The European Deep Value Week – 2026/07

Reports, Analyst Ratings & TR1’s

Companies mentioned:

· DELFINGEN – FY2025 Revenue in Line; Margin Target Reaffirmed

· Bertrandt – Positive Q1 EBIT; Guidance Confirmed and Diversification Accelerates

· Bertrandt AG – Montega Reiterates Buy; €26 Target on Stabilization Signs

· Groupe Plastivaloire – Plans Transfer to Euronext Growth to Simplify Listing Framework

· POLYTEC Holding AG – Research Error Corrected; Guidance Reaffirmed

· SMT Scharf AG – MoUs in China for Battery Transport; Majority in Xinsha and Canada Exit

· Siltronic AG – 2026 Guidance Points to Lower Sales and Margin Pressure

· AIREA PLC – Newlands Increase Stake Above 15% Threshold

· IG Design Group plc – Trading Ahead of Expectations; Cash Stronger Than Forecast

· IG Design Group plc – Canaccord Genuity Reduces Stake to 11.05%

· Sanderson Design Group plc – FY2026 In Line; Profit and Cash Improve

· Severfield plc – Andrew Page Appointed CFO and Executive Director

· MJ Gleeson plc – H1 Robust but Cautious on FY Outturn; Guidance Update Due in April

· Ferronordic AB – Q4 Profitability Improved; FY Net Loss but Strong Operating Cash Flow

· Corem Property Group AB – Large Value Declines and Portfolio De-Risking via Disposals, Including US Exit Steps

· ES Energy Save Holding – CEO succession: Deputy CEO Yibo Zhao to become CEO at AGM; current CEO proposed as Executive Chair

· FASING – Orders from subsidiary Fasing America Corp. (USA)

· KPPD-Szczecinek – Preliminary 2025 Results Show Improved Profitability

· Relpol – Subsidiary Deleted from National Court Register

· Remak-Energomontaż – Selected as Most Advantageous Bidder for PLN 25.8m Turbine Contract

· Remak-Energomontaż – Signs Annex Increasing Contract Value to PLN 26.9m

· STALPROFIL – Extraordinary General Meeting Adopts Statute and Remuneration Policy Amendments

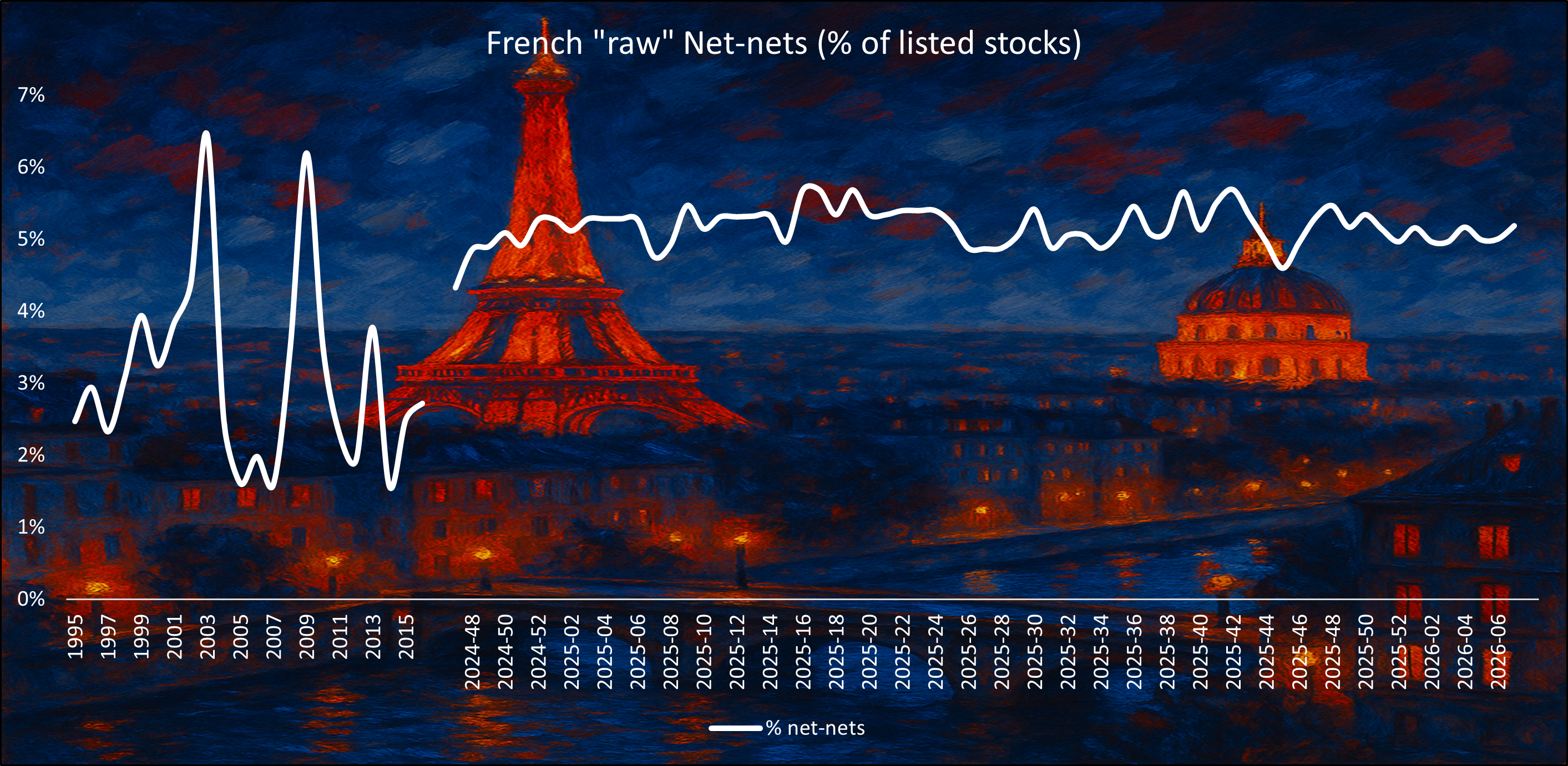

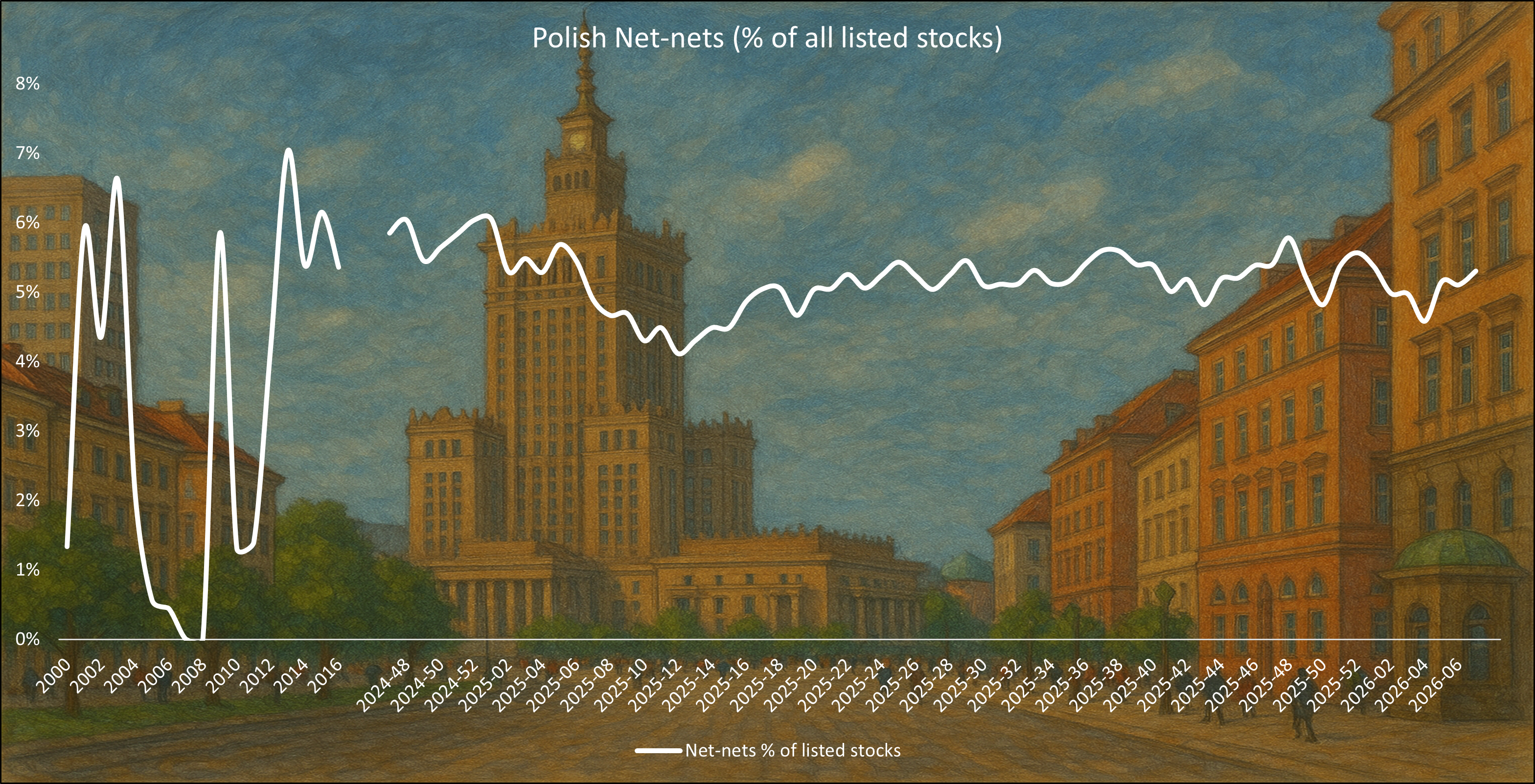

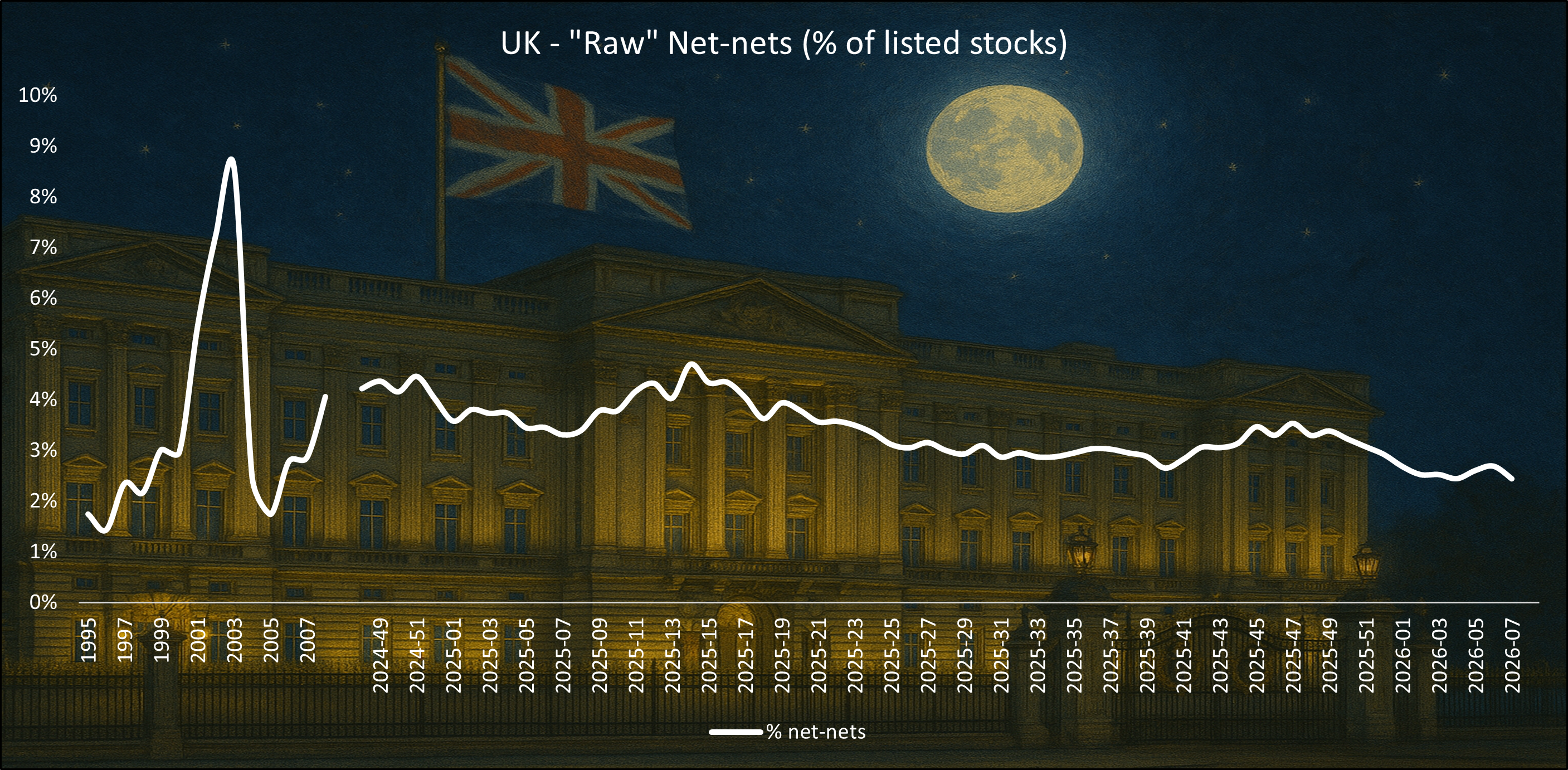

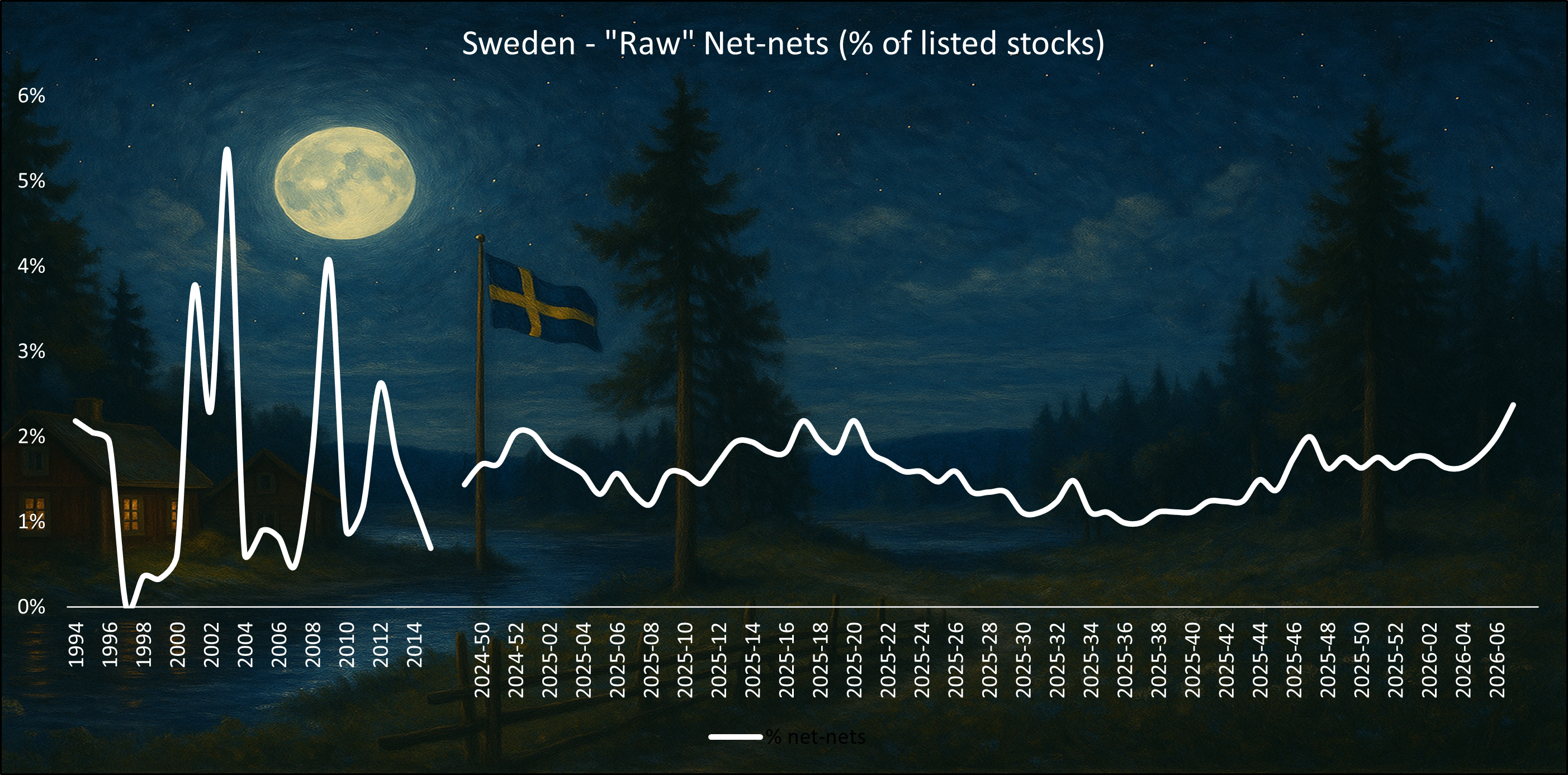

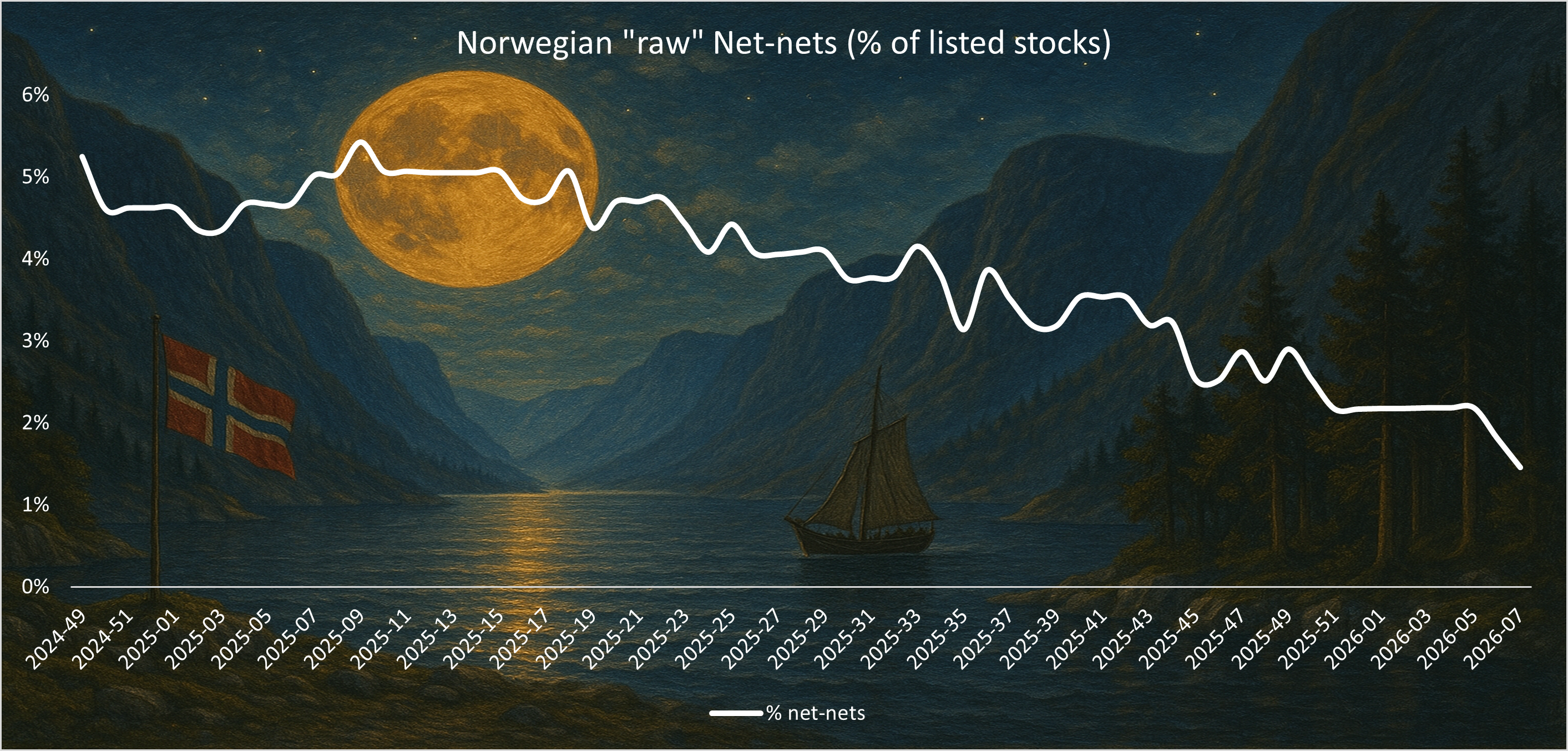

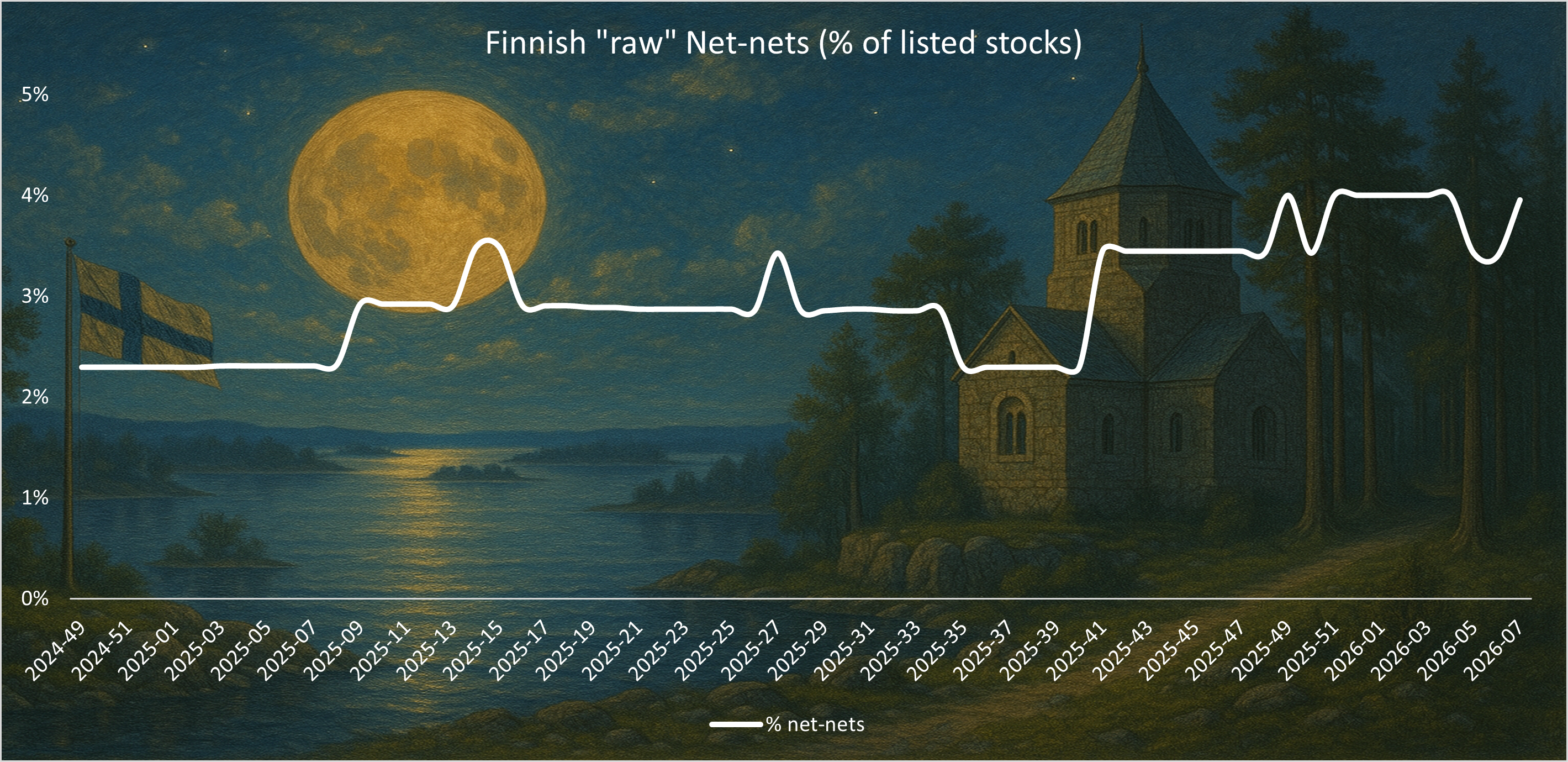

“Graham’s Geiger counter”

Benjamin Graham suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive. Today’s net-nets, however, are not the same as Graham’s net-nets. Many are un-investable being Chinese RTO’s, loss-making biopharma’s etc. But we do think it is interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable.

DELFINGEN – FY2025 Revenue in Line; Margin Target Reaffirmed

2026-02-09 │ P/TB 1.68 │ URL

09 February 2026 – DELFINGEN reported FY2025 revenue of €400.3m, down 5.5% year-on-year (-3.1% at constant exchange rates), in line with expectations despite a €10.2m negative currency impact. Q4 revenue declined 9.4% to €89.6m (-4.4% at constant exchange rates), reflecting continued pricing pressure and an unfavorable €/$ effect. Automotive sales fell 6.4% for the year (-4.1% CER) to €333.4m, while Industry was broadly stable at €66.8m (+1.8% CER). The Americas region was impacted by the voluntary termination of least profitable fluid transfer tubing (FTT) contracts (-49% like-for-like), reducing revenue by €12m, whereas Asia grew 10.1% at constant exchange rates. The Textiles business increased 7.3% and now represents 20% of group sales, supported by production relocation to China and India under the IMPULSE 2026 plan. The company reaffirmed its target of a current operating margin above 7% for 2025 and confirmed a significant reduction in leverage, supported by improved cash generation. For 2026, management expects stable revenue at constant exchange rates, with a focus on value over volume, further margin improvement and continued deleveraging, alongside expansion in higher value-added industrial markets.

Bertrandt – Positive Q1 EBIT; Guidance Confirmed and Diversification Accelerates

2026-02-12 │ P/TB 0.73 │ URL

12 February 2026 – Bertrandt AG reported a solid start to FY2025/2026 with a small positive EBIT in Q1 and confirmed its full-year guidance. The EBIT margin remained around break-even in the quarter, with management reiterating a medium-term margin target of 6–9%. CFO Markus Ruf expects positive EBIT and strong cash flow for the full year, supported by a cost-cutting program that achieved its upper €90m savings target and helped stabilize earnings. Operationally, Digital Engineering continues to face underutilization, while Physical Engineering showed significant improvement and Electronics remained profitable despite market pressure. Total assets declined following repayment of a €103m bond, lifting the equity ratio to 46%. Diversification efforts are gaining traction, with Aerospace and Defense posting growth and the non-automotive revenue share targeted to reach 25% by 2027. The company is also entering a partnership with Volvo Cars in Sweden to drive further growth. For the remainder of the year, management maintains its outlook for positive EBIT and strong cash flow, with continued focus on capacity utilization, margin expansion and reducing cyclicality through sector diversification.

Bertrandt AG – Montega Reiterates Buy; €26 Target on Stabilization Signs

2026-02-13 │ P/TB 0.73 │ URL

13 February 2026 – Montega AG reiterated its Buy rating on Bertrandt AG with a €26.00 target price (12-month horizon) following the Q1 FY2025/2026 update. Revenue of €233.7m was down 12.2% year-on-year but broadly stable sequentially (-0.7% vs. Q4), despite three fewer working days, signaling continued operational stabilization since Q3 2024/2025. Montega highlights first signs of recovery in the German market, with increasing project inquiries expected to support top-line momentum in H2. Despite double-digit revenue decline, EBIT turned positive year-on-year, reflecting the effectiveness of the Fit-for-Future (F3) efficiency program, which reduced headcount from 13,605 to 11,932 and delivered high double-digit €m annual savings through personnel and process measures. The leaner cost base positions the company to benefit disproportionately from improving capacity utilization. Montega also sees potential regulatory tailwinds from a possible easing of EU fleet emission targets, which could broaden drivetrain platforms beyond 2035 and structurally increase development demand per model generation. The analysts expect operational recovery in FY2026/2027 and view the valuation (EV/EBIT ~5.0x) as attractive, maintaining the Buy recommendation and €26 price target.

Groupe Plastivaloire – Plans Transfer to Euronext Growth to Simplify Listing Framework

2026-02-09 │ P/TB 0.65 │ URL

09 February 2026 – Groupe Plastivaloire announced a project to transfer its listing from the regulated market of Euronext Paris (Compartment C) to Euronext Growth Paris, subject to shareholder approval at the General Meeting on 31 March 2026. The Board approved the proposal on 12 December 2025. The group meets eligibility criteria for Euronext Growth, including market capitalization below €1bn and a free float above €2.5m. Management cites reduced regulatory constraints and lower compliance costs as key motivations, while maintaining access to capital markets in a framework deemed more suited to the company’s size and profile. Following the transfer, periodic reporting requirements would be simplified, including extended deadlines for annual and half-year reporting, no obligation for “say on pay,” and lighter AGM formalities, although the company would continue quarterly revenue disclosure and IFRS reporting. Ongoing disclosure obligations under EU market abuse regulation would remain in force, and minority shareholder protection would be ensured via mandatory takeover rules at the 50% threshold, with certain Euronext Paris obligations maintained for three years post-transfer. Subject to approval and Euronext’s consent, delisting from Euronext Paris and admission to Euronext Growth could occur from 25 May 2026 at the earliest, with TP ICAP Midcap acting as listing sponsor.

POLYTEC Holding AG – Research Error Corrected; Guidance Reaffirmed

2026-02-10 │ P/TB 0.43 │ URL

10 February 2026 – POLYTEC Holding AG reported increased trading volumes and share price weakness on 9–10 February following the accidental release of a draft research note by Baader Europe containing a calculation error in the valuation section. The erroneous version cited a €2.20 price target and a “Sell” recommendation; this was corrected the same day to “Reduce” with a €4.03 target, broadly in line with the prior share price. Baader Europe has since apologized to market participants. POLYTEC is currently covered by three research houses: Baader Europe (“Reduce”, €4.03), M.M.Warburg & CO (“Buy”, €5.75), and ODDO BHF (“Outperform”, €4.00), implying an average target price of €4.59. Management reiterated its FY2025 outlook, guiding for revenue of €660–680m, an EBIT margin of around 2.5%, and a positive net result for the year. The annual report will be published on 30 April 2026.

SMT Scharf AG – MoUs in China for Battery Transport; Majority in Xinsha and Canada Exit

2026-02-12 │ P/TB 0.39 │ URL

12 February 2026 – SMT Scharf AG announced strategic and structural measures to expand its electric transport offering and streamline operations. The company signed two non-binding MoUs with Chinese LEV providers, Delta Industrial Intelligent Electric Vehicle Co., Ltd. and Shanxi Tiandi Coal Mining Machinery Equipment Co., Ltd., to jointly develop lithium battery-powered transport solutions for underground coal and non-coal mining as well as tunneling logistics. Binding agreements are targeted by mid-2026, with development and production primarily based in China and supported by group subsidiaries. In parallel, the group is finalizing ATEX certification for the lithium battery monorail system of joint venture Shandong Xinsha Equipment Monorail Co., Ltd. for the European market. SMT Scharf plans to increase its stake in Xinsha from 50% to 51% via its subsidiary SMT Scharf GmbH, enabling consolidation and a planned rebranding to SMT Scharf (China) Co., Ltd., strengthening governance and market positioning in China; Xinsha is also considering bringing in strategic investors for the remaining 49%. Additionally, the group will discontinue operations at Canadian subsidiary RDH Mining Equipment Ltd. due to underperformance and limited profitability prospects, with its future role under review.

Siltronic AG – 2026 Guidance Points to Lower Sales and Margin Pressure

2026-02-12 │ P/TB 0.84 │ URL

12 February 2026 – Siltronic AG issued its FY2026 guidance, expecting group sales to decline in the mid-single-digit percentage range year-on-year (2025 preliminary: €1,347m), based on an assumed EUR/USD rate of 1.18. On a comparable basis, excluding exchange rate effects and the closure of the SD production line in Burghausen, revenue is projected to be roughly in line with the prior year, although management anticipates a subdued start to 2026. The company highlighted headwinds from unfavorable FX, ongoing price pressure outside long-term agreements, a decline in 200 mm wafer demand due to inventory reductions in the power segment, and the full-year impact of the SD line closure, while 300 mm volumes are supported by AI-driven end markets. EBITDA margin is guided at 20–24% (2025 preliminary: 23.5%). Depreciation is expected to increase significantly to €490–520m due to prior 300 mm investments, resulting in EBIT significantly below the previous year (2025 preliminary: €-26m). Capex is set to decline to €180–220m (2025 preliminary: €369m), but as cash outflows for investments will exceed this level, net cash flow is anticipated to remain around last year’s level (2025 preliminary: €-85m).

AIREA PLC – Newlands Increase Stake Above 15% Threshold

2026-02-11 │ P/TB 0.55 │ URL

11 February 2026 – AIREA PLC announced a TR-1 notification that David and Monique Newlands have increased their holding in the company. On 10 February 2026, the pair crossed the 15% threshold, raising their stake to 15.061% of voting rights, equivalent to 6,228,500 shares, compared with a previous position of 12.411%. The notification relates solely to voting rights attached to shares, with no financial instruments involved. The transaction was completed in the UK on 10 February 2026 and reflects an acquisition of voting rights.

IG Design Group plc – Trading Ahead of Expectations; Cash Stronger Than Forecast

2026-02-11 │ P/TB 0.74 │ URL

11 February 2026 – IG Design Group plc issued a trading update for the nine months to 31 December 2025, reporting performance in line with expectations and a strong Christmas trading period. For FY2026 (ending 31 March 2026), management now expects results at the upper end of prior guidance and above current market consensus, with revenue projected at approximately $280–285m and Q4 sales broadly in line with the prior year. Adjusted operating margin is expected at around 4%, the top end of the previous 3–4% range, and together with higher-than-expected interest income, adjusted profit is set to exceed market expectations. Net cash is forecast at $55–60m, around $15–20m ahead of consensus, supported by disciplined working capital management following the disposal of DG Americas and the anticipated sale of a surplus UK warehouse before year-end. Looking beyond FY2026, the Board reiterated guidance for annual revenue growth of 0–5%, adjusted operating margins of 4–5% and sustainable annual cash generation of $6–8m, alongside continued focus on long-term growth initiatives. The company expects to publish FY2026 results in June 2026, provide an update on capital allocation following shareholder approval of a capital reduction, and will adopt GBP as its presentation currency from the FY2026 full-year results.

IG Design Group plc – Canaccord Genuity Reduces Stake to 11.05%

2026-02-13 │ P/TB 0.74 │ URL

13 February 2026 – IG Design Group plc announced a TR-1 notification that Canaccord Genuity Group Inc. has reduced its holding below the previous disclosure level. On 12 February 2026, Canaccord crossed the relevant threshold, lowering its total voting rights to 11.0515%, equivalent to 10,864,541 shares, compared with a prior position of 13.9872%. The holding relates entirely to voting rights attached to shares, with no financial instruments reported. The stake is held through discretionary clients and a chain of controlled undertakings within the Canaccord Genuity group, including wealth and asset management subsidiaries.

Sanderson Design Group plc – FY2026 In Line; Profit and Cash Improve

2026-02-10 │ P/TB 0.78 │ URL

10 February 2026 – Sanderson Design Group plc reported full-year trading for the year ended 31 January 2026 in line with expectations, with revenue of £99.5m (FY2025: £100.4m), down 1% reported and flat at constant currency. Adjusted underlying profit is expected to be at least £5m (FY2025: £4.4m), reflecting strategic cost-saving initiatives, while net cash increased to approximately £9.8m (FY2025: £5.8m), supported by inventory reductions, disciplined working capital management and controlled capex. Brand product revenue declined 2% overall, with UK sales down 9%, offset by strong North America performance (underlying +5% reported, +9% CER) and improved second-half momentum in Northern Europe and other overseas markets. Third-party manufacturing revenue rose 5% to £18.9m, with operations expected to achieve slightly above break-even for the year, and licensing delivered £10.5m, with underlying licensing income up strongly due to minimum guarantees and renewals. Direct-to-consumer sales increased to £1.8m (FY2025: £0.4m), driven primarily by Morris & Co. and US growth. Entering the new financial year, management sees increasing momentum in the US, manufacturing and DTC channels, though UK conditions remain subdued, and reiterates confidence in the group’s strategy; full-year results are scheduled for late April 2026.

Severfield plc – Andrew Page Appointed CFO and Executive Director

2026-02-11 │ P/TB 1.16 │ URL

11 February 2026 – Severfield plc announced the appointment of Andrew Page as Chief Financial Officer and Executive Director, effective 16 February 2026. He succeeds Jan Bramall, who has served as Interim CFO since 1 November 2025, following a Board-led search supported by external advisers. Page most recently served as Interim CFO at ISG and previously held senior finance roles at British Energy Group plc, Centrica plc, FirstGroup plc and Ocado Group plc. The company noted that a number of ISG entities where Page served as director ceased trading in September 2024 and are currently in administration or liquidation, as required under UK Listing Rules disclosure. Management highlighted his experience in UK-listed environments and capital markets expertise as supportive of the group’s ongoing strategic transformation and long-term growth plans.

MJ Gleeson plc – H1 Robust but Cautious on FY Outturn; Guidance Update Due in April

2026-02-11 │ P/TB 0.64 │ URL

11 February 2026 – MJ Gleeson plc reported a “robust performance” for the half year ended 31 December 2025 in a subdued market, with group revenue up 9.6% to £173.1m, driven by Gleeson Homes (+7.7% to £168.6m) and higher Gleeson Land activity (£4.5m vs £1.3m). Profitability softened as group underlying operating profit fell 17.6% to £4.2m and underlying PBT declined to £2.0m, reflecting a lower operating margin in Homes (4.1% vs 5.8%) as selling price increases lagged build cost inflation and incentives remained elevated. Homes volumes rose to 848 completions (801), average selling price increased 2.5% to £198.8k, and the forward order book grew 64% to 978 plots, supported by three additional partnership agreements; gross margin on home sales eased to 19.8% (20.6%). Net debt increased to £22.5m as the group opened nine new build sites and invested ahead of the spring selling season, while Gleeson Land completed three sales and saw record planning activity (15 applications submitted) underpinning future site supply. Early 2026 trading showed improving open-market demand (net reservations per site 0.55 in the five weeks to 6 February, +38% vs the prior three months), but the bulk investor market has softened further and margins remain under pressure from build costs, regulation and tax headwinds. For the full year, management said current market expectations remain achievable but a strong spring selling season is critical, and it will update guidance in April 2026 as visibility improves.

Ferronordic AB – Q4 Profitability Improved; FY Net Loss but Strong Operating Cash Flow

2026-02-12 │ P/TB 0.71 │ URL

12 February 2026 – Ferronordic AB reported improved profitability in Q4 2025 despite lower sales, with net revenue down 10% to 1,211 msek while EBIT rose to 31 msek (2 msek), implying a 2.6% margin (0.2%); adjusted for one-offs, EBIT was stated as 54 msek. Operating cash flow improved to -41 msek from -480 msek, and management highlighted a stronger balance sheet with net debt/EBITDA improving to 3.4x from 5.2x a year earlier. For FY2025, revenue fell 6% to 4,566 msek, EBIT increased to 77 msek (21 msek) and margin to 1.7% (0.4%), while net profit declined to -199 msek (-89 msek), with operating cash flow up to 701 msek (340 msek) and net debt reduced to 1,616 msek (1,978 msek). The US business delivered a strong quarter with sales up 16% in USD and EBIT of 73 msek, and the group completed the acquisition of Housby Heavy in Iowa after quarter-end as a first step in geographic expansion. Germany remained weak but showed early recovery signs; cost savings actions are expected to deliver 16–17 msek annually but included one-off costs of 17 msek, and excluding one-offs EBIT was -9 msek. Kazakhstan continued to work down older inventory, with stable aftermarket margins and EBIT around break-even excluding one-offs. Given the FY2025 net loss, the Board proposed no dividend. Looking ahead, management remains optimistic, expecting continued strong activity in US infrastructure and data center-related investment, a gradual recovery in Germany with a strengthened service organization and lower cost base, and improving conditions in Kazakhstan supporting both sales and profitability.

Corem Property Group AB – Large Value Declines and Portfolio De-Risking via Disposals, Including US Exit Steps

2026-02-13 │ URL

13 February 2026 – Corem Property Group AB (publ) reported FY2025 results with lower income and significant negative property revaluations, as rental income fell to 3,465 msek (3,695) and NOI to 2,225 msek (2,362), while net financial items improved slightly to -1,225 msek (-1,288) and profit from property management decreased to 863 msek (914). Value changes on investment properties were -3,906 msek (-1,717), driving a net result of -3,311 msek (-1,058), equivalent to -2.96 SEK per A and B ordinary share, and NAV per A/B share declined to 10.70 SEK (15.97); the investment property portfolio value was 46,937 msek (55,205) and net letting for the year was 7 msek (61). During 2025, Corem transferred 46 properties with an underlying value of 5.2 bn sek, generating a reported earnings effect of 302 msek including reversed deferred tax, and in Q4 alone completed 22 disposals (2.4 bn sek), including the 28&7 project property in Manhattan, a Copenhagen asset and a 14-property portfolio across several Swedish cities. Corem also signed an LOI in December to divest the 417 Park Avenue project site in New York, which resulted in an approximately -1.5 bn sek negative earnings impact in 2025; a binding SPA was signed in January 2026, all conditions have since been fulfilled, and closing is expected in Q2 2026 (planned for April 2026). The company initiated share buybacks under the AGM mandate and repurchased 153 msek of bonds in Q4, while Scope Ratings revised Corem’s rating to BB+ with stable outlook (from BBB- with negative outlook). Management emphasized ongoing de-risking through reduced US exposure and a more selective transaction strategy focused on non-core assets, noting improved net letting in Q4 (27 msek) despite softer leasing markets and a slightly lower economic occupancy due to disposals, alongside cost discipline and energy-efficiency measures supporting stable comparable NOI and lower comparable operating costs. Looking into 2026, the CEO described Corem as more focused and financially stronger after disposals, a summer equity issue, hybrid bond redemption in Q3, early-2026 investments in listed Nordic bank shares and the start of share buybacks, and expects clearer macro recovery while continuing to prioritize portfolio focus, capital structure optimization and sustainability-led competitiveness.

ES Energy Save Holding – CEO succession: Deputy CEO Yibo Zhao to become CEO at AGM; current CEO proposed as Executive Chair

2026-02-11 │ P/TB 0.73 │ URL

11 February 2026 – ES Energy Save Holding AB (publ) announced a planned management and board succession. The Board has appointed current Deputy CEO Yibo Zhao as new CEO, effective from the AGM on 29 April 2026; current CEO Fredrik Sävenstrand will remain CEO until the AGM. The company’s largest shareholders (Christian Gulbrandsen and Fredrik Sävenstrand via Project Air AB) intend to propose that Sävenstrand is elected Executive Chairman at the AGM; the third-largest owner (Tedde Jeansson) is stated to be positive to the proposal. Current Chairman Per Wassén is available for election as a board member and is intended to be proposed as Deputy Chairman. Yibo Zhao joined in January 2022, has been COO with responsibility for ISO certification, is currently Deputy CEO, owns 54,423 shares, and has recently worked on strengthening sales under the ES Energy Save own brand.

FASING – Orders from subsidiary Fasing America Corp. (USA)

2026-02-09 │ P/TB 0.28 │ URL

Fabryki Sprzętu i Narzędzi Górniczych Grupa Kapitałowa FASING S.A. announced that on 9 February 2026 it accepted a new order (conveyor parts) from its US subsidiary Fasing America Corp. valued at USD 859.9k. Orders placed by Fasing America Corp. since 25 September 2025 (publication of Current Report No. 48/2025), including this latest order, amount to USD 4,931.6k. In practical terms, the disclosure highlights continued intra-group sales activity to the US market, with nearly USD 4.9m in aggregate orders over roughly 4.5 months.

KPPD-Szczecinek – Preliminary 2025 Results Show Improved Profitability

2026-02-15 │ P/TB 0.46 │ URL

15 February 2026 – KPPD-Szczecinek reported preliminary 2025 revenue of PLN 332m, up from PLN 326m in 2024, while gross profit on sales increased to PLN 25.8m from PLN 15.3m. EBITDA turned positive at PLN 1.9m compared with PLN -20.7m the previous year, and the net result improved to PLN -20.3m from PLN -44.2m, indicating a significantly reduced loss year-on-year. The company noted that the 2025 figures are preliminary and may differ from the final audited results to be presented in the annual financial statements.

Relpol – Subsidiary Deleted from National Court Register

2026-02-15 │ P/TB 0.74 │ URL

15 February 2026 – Relpol announced that on 12 February 2026 it received a decision from the District Court in Zielona Góra, 8th Commercial Division of the National Court Register, confirming the deletion of its subsidiary Relpol Elektronik sp. z o.o. in liquidation from the register. The decision follows the earlier resolution to liquidate the subsidiary, disclosed in January 2022, after which the entity ceased conducting statutory activities.

Remak-Energomontaż – Selected as Most Advantageous Bidder for PLN 25.8m Turbine Contract

2026-02-15 │ P/TB 0.53 │ URL

15 February 2026 – Remak-Energomontaż announced that PGE Energia Ciepła S.A., Warsaw, has selected the company’s bid as the most advantageous in a public procurement procedure covering repairs, inspections and servicing of a 7CK65 steam turbine with equipment. The total net value of the offer amounts to PLN 25.75m (PLN 31.67m gross). The company stated that further details will be disclosed in a separate report should the contract be formally signed, and highlighted the event as significant due to its value and importance for the issuer.

Remak-Energomontaż – Signs Annex Increasing Contract Value to PLN 26.9m

2026-02-15 │ P/TB 0.53 │ URL

15 February 2026 – Remak-Energomontaż announced that on 12 February 2026 it concluded Annex No. 2 to its agreement with ZARMEN Sp. z o.o. relating to the assembly of technological steel pipelines as part of the EPC investment for ORLEN Południe S.A.’s second-generation bioethanol (B2G) installation at the Jedlicze production plant. The annex expands the scope of work to include additional tasks and increases the contractor’s total estimated remuneration to PLN 26.90m net, representing a net increase of PLN 0.48m. The final remuneration will be calculated based on unit prices specified in the agreement. The company classified the event as material due to its significance for the issuer.

STALPROFIL – Extraordinary General Meeting Adopts Statute and Remuneration Policy Amendments

2026-02-15 │ P/TB 0.29 │ URL

15 February 2026 – STALPROFIL held an Extraordinary General Meeting on 12 February 2026, during which shareholders representing 56.87% of the share capital adopted a series of resolutions. The meeting elected Ewa Szymura as Chair and approved the proposed agenda, followed by resolutions amending the company’s Articles of Association and updating the Remuneration Policy for the Management and Supervisory Boards. The amendments to the Articles primarily expand and уточнить the company’s scope of business activities across wholesale steel trading, construction, infrastructure, industrial services, waste management, transport and financial support activities, while also detailing and broadening the powers of the Supervisory Board, including oversight, approval, and governance competencies. The updated remuneration policy was adopted in a consolidated text reflecting the approved changes. All resolutions were passed with a clear majority of votes cast.

The writer may own shares of the companies mentioned. This communication is for informational purposes only. AI helped us with this. Check important info.

Really interesting take on using Graham’s “net-net count” as a market thermometer. Even if today’s net-nets aren’t as investable as in Graham’s time, tracking their share still feels like a useful way to gauge overall market froth. The Delfingen update also shows how much execution and margins matter in cyclical names. Curious how much weight you personally put on the net-net signal versus company-specific fundamentals when positioning.

I’ve subscribed and would be happy to support each other.

Jorrit