turning negative at approximately PLN –9.5m. The company noted that the results are preliminary and may change when the audited annual report is released. In a separate annual report disclosure, the company confirmed the 2025 financial statements and detailed selected financial metrics, including total assets of PLN 177.3m and equity of PLN 64.4m at year-end. No outlook or guidance was provided in the announcement.

The writer may own shares of the companies mentioned. This communication is for informational purposes only. AI helped us with this. Check important info.