The European Deep Value Week – 2025/18

Lots of Reports, AGM’s, updated outlooks and Dividends

Companies mentioned:

· Headlam Group (HEAD) - Directors Acquire Shares and CEO Exercises Deferred Bonus Option

· IG Design (IGR) - Reports FY25 Results, Eyes DG Americas Exit Amid Tariff Pressures

· Northamber (NAR) - Appoints Matthew Light as Executive Director to Strengthen AV Business

· Sanderson Design Group (SDG) - FY25 Loss Amid Market Weakness and Goodwill Impairment

· Naked Wines (WINE) - Director-Linked Entity Acquires Additional Shares

· James Cropper (CRPR) - Strategic partnership with HOERBIGER and divests non-core IP assets

· Altheora (ALORA) - €37m Revenue, 5.8% EBITDA Margin, €1.7m Net Loss Amid Strategic Transition in 2024

· Herige Industries (ALHRG) - 2024 Results — Strong Focus on Industrial Growth and Profitability

· Installux Group (ALLUX) – 2024 Annual Report

· Akwel (AKW) – Q1 2025 Turnover Decline and Stable Cash Position

· Centrale del Latte d’Italia (CLI) – Shareholders Approve 2024 Financial Statements

· Delignit AG (DLX) – Revenue and EBITDA Decline in FY24, Stable Cash Flow and Solid Balance Sheet

· Emak S.p.A. (EM) – Shareholders Approve FY 2024 Results, Dividend of €0.025 per Share

· Encres Dubuit (ALDUB) — Revenue Stabilization Amidst Ongoing Turnaround Efforts

· Laboratoires Euromedis (ALEMG) - Revenue Growth in 2024 Offset by Exceptional Charges, Resulting in Net Loss

· Guerbet (GBT) - Revenue Growth and Profitability Improve in 2024 Amidst Continued High Debt

· DR. HÖNLE AG (HNL) - UV Technologies for Battery Manufacturing Introduced at Battery Show Europe 2025

· Exacompta Clairefontaine (EXAC) – 2024 Financial Results and AGM Decisions

· H&R GmbH & Co. KGaA – Preliminary Q1 2025 Results Slightly Improved

· Passat SA (PSAT) - 2024 Revenue Decline and Lower Net Profit Amid Rising Financial Expenses

· SMT Scharf Reports (S188) - Strong Q1 2025 Revenue Growth and Improved Profitability

· InTiCa Systems SE (IS7) - Preliminary FY24 Results; Final Financial Reports Delayed

· Lacroix (LACR) - Targets Growth in Heating Networks and Building Management Systems

· Iberpapel (IBG) - Reports €1.1 Million Net Profit in Q1 2025 Despite Market Pressures

· Exel Industries (EXE) - Q2 2024–2025 Sales Decline of 3.8%, Maintains Resilience Amid Market Challenges

· Nimbus Group (BOAT) - Weak Q1 2025 sales amid market uncertainty, premium segment resilient

· Harboes Bryggeri (HARB) - Q3 2024/25 sees revenue growth but lower margins; full-year guidance cut

· HKFoods (HKFOODS) - Evaluating sale of Polish bacon unit to strengthen balance sheet

· Ilkka (ILKKA) - Media business merger with Kaleva completed, gains EUR 4m & management team change announced & Ilkka Q1 2025: Revenue Growth Offset by Weak Profitability Amid Restructuring

· Tecnotree (TEM1V) - Q1 2025: Modest Revenue Growth, Strong Free Cash Flow and Strategic Market Shift & Wins Multi-Million Euro Digital BSS Deal in the Netherlands

· K-Fastigheter (KFAST) - Sells Property Portfolio to Joint Venture K-Fast Kilen AB & Q1 2025: Strong property management profit, strategic portfolio shifts

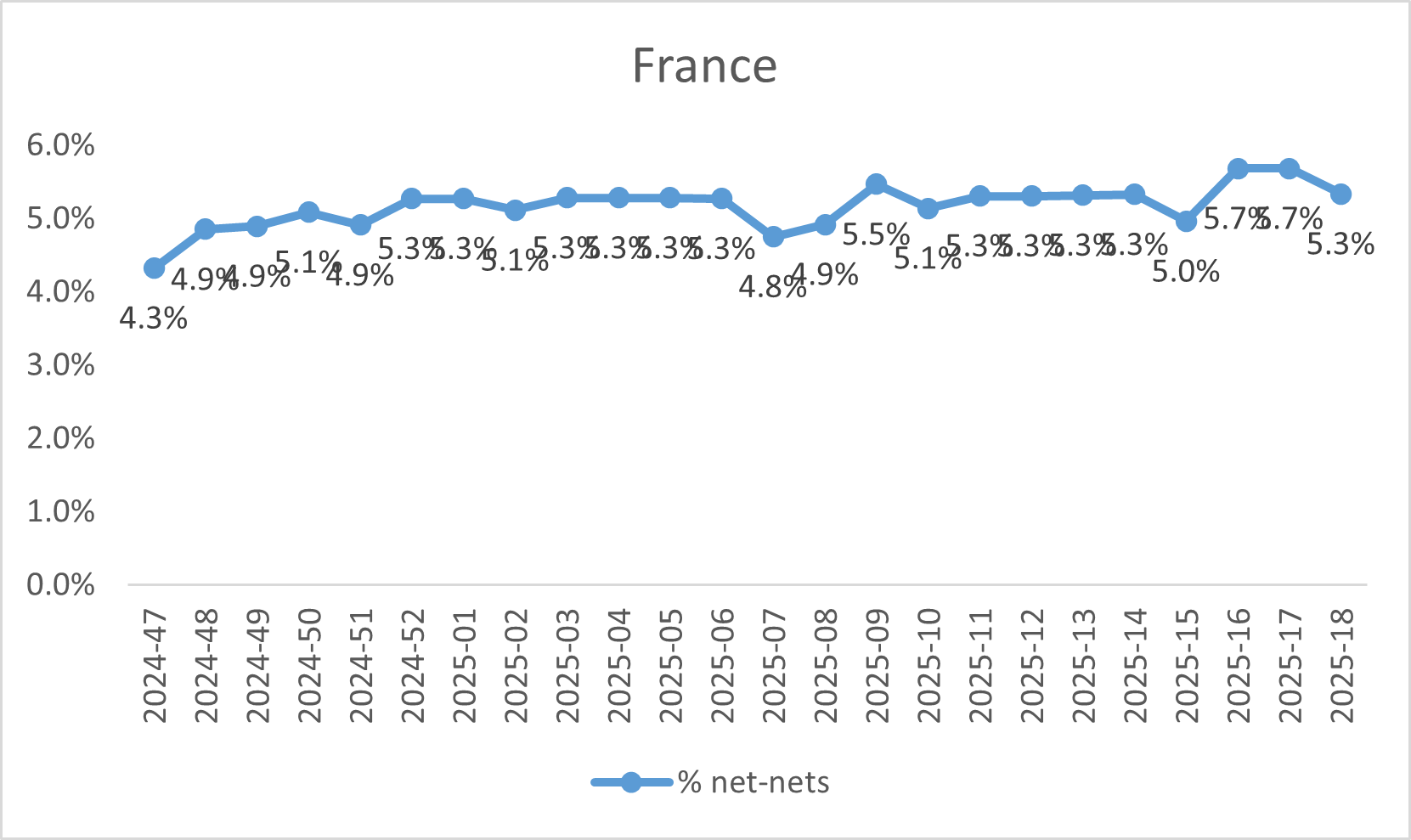

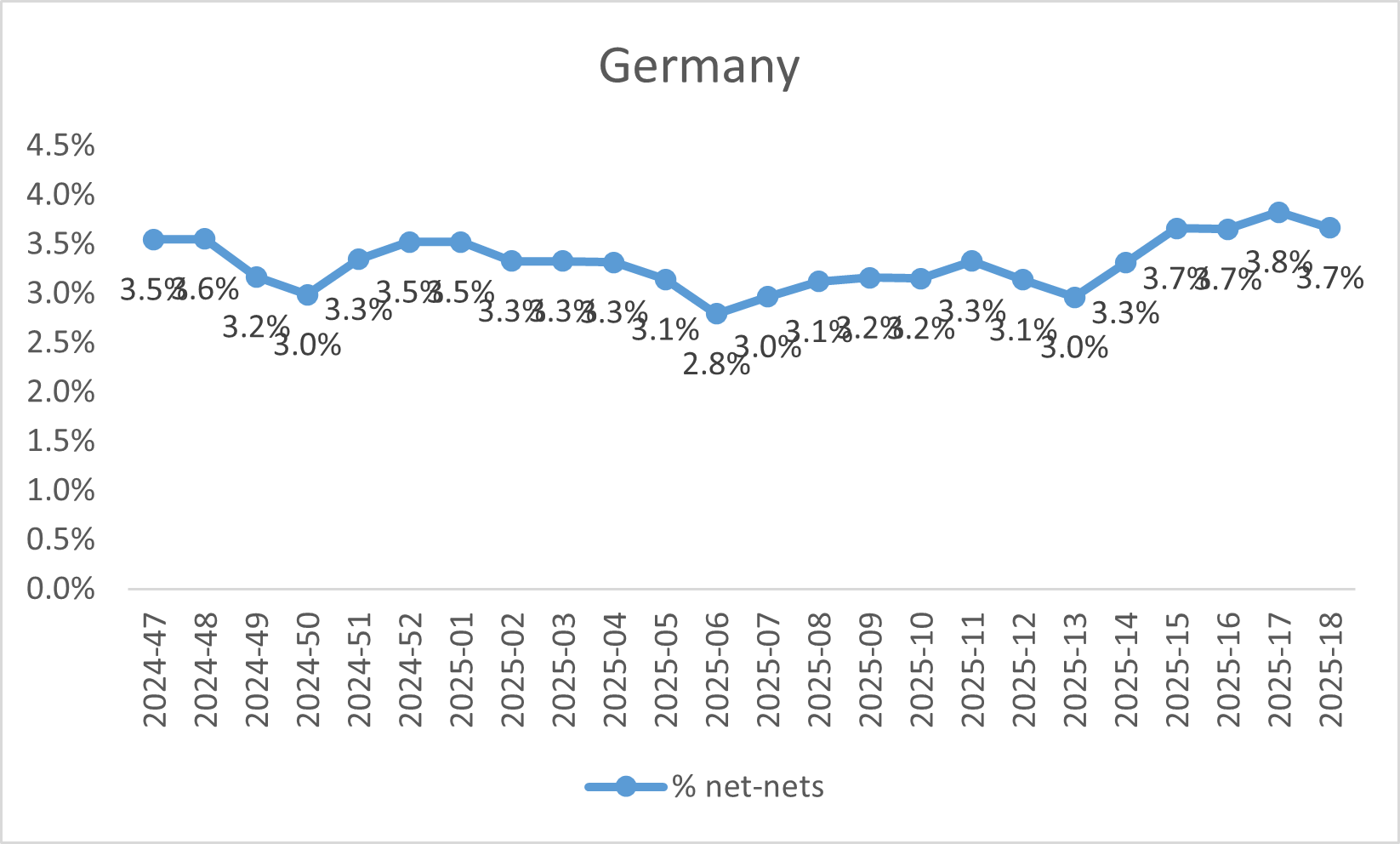

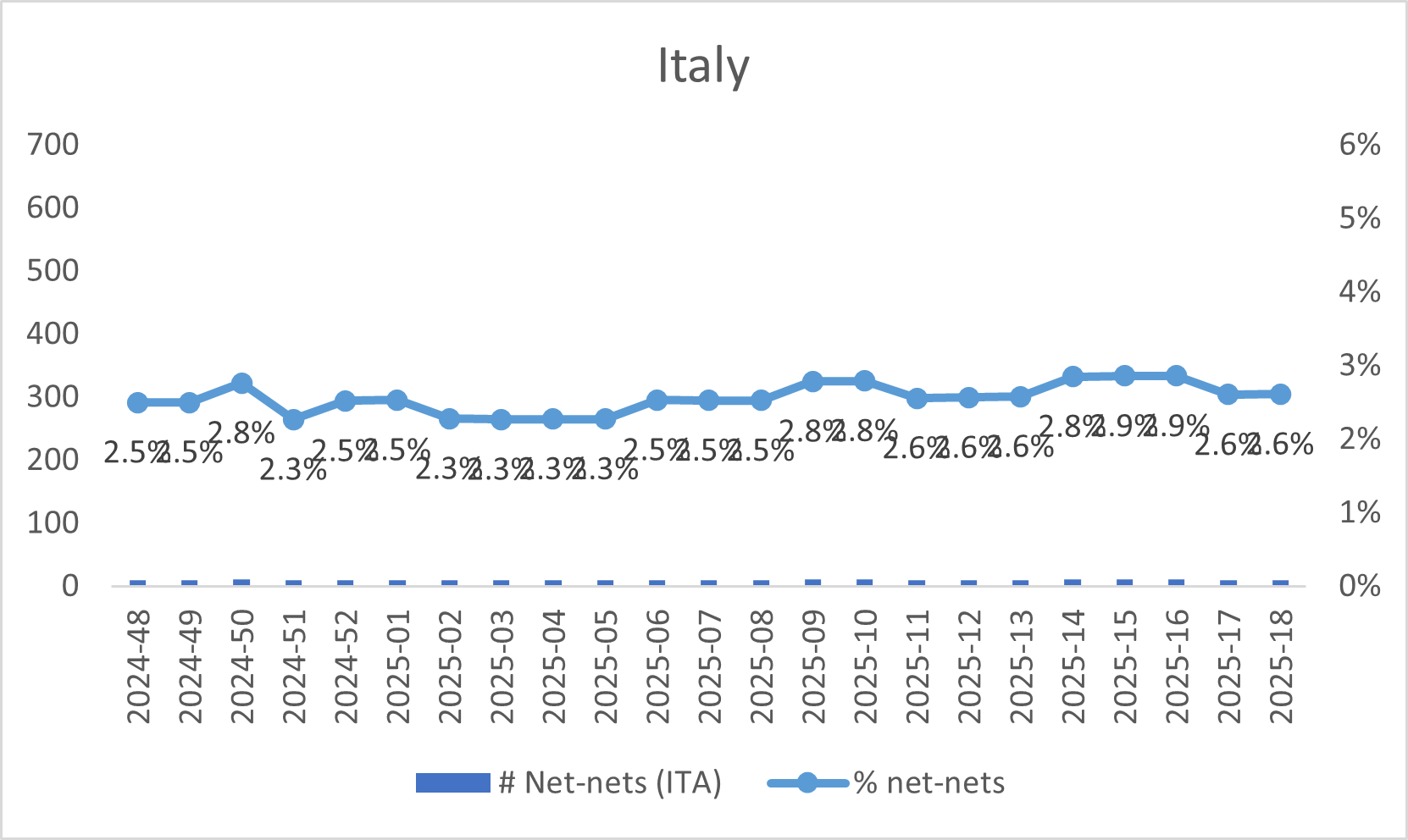

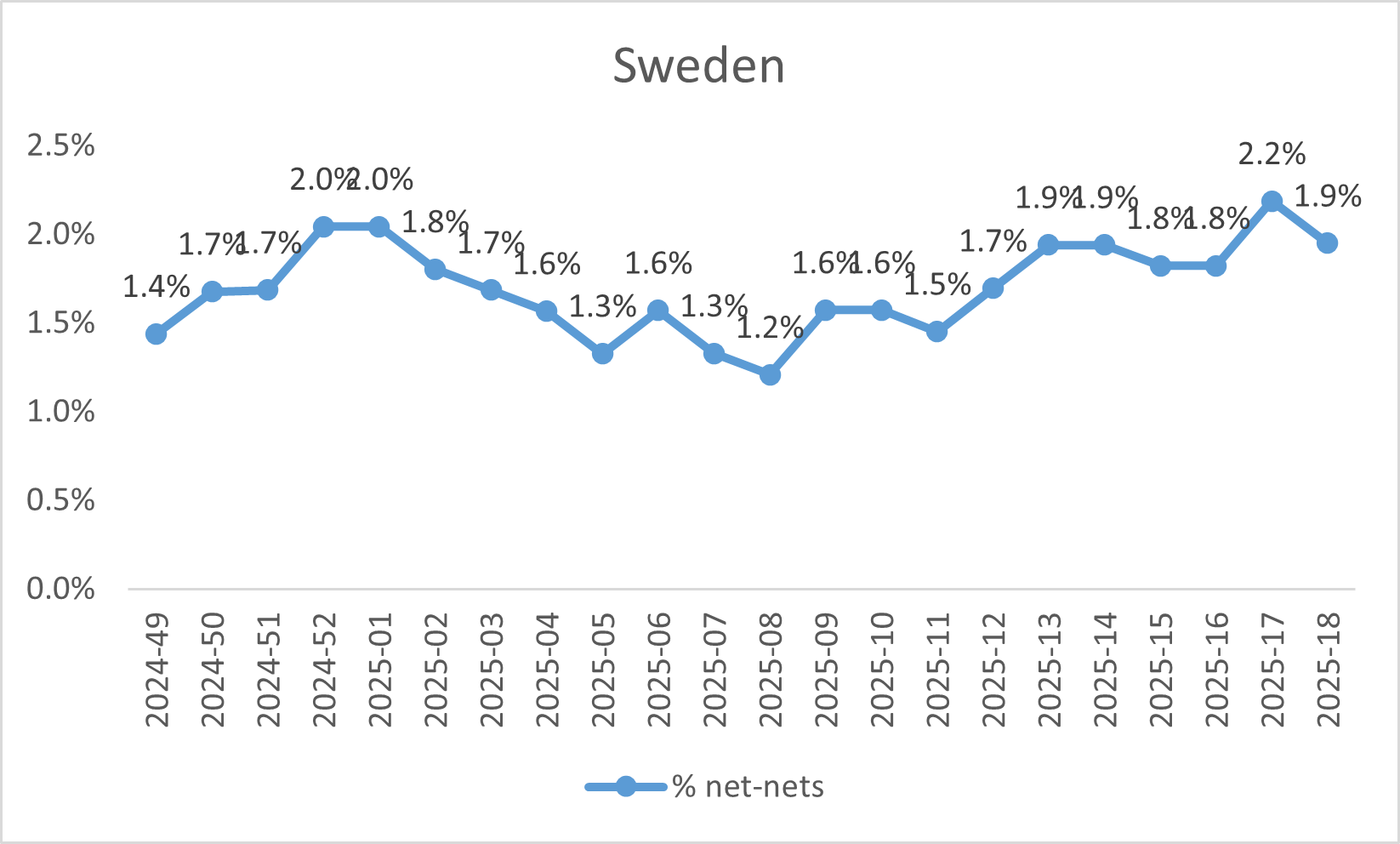

“Graham’s Geiger counter”

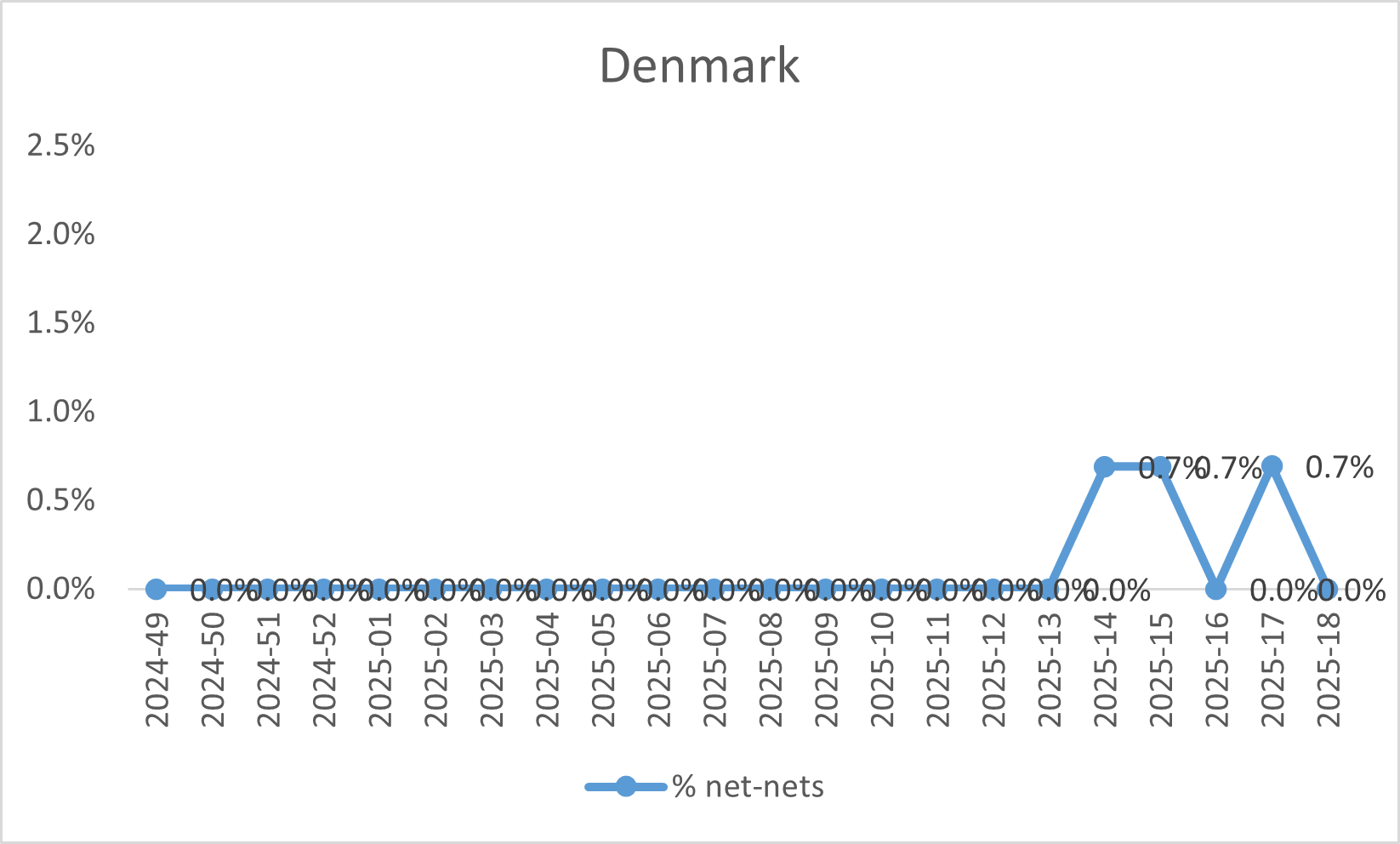

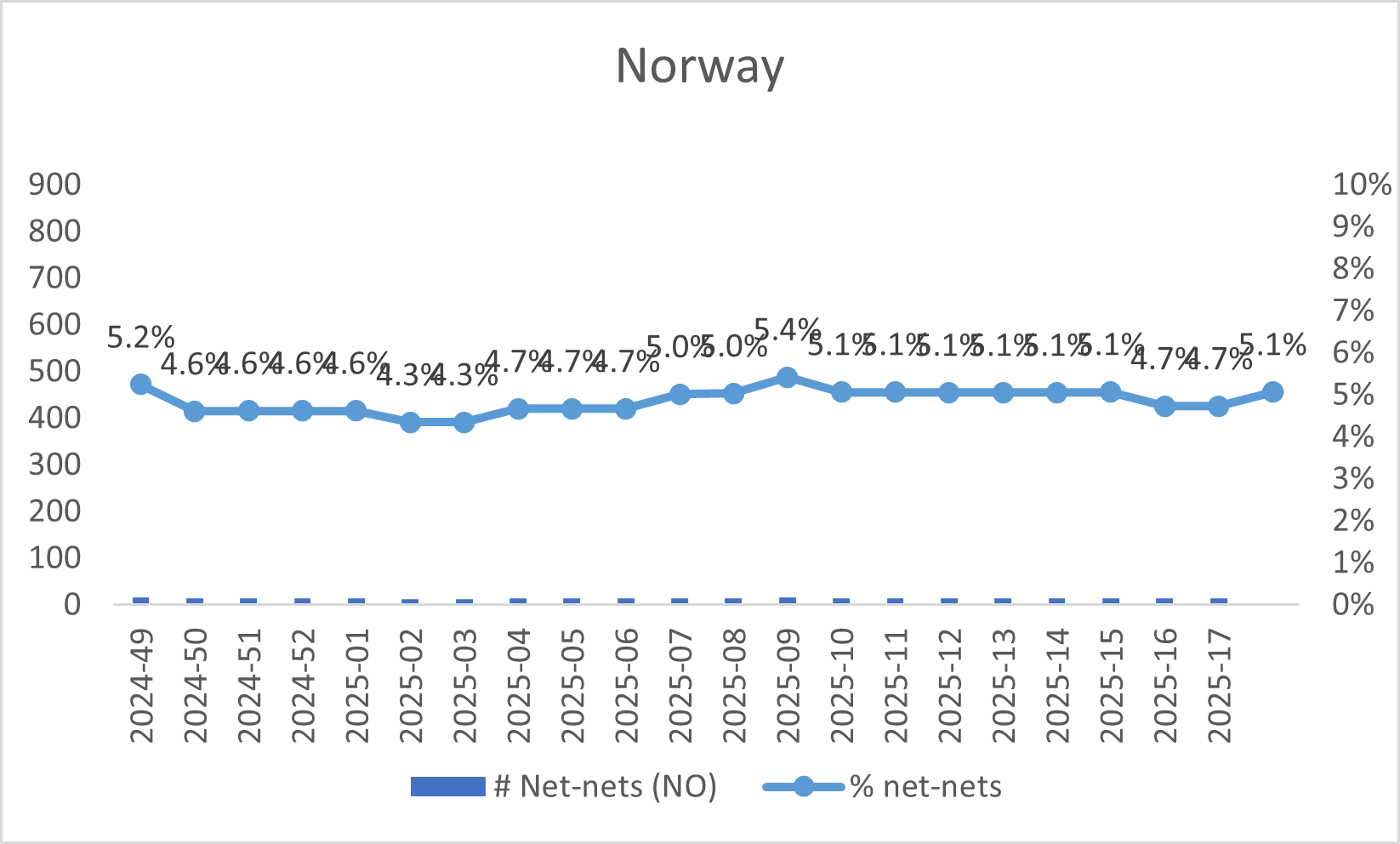

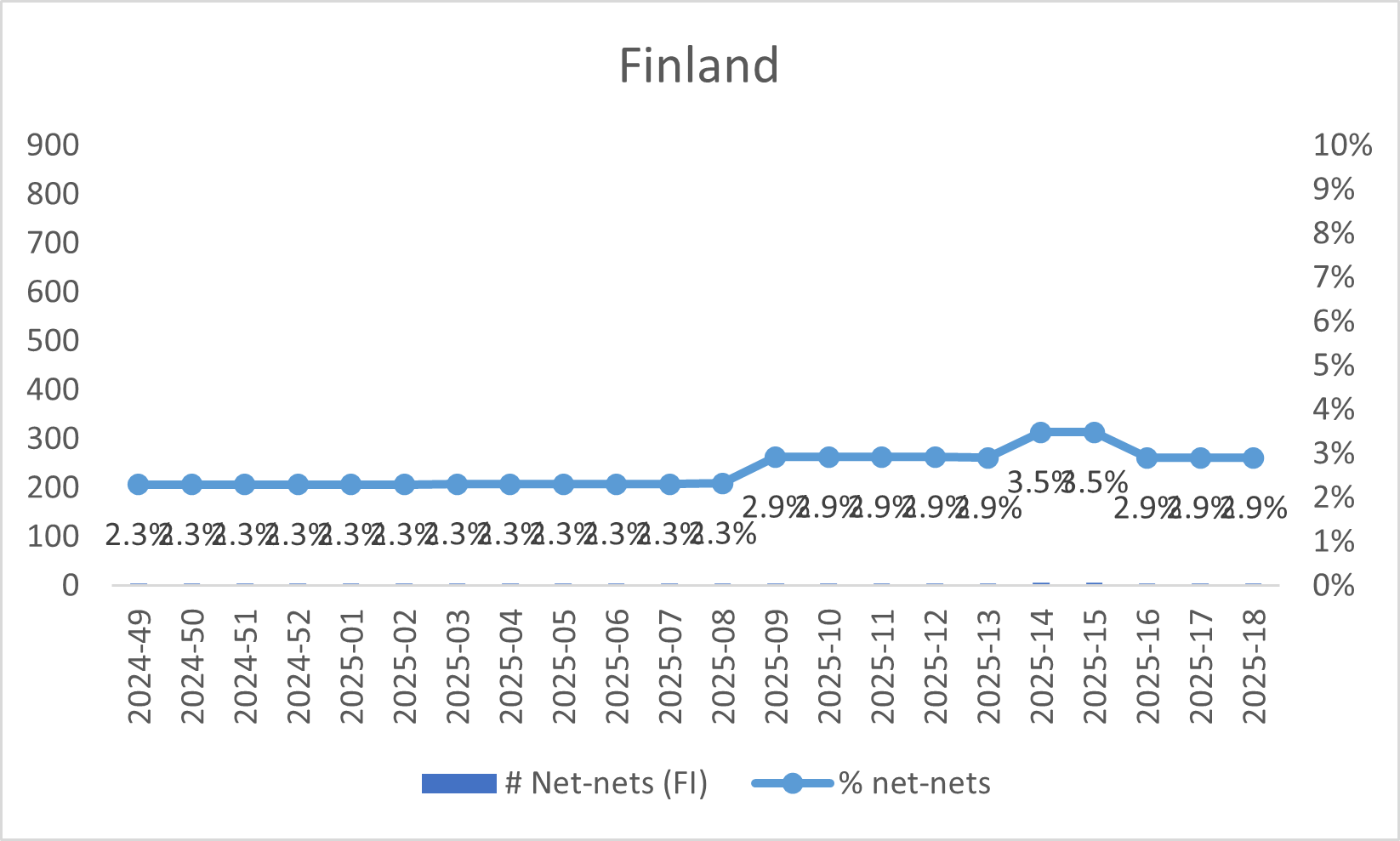

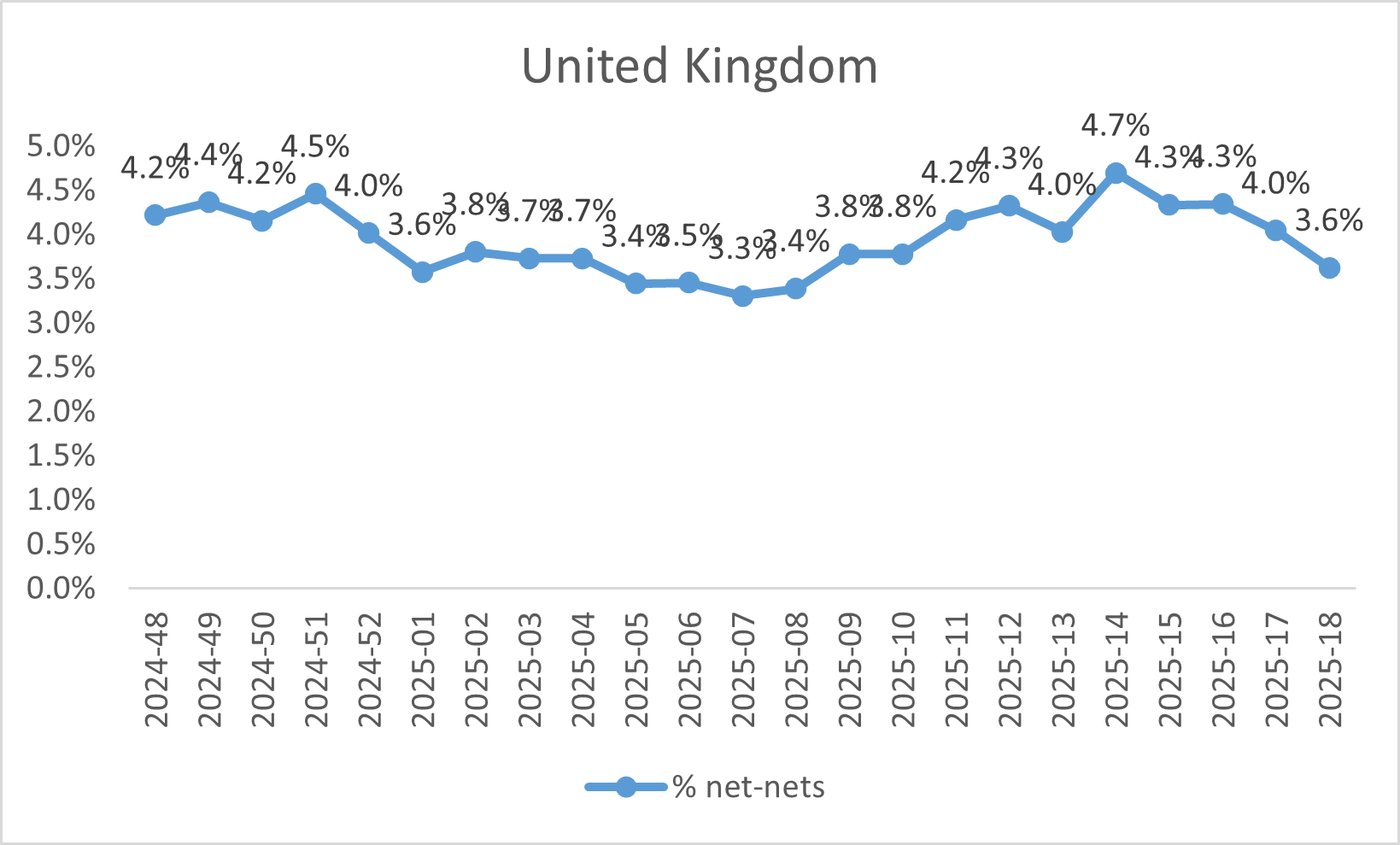

Benjamin Graham suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive. Today’s net-nets, however, are not the same as Graham’s net-nets. Many are un-investable being Chinese RTO’s, loss-making biopharma’s etc. But we do think it is interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable. Below is a net-net screen from Stockopedia.

Headlam Group (HEAD) - Directors Acquire Shares and CEO Exercises Deferred Bonus Option

UK │ P/TB 0.43 │ URL

Headlam Group plc, Europe’s leading floorcoverings distributor, announced that on 1 May 2025, Non-Executive Chairman Stephen Bird purchased 50,000 shares at 81.8p per share, and Non-Executive Director Jemima Bird acquired 12,117 shares at 82.014p per share. Additionally, CEO Chris Payne exercised a nil-cost option, receiving 24,748 shares under the company’s Deferred Bonus Plan, including dividend equivalents. Following these transactions, 4.77 million shares remain held in treasury, with the total voting rights amounting to 80.87 million shares. No immediate business or going concern risks were indicated in the announcement.

IG Design (IGR) - Reports FY25 Results, Eyes DG Americas Exit Amid Tariff Pressures

UK │ P/TB 0.27 │ URL

IG Design Group plc reported a 9% revenue decline and expects FY25 adjusted pre-tax profit of around $1m, in line with earlier guidance. The DG Americas division, heavily impacted by a weak US retail environment, customer bankruptcies, and new tariffs, posted a 12% revenue drop and operating losses. Management is now considering strategic options, including a potential sale of DG Americas. A significant non-cash write-down of the division’s value is anticipated. DG International saw a 3% revenue dip but remained profitable despite supply chain and freight cost challenges. The Group closed the year with $84m net cash and extended its asset-backed lending facility to June 2027. The outlook for DG International is positive, while the future performance of the Group will largely depend on the outcome of strategic actions regarding DG Americas.

Northamber (NAR) - Appoints Matthew Light as Executive Director to Strengthen AV Business

UK │ P/TB 0.44 │ URL

Northamber plc announced the appointment of Matthew Light as Executive Director effective 27 March 2025. Light brings 30 years of experience in the AV and IT sectors, focusing on videoconferencing, networking, and voice technologies. He is currently Managing Director of Tempura Communications, an AV and Unified Communications distributor acquired by Northamber in April 2024. Light will oversee Northamber’s UK AV operations and help leverage synergies across the Group’s AV businesses. He holds 181,818 shares in the company.

Sanderson Design Group (SDG) - Reports FY25 Loss Amid Market Weakness and Goodwill Impairment

UK │ P/TB 0.53 │ URL

Sanderson Design Group plc reported FY25 revenue of £100.4m, down 7.6%, reflecting continued weak consumer demand, particularly in the UK. Adjusted underlying profit before tax fell sharply to £4.4m from £12.2m, while a £16.3m non-cash goodwill impairment linked to the 2016 Clarke & Clarke acquisition resulted in a statutory pre-tax loss of £13.9m. Cash declined to £5.8m from £16.3m, though liquidity remains stable with a £10m undrawn facility. Licensing revenue grew slightly to £11.0m, offsetting some declines in brand and manufacturing sales. The board highlighted progress in cost savings, digitalisation, and strong North American growth potential. Despite near-term market uncertainties, the group maintained its dividend.

Naked Wines (WINE) - Director-Linked Entity Acquires Additional Shares

UK │ P/TB 0.92 │ URL

Naked Wines plc announced that Colebrooke Partners Limited, an entity closely associated with Non-Executive Director Jack Pailing, acquired 50,000 ordinary shares at £0.80 each on 25 April 2025. Following this transaction, Mr. Pailing and his associated entities now hold 873,654 shares, representing approximately 1.18% of the company’s issued share capital. No financial or going concern risks were disclosed in connection with the transaction.

James Cropper (CRPR) - Strategic partnership with HOERBIGER and divests non-core IP assets

James Cropper plc has announced a strategic collaboration with HOERBIGER to jointly develop Ready2Stack™, an integrated bipolar plate (BPP) solution for PEM electrolysers used in hydrogen production. The partnership combines Cropper’s expertise in electrochemistry and coatings with HOERBIGER’s industrial manufacturing and automation capabilities, aiming to reduce costs, improve quality, and accelerate the scalability of green hydrogen production.

On 1 May 2025, James Cropper completed the sale of certain non-core intellectual property assets developed by its Centre for Innovation to an unrelated engineering sector buyer for an initial cash consideration of €1.75 million, with potential additional payments of up to €2.45 million including deferred consideration and royalties over the next nine years. The company retains a royalty stream and license rights to use the technology internally. Proceeds from the sale will support the Group’s growth strategy.

Altheora (ALORA) - €37m Revenue, 5.8% EBITDA Margin, €1.7m Net Loss Amid Strategic Transition in 2024

FRA │ P/TB 0.53 │ URL

2024, Altheora demonstrated resilience and strategic agility in a challenging economic and geopolitical environment. While financial performance remained under pressure, with revenues of €37m, an EBITDA margin of 5.8%, and a net loss of €1.7m, the company made significant strides in implementing its "Confluence 2030" strategic plan. Altheora diversified its customer base and entered new growth sectors including sustainable mobility, aerospace, and energy. Operational excellence initiatives improved production efficiency and quality, while innovation and R&D investments began yielding results. The group maintained a strong focus on low-carbon solutions and strengthened its role in regional industrial revitalization. Key business risks include the pace of market recovery, cost pressures, and the successful execution of its sustainability and diversification strategies. Management, under CEO Bénédicte Durand, emphasized a culture of continuous improvement and environmental responsibility, positioning Altheora for long-term competitive advantage despite short-term profitability challenges.

Herige Industries (ALHRG) - 2024 Results — Strong Focus on Industrial Growth and Profitability

FRA │ P/TB 0.57 │ URL

In 2024, HERIGE Industries reported revenues of €406.1m and an EBITDA of €19.5m, reflecting its sharpened focus on industrial activities following the divestment of its building materials trading division in April. Operating profit reached €4.6m, while net profit stood at €15.4m. The company invested €14.9m during the year, supporting innovation and operational efficiency across its two main segments: industrial carpentry and concrete. HERIGE's workforce averaged 1,686 full-time equivalents. Despite a challenging construction market, the company’s industrial repositioning and strategic investments aim to ensure long-term profitability and sustainability.

Installux Group (ALLUX) – 2024 Annual Report

FRA │ P/TB 0.77 │ URL

In 2024, Groupe Installux reported revenues of €147.6 million, reflecting a slight decrease of 1.3% year-on-year due to lower sales volumes. The group’s operating profit rose by €2.1 million, mainly driven by a €2.5 million increase in gross margin and a €1.6 million reduction in external charges, though offset by higher amortization/provisions (+€1.4 million) and personnel expenses (+€0.8 million). The net income attributable to the Group increased by €1.9 million to €8.4 million. The group maintained robust financial health with equity of €120.7 million and net cash of €44.9 million, an increase of €4.0 million driven by strong operating cash flow (+€19.8 million), despite €11.3 million in investment outflows, including the acquisition of COMEY, and €4.6 million in financing outflows. The aluminium business benefited from a strategic procurement policy, mitigating a 20% rise in aluminium prices starting April 2024. The group highlighted potential market softness continuing into 2025, especially in new construction. Nevertheless, the group continues to invest in digital transformation, R&D, and commercial development to safeguard margins and capture new market share.

Akwel (AKW) – Q1 2025 Turnover Decline and Stable Cash Position

FRA │ P/TB 0.35 │ URL

In Q1 2025, AKWEL reported consolidated turnover of €255.6m, a decrease of -3.0% compared to Q1 2024 (-4.0% at constant scope and exchange rates). This decline reflects lower global automotive production across most key markets, excluding China and Japan. Turnover by region was EMEA €170.7m (-3.8%), America €76.4m (-1.9%), and Asia €8.5m (+2.8%). By product line, Decontamination (+10.4%) and Cooling (+4.5%) grew, while Air (-27.1%), Mechanisms (-8.7%), and Fuel (-2.7%) declined. Net cash excluding lease liabilities rose to €149.6m, up €4.6m from December 2024, despite €8.6m in investments (down from €20.2m in Q1 2024). Due to continued uncertainty in the automotive sector, the group anticipates a revenue decrease in 2025 similar to the decline recorded in 2024.

Centrale del Latte d’Italia (CLI) – Shareholders Approve 2024 Financial Statements and Profit Allocation

FRA │ P/TB 0.90 │ URL

On April 28, 2025, the shareholders’ meeting of Centrale del Latte d’Italia S.p.A. (CLI) approved the 2024 financial statements. Revenues reached €349.7m, up 4.7% from €333.9m in 2023, driven by organic growth and higher sales prices reflecting inflation in the dairy market. EBITDA remained stable at €25.2m, while EBIT rose 11.3% to €9.7m. Net profit increased significantly by 49.4% to €4.4m (€2.9m in 2023). The net financial position improved by €3.9m to €-38m, or €6.2m improvement when excluding share buybacks. The meeting also approved the remuneration policy and authorized a new share buyback plan, replacing the previous authorization.

Delignit AG (DLX) – Revenue and EBITDA Decline in FY 2024, Stable Cash Flow and Solid Balance Sheet

DEU │ P/TB 0.74 │ URL

Delignit AG reported FY 2024 revenue of €65.1m, a decline of 24.3% from the record €86.1m in 2023, in line with guidance (€63m–€67m). EBITDA dropped to €3.8m (5.7% margin), down from €7.1m (8.2% margin) in 2023, primarily due to lower volumes from key OEM contracts and inflation-driven personnel cost increases. However, gross margin improved due to insourcing and cost control measures. Operating cash flow remained robust at €6.0m (vs. €6.8m in 2023), and net cash rose to €7.1m from €5.9m, strengthening the balance sheet with an equity ratio of 78%. For 2025, Delignit guides for moderate revenue growth to €68m and an EBITDA margin between 6–7%, supported by recovery in the LCV market and growth in Technological Applications, despite ongoing macroeconomic and geopolitical uncertainties.

Emak S.p.A. (EM) – Shareholders Approve FY 2024 Results, Dividend of €0.025 per Share Confirmed

ITA │ P/TB 0.73 │ URL

Emak S.p.A. held its AGM on April 29, 2025, approving the FY 2024 financial statements and a dividend of €0.025 per share. Consolidated net sales increased 6.3% to €601.9m (FY 2023: €566.3m). However, EBITDA adjusted fell to €62.2m from €67.9m and EBIT declined significantly to €24.4m (FY 2023: €37.2m). Net profit dropped sharply to €6.5m from €19.9m, mainly due to a goodwill impairment. Normalized net profit was €10.9m. Net financial debt increased to €210.0m (vs. €191.5m), or €165.8m excluding IFRS 16 effects. The meeting also approved executive remuneration policies, the renewal of the board (2025–2027), the appointment of KPMG S.p.A. as auditor (2025–2033), and authorized a share buyback program covering up to 5.49% of share capital. Amendments to the company’s bylaws were also adopted, including flexibility for virtual meetings and governance updates.

Encres Dubuit (ALDUB) — Revenue Stabilization Amidst Ongoing Turnaround Efforts

FRA │ P/TB 0.49 │ URL

Encres Dubuit reported a consolidated revenue of €20.2m for FY 2024, representing a slight increase of 1.26% versus 2023 (€19.9m). At constant exchange rates, sales grew 0.85%. Performance varied across geographies, with revenue growth in Europe (+15.9%) and North America (+22.2%), offset by declines in Asia (-6.2%) and France (-5%).

Key financials (2024 vs 2023):

Revenue: €20.2m (+1.26%)

Gross margin: €11.71m (58% of sales, stable YoY)

Operating result: -€1.44m (vs -€2.22m in 2023)

Net result: -€1.19m (vs -€2.23m in 2023)

Net debt: -€3.84m (net cash position improved from -€3.52m in 2023)

Operating cash flow: -€347k (vs -€451k)

CapEx: €832k

Equity: €19.3m (vs €20.2m in 2023)

Laboratoires Euromedis (ALEMG) - Revenue Growth in 2024 Offset by Exceptional Charges, Resulting in Net Loss

FRA │ P/TB 0.46 │ URL

Laboratoires Euromedis reported a 6% increase in net revenue to €36.2m in FY2024 (FY2023: €34.0m), despite downward pressure on sales prices and increased freight costs. Gross margin remained stable at 26.5% (€9.6m). EBITDA improved significantly but remained negative at -€1.3m (FY2023: -€3.6m). Operating profit turned positive at €0.5m compared to a -€5.7m loss in 2023. However, the company posted a net loss of €6.1m (FY2023: €13.1m net profit), mainly due to a €6m exceptional charge from the full depreciation of receivables linked to Groupe Gaillard, which entered liquidation in April 2025. Net financial debt improved to €7.2m (FY2023: €9.0m) and gearing stood at -43.6%. No dividend was proposed, and the company emphasized ongoing cost management and diversification efforts. Management flagged continued exposure to public tender pricing pressure and external geopolitical risks for 2025.

Guerbet (GBT) - Revenue Growth and Profitability Improve in 2024 Amidst Continued High Debt Levels

FRA │ P/TB 0.88 │ URL

In 2024, Guerbet reported revenue growth of +9% at constant exchange rates (CER), reaching €841.1 million (2023: €785 million). EBITDA rose to €119.4 million (2023: €98.8 million), implying a margin improvement to 14.2% (2023: ~12.6%). Operating income increased sharply to €49.6 million (2023: €38.7 million), and net income climbed to €38.7 million (2023: €13.5 million). Equity improved slightly to €394.2 million (2023: €378.3 million). However, net financial debt also increased to €344.9 million (2023: €335.8 million), keeping the leverage ratio at a relatively high 2.89x EBITDA (2023: 3.40x). Investments moderated slightly to €58.2 million (2023: €62.3 million). Key growth drivers included MRI contrast agents (notably Elucirem™), expansion in Asia-Pacific, and the launch of new AI solutions.

DR. HÖNLE AG (HNL) - Innovative UV Technologies for Battery Manufacturing Introduced at Battery Show Europe 2025

DEU │ P/TB 0.78 │ URL

Dr. Hönle AG will showcase a wide range of modern UV curing devices at the Battery Show Europe in Stuttgart (3–5 June 2025), highlighting solutions for bonding and coating in battery cell contacting systems. Key innovations include the LED Powerline 820 AC IC system, offering high-intensity radiation for fast curing of adhesives in battery modules, and the LED SPOT 100 IC system, ensuring rapid curing of UV protective coatings on battery housings.

Exacompta Clairefontaine (EXAC) – 2024 Financial Results and AGM Decisions

FRA │ P/TB 0.38 │ URL

For the year ended December 31, 2024, Exacompta Clairefontaine reported consolidated revenue of €831.3 million, a slight decrease of 1.4% compared to €843.2 million in 2023. EBITDA amounted to €98.2 million (2023: €115.6 million), and EBIT declined to €45.3 million from €72.1 million in the prior year. Net profit reached €31.5 million, down from €43.1 million in 2023. The group maintained a robust financial position with a net debt of €19.9 million, or a net cash position of €21.8 million excluding lease liabilities under IFRS 16. The equity ratio stood at a solid 64.5%.

In the Paper division, production volumes rose by 1.3%, but sales remained stable as demand for graphic papers continued to decline in line with industry trends. The Processing division experienced weaker demand for traditional paper-based office supplies, particularly in France, leading to restructuring efforts in some production lines.

The parent company posted a net profit of €0.9 million in 2024 (2023: €-11.5 million). The AGM, held on May 27, 2025, approved the financial statements and declared a dividend of €7.50 per share, an increase from €6.70 in the previous year. Shareholders also approved the reappointment of directors and the appointment of new sustainability auditors.

The group highlighted risks related to raw material and energy cost inflation, as well as ongoing structural challenges from digitalization reducing demand for printed products. Looking ahead, the company expects softer demand to continue into 2025, with results anticipated to be lower than 2024 due to persistent cost pressures and market headwinds.

H&R GmbH & Co. KGaA (2HRA) – Preliminary Q1 2025 Results Slightly Improved

DEU │ P/TB 0.38 │ URL

H&R GmbH & Co. KGaA reported preliminary results for Q1 2025, showing a 2.6% revenue increase to €345.8 million (Q1 2024: €337.0 million) and a 5% rise in EBITDA to €22.4 million (Q1 2024: €21.3 million). EBIT improved to €7.7 million and pre-tax earnings (EBT) reached €4.7 million, while net income attributable to shareholders rose to €1.9 million (Q1 2024: €1.5 million). The ChemPharm Refining segment saw EBITDA growth to €13.9 million, while ChemPharm Sales EBITDA declined to €9.7 million; the Plastics division posted a negative EBITDA of €-0.4 million due to weak automotive demand. Operating cash flow turned negative at €-8.1 million, mainly from working capital changes, and free cash flow was €-17.7 million. Despite this, the balance sheet remained solid with an equity ratio of 46.1%. The company reaffirmed its full-year 2025 EBITDA guidance of €85–100 million.

Passat SA (PSAT) - Reports 2024 Revenue Decline and Lower Net Profit Amid Rising Financial Expenses

FRA │ P/TB 0.49 │ URL

In 2024, PASSAT SA reported a consolidated revenue of €62.3 million, down 2.5% compared to 2023. Operating income declined from €3.1 million to €2.8 million, while the net profit attributable to the group decreased to €1.14 million from €2.2 million in 2023, mainly due to higher financial expenses linked to asset depreciation. In France, revenue dropped by 3.2%, but net income rose to €2.86 million from €1.81 million in the previous year, supported by higher financial results. The U.S. subsidiary contributed dividends of €999k, and the BEST OF TV sub-group delivered €26.1 million in revenue and €1.28 million in net profit. The group maintained a healthy balance sheet with no long-term or short-term bank debt. Risks include dependence on key customers (top 5 accounting for 52.2% of sales) and product obsolescence.

The company proposed retaining the 2024 profit in reserves and did not recommend a dividend. PASSAT renewed its share buyback program and proposed the potential cancellation of repurchased shares.

SMT Scharf Reports (S188) - Strong Q1 2025 Revenue Growth and Improved Profitability

DEU │ P/TB 0.45 │ URL

SMT Scharf AG announced a significant increase in Q1 2025 revenue to €22.9m, up 83.2% from €12.5m in Q1 2024, mainly driven by the full consolidation of its joint venture Xinsha and strong growth in the Tunnel Logistics segment. EBIT improved to €1.2m from a loss of €-1.0m in the prior year period, yielding an EBIT margin of 4.4%. Revenue growth was broad-based, with new equipment sales rising to €11.4m (Q1 2024: €4.7m), service revenue increasing to €2.8m (Q1 2024: €1.5m), and spare parts sales reaching €8.7m (Q1 2024: €6.3m). China became the largest market, contributing 41.5% of total sales at €9.5m. Segment-wise, coal mining remained dominant (€14.5m), while mineral mining (€2.8m) and tunnel logistics (€5.2m) showed solid growth. Despite a lower order intake (€13.0m vs. €41.7m in Q1 2024), the company maintained an order backlog of €21.9m. SMT Scharf reaffirmed its 2025 guidance, projecting revenue between €110m and €130m and EBIT between €5.5m and €7.5m.

InTiCa Systems SE (IS7) - Reports Preliminary FY 2024 Results; Final Financial Reports Delayed

DEU │ P/TB 0.66 │ URL

InTiCa Systems SE reported preliminary unaudited figures for fiscal year 2024, posting consolidated revenue of €70.6 million, down 18.7% from €86.9 million in 2023. EBIT came in slightly negative at €-0.6 million, an improvement compared to the revised forecast, while EBITDA was €6.1 million, representing a margin of 8.6%. Revenue declines were significant in both the Industry & Infrastructure (-39.4%) and Mobility (-10.2%) segments. Despite challenges from geopolitical tensions and market volatility, cost-cutting measures positively impacted results. The company ended the year with an order backlog of €77.3 million (down from €99.3 million) and liquid assets of €1.9 million, with additional undrawn credit lines of €3.3 million. The equity ratio stood at 29.8%. InTiCa continues restructuring efforts, particularly targeting new series production orders in e-machinery components and expanding opportunities in Mexico. Final audited financial statements for 2024 are now expected to be published on May 27, 2025.

Lacroix (LACR) - Targets Growth in Heating Networks and Building Management Systems

FRA │ P/TB 0.78 │ URL

LACROIX announced strong momentum in its HVAC (Heating, Ventilation, Air Conditioning) and Building Management Systems (BMS) segments, driven by urbanization, decarbonization, rising energy prices, and supportive public policies like France’s BACS decree. The company’s Environment division, which posted a 10% CAGR from 2021 to 2024, reported accelerating sales in early 2025. LACROIX’s IIoT solutions—covering the entire equipment chain from sensors to secure software—have positioned it as a key supplier for operators such as ENGIE Solutions and DALKIA. In addition to French market growth, LACROIX is expanding across Europe via subsidiaries in Italy and Spain and a channel partner network. For FY 2024, the group reported €636 million in revenue. Management expects 2025 to be a record year for its HVAC segment and continues to advance its 2027 roadmap, emphasizing international growth and delivering cybersecure, scalable solutions. The Q1 2025 revenue report is scheduled for May 15, 2025.

Iberpapel (IBG) - Reports €1.1 Million Net Profit in Q1 2025 Despite Market Pressures

ESP │ P/TB 0.68 │ URL

Iberpapel reported a net profit of €1.1 million for the first quarter of 2025, down from €3.93 million in Q1 2024, amid falling uncoated woodfree paper prices (down 3% year-on-year) and rising energy costs. EBITDA declined to €4.28 million from €7.68 million in the prior-year period. Despite these challenges, revenue increased to €65.82 million (Q1 2024: €62.11 million). Production was paused for six days during the quarter for scheduled maintenance. Notably, Iberpapel’s diversification into packaging, labels, and paper for food and health industries continued to gain traction, representing 30% of total Q1 sales, up from an average of 28.4% in 2024.

Exel Industries (EXE) - Reports Q2 2024–2025 Sales Decline of 3.8%, Maintains Resilience Amid Market Challenges

FRA │ P/TB 0.64 │ URL

EXEL Industries posted Q2 2024–2025 revenue of €281.4 million, down 3.8% year-on-year, mainly due to a 15.7% drop in Agricultural Spraying sales linked to low volumes and market uncertainties, especially in North America. However, Sugar Beet Harvesting sales rose sharply by 47.6%, while Leisure was stable (-0.1%) and Industrial Spraying grew by 7.5%. For the six-month period, group revenue totaled €443.4 million, reflecting a 10% decline versus the prior year. Despite macroeconomic uncertainty and reduced volumes in some segments, the Group reported stable or improving sales in Leisure and Industry and sees early signs of recovery in Agricultural Spraying in Europe. Management reaffirmed its cautious approach, particularly in North America, but highlighted ongoing growth in Industrial Spraying and positive momentum in the Leisure segment. H1 2024–2025 results will be published on May 23, 2025.

Nimbus Group (BOAT) - Weak Q1 2025 sales amid market uncertainty, premium segment remains resilient

SWE │ P/TB 0.98 │ URL

Nimbus Group reported a 13% year-on-year decline in Q1 2025 net sales to MSEK 300, mainly driven by weaker Commercial Sales, while Retail Sales rose slightly. Organic growth was -13%, and EBITA remained negative at MSEK -13. The order book shrank to MSEK 624 from MSEK 789 a year earlier. While Europe and the premium boat segment showed resilience — exemplified by sold-out production of the Nimbus 495—global economic uncertainty, tariffs, and weak consumer sentiment weighed on overall performance. Operating cash flow deteriorated to MSEK -127, though liquidity was strengthened by a MSEK 345 rights issue completed in January. Notably, sales of premium boats in Europe increased, and the North American EdgeWater brand doubled sales, albeit from a weak prior-year base. Risks remain from fluctuating demand, foreign exchange volatility, and continued production under-absorption. CEO Jan-Erik Lindström confirmed his upcoming retirement, and the company expanded its retail footprint in Stockholm.

Harboes Bryggeri (HARB) - Q3 2024/25 sees revenue growth but lower margins; full-year guidance cut

DK │ P/TB 0.81 │ URL

In Q3 2024/25, Harboes Bryggeri maintained revenue growth, supported by increased volumes in Denmark and export markets, which offset the continued phase-out of unprofitable contracts in Germany. However, profitability weakened due to higher production costs—partly linked to the ramp-up of a new production line—as well as increased sales and distribution expenses. The EBITDA margin fell to 6.8%, below both expectations and the company’s financial target. As a result, Harboe downgraded its full-year guidance, now expecting EBITDA of DKK 140–150m (previously DKK 160–180m) and pre-tax profit of DKK 50–60m (previously DKK 70–90m). Management emphasized that the current margin pressure is viewed as temporary, with recent investments and cost optimization efforts expected to improve efficiency and competitiveness in the coming years.

HKFoods (HKFOODS) - Evaluating sale of Polish bacon unit to strengthen balance sheet

FIN │ P/TB 0.68 │ URL

HKFoods has initiated a strategic review of its bacon production unit in Świnoujście, Poland, which may lead to a sale as part of ongoing efforts to streamline group operations and reinforce the balance sheet. The Polish unit, generating estimated 2025 net sales of EUR 70 million and employing around 300 people, is the latest focus following previous divestments in the Baltics, Sweden, and Denmark. The company emphasized that no further comments will be provided until the review progresses. The move reflects HKFoods' broader restructuring aimed at improving financial flexibility after years of portfolio adjustments.

Ilkka (ILKKA) - Media business merger with Kaleva completed, gains EUR 4m & management team change announced & Ilkka Q1 2025: Revenue Growth Offset by Weak Profitability Amid Restructuring

FIN │ P/TB 0.75 │ URL / URL / URL

Ilkka has completed the merger of its media business with Kaleva Media, transferring its subsidiary I-Mediat Oy to Kaleva365 Oy in exchange for a 35% ownership stake, with Kaleva retaining 65%. The merged entity now controls 22 strong regional media brands with a combined 2024 pro-forma revenue of EUR 62m and EBITDA of around EUR 4m. The transaction strengthens regional media and supports future digital investments. Ilkka’s share in Kaleva365 is valued at EUR 9m, aligning with the agreed value of I-Mediat. The deal results in an estimated EUR 4m profit for Ilkka and the media business will now be reported as discontinued operations. All employees continue under the new ownership, and Ilkka remains an active minority owner committed to developing the new company.

Ilkka has finalized the previously announced media business restructuring with Kaleva, transferring its subsidiary I-Mediat Oy to Kaleva365 Oy in exchange for a 35% ownership stake. As a result, Media Services Business Director Timo Ranta will leave the Ilkka management team after more than seven years of service. The remaining management team will focus on the continued development of the group's core business, Summa Collective, which includes marketing, communication, and digital services companies operating in Finland, Sweden, and the Middle East. Ilkka's CEO emphasized the ongoing commitment to developing the joint media venture while strengthening the group's technology and marketing services.

Ilkka reported Q1 2025 revenue of €9.4 million, up 21.1% year-over-year, mainly driven by growth in subscription-based technology services and the acquisition of Profinder. However, adjusted operating profit remained negative at -€226 thousand (-2.4% margin), while reported operating loss widened to -€1.4 million due to restructuring and acquisition-related costs. Pre-tax loss totaled -€1.4 million, significantly below the prior year’s profit. The company’s media business was divested to Kaleva365 Oy (Ilkka retains a 35% stake) as part of a strategic shift towards digital marketing and technology services. Despite cost pressures and increased financial expenses, Ilkka maintains a strong balance sheet with an equity ratio of 84.6% and net cash position. The company expects both revenue and adjusted operating profit from continuing operations to improve in 2025, with additional contributions from its associate Kaleva365 and dividend income from Alma Media.

Tecnotree (TEM1V) - Q1 2025: Modest Revenue Growth, Strong Free Cash Flow and Strategic Market Shift & Wins Multi-Million Euro Digital BSS Deal in the Netherlands

Tecnotree reported Q1 2025 net sales of €16.9 million (+3.7% YoY), supported by increased license revenues and progress in shifting toward recurring revenue models. Operating profit grew slightly to €4.5 million, while the operating margin remained stable at 26.9%. TEM1V achieved a notable turnaround in free cash flow, generating €1.0 million compared to -€4.7 million a year earlier, driven by cost optimisation and improved receivables collection (DSO reduced from 216 to 155 days). Despite a 6% YoY decline in the order book to €70.3 million, Tecnotree increased order intake in Europe & the Americas, reducing exposure to high-risk currencies (15% of revenue vs. 45% last year). Guidance for 2025 includes low to mid-single digit net sales growth, at least 200 basis points margin expansion, and free cash flow over €4 million.

Tecnotree has signed a new multi-year agreement with a private network service provider in the Netherlands to supply its digital BSS platform and AI/ML products. The contract, representing less than 10% of Tecnotree’s 2024 revenue, strengthens the company’s European market presence and highlights continued demand for its digital transformation solutions. The deal will not impact Tecnotree’s existing 2025 financial guidance.

K-Fastigheter (KFAST) - Sells Property Portfolio to Joint Venture K-Fast Kilen AB & Q1 2025: Strong property management profit, strategic portfolio shifts

K-Fastigheter has sold a large residential property portfolio in Gävle and Uppsala to its joint venture K-Fast Kilen AB (51% K-Fastigheter, 49% Kilenkrysset). The deal includes 288 apartments under management, 133 under construction, and a pipeline of 418 units either permitted or planned. The agreed property value totals 1,036 msek, with a book value of 1,126 msek as of March 31, 2025. The transaction will provide a net liquidity inflow of ~220 msek upon completion (April 30). The total portfolio, when fully built, is expected to reach a market value of ~2,265 msek with an annual rental value of 125 msek.

K-Fastigheter reported Q1 2025 rental income of 161.2 msek (146.8), with profit from property management rising to 34.1 msek (25.3), driven by a 96.4% occupancy rate. However, group profit fell to -5.3 msek (35.5), mainly due to lower earnings from construction (-66% YoY). Major portfolio shifts included the Brinova deal (K-Fastigheter now owns 57.6% of Brinova) and the sale of Gävle and Uppsala properties to K-Fast Kilen AB. Net investments totaled 487.9 msek, with investment properties valued at 16,062 msek. The company reaffirmed its focus on construction and capital efficiency as part of its 2025–2028 business plan.

The writer may own shares of the companies mentioned. This communication is for informational purposes only. AI helped us with this. Check important info.