The Deep Value Week – 2026/19

Companies mentioned:

· Datron - New headquarters and stronger software push highlight upside potential

· Datron - Audited 2025 results and Q1 2026 figures confirm profitable start to the year

· Datron - Related party to CEO buys shares on Xetra

· HERIGE Industries - Q1 revenue returns to growth despite adverse weather

· ElringKlinger - Q1 margin improvement and E-Mobility growth support transformation path

· EuroGroup Laminations - AGM approves 2025 accounts, new board appointments and treasury-share authorization

· Portmeirion Group - Michael Scheepers appointed CEO as Mike Raybould steps down

· Portmeirion Group - 2025 results show transformation progress but profitability hit by US tariffs

· Taylor Wimpey - Weekly buyback transactions completed for cancellation

· Robinson - Sale of Hipper House surplus property completed

· IG Design Group - CEO designate buys 1.27% stake

· IG Design Group - Crucible Clarity Fund raises holding above 5%

· AIREA - AGM update highlights stronger 2025 profit and positive start to 2026

· Duell Corporation - Tomi Virtanen appointed CEO after interim period

· Metsä Board - Strategic collaboration with HEIDELBERG targets packaging innovation

· Rottneros - Q1 loss widens as lower pulp prices and weaker USD offset cost cuts

· Universal Electronics - Leviticus Partners discloses 5.1% stake

· TrueBlue - Q1 revenue growth and cost discipline offset by continued net loss

· TrueBlue - Removal of Preferred Stock Purchase Rights from NYSE listing

· TrueBlue - Invesco cuts ownership below 5%

· Mercer International - German lenders waive 2026 leverage covenant and tighten facility terms

· Mercer International - Reports weaker Q1 results and outlines liquidity actions

· Tronox - Q1 results show revenue growth but elevated leverage and cash burn

· Resources Connection - Announces planned board transition and governance updates

· Valhi - Q1 earnings decline as Chemicals segment profitability weakens

· Unifi - Q3 profitability improves despite lower sales

· PLAYSTUDIOS - Transfers Nasdaq listing and receives second bid-price compliance period

· Natural Alternatives - Expands TriBsyn applications across functional nutrition categories

· Chicago Rivet & Machine - Reports Q1 loss as sales decline

· Key Tronic - Q3 revenue declines but operating efficiency improves

· AdvanSix - Q1 sales rise but earnings turn negative on cost headwinds

· AdvanSix - Assesses Hopewell ammonia expansion for DEF market

· Bowim - Preliminary Q1 profit improves despite lower sales

· Lena Lighting - Supervisory Board recommends approval of 2025 reports and dividend

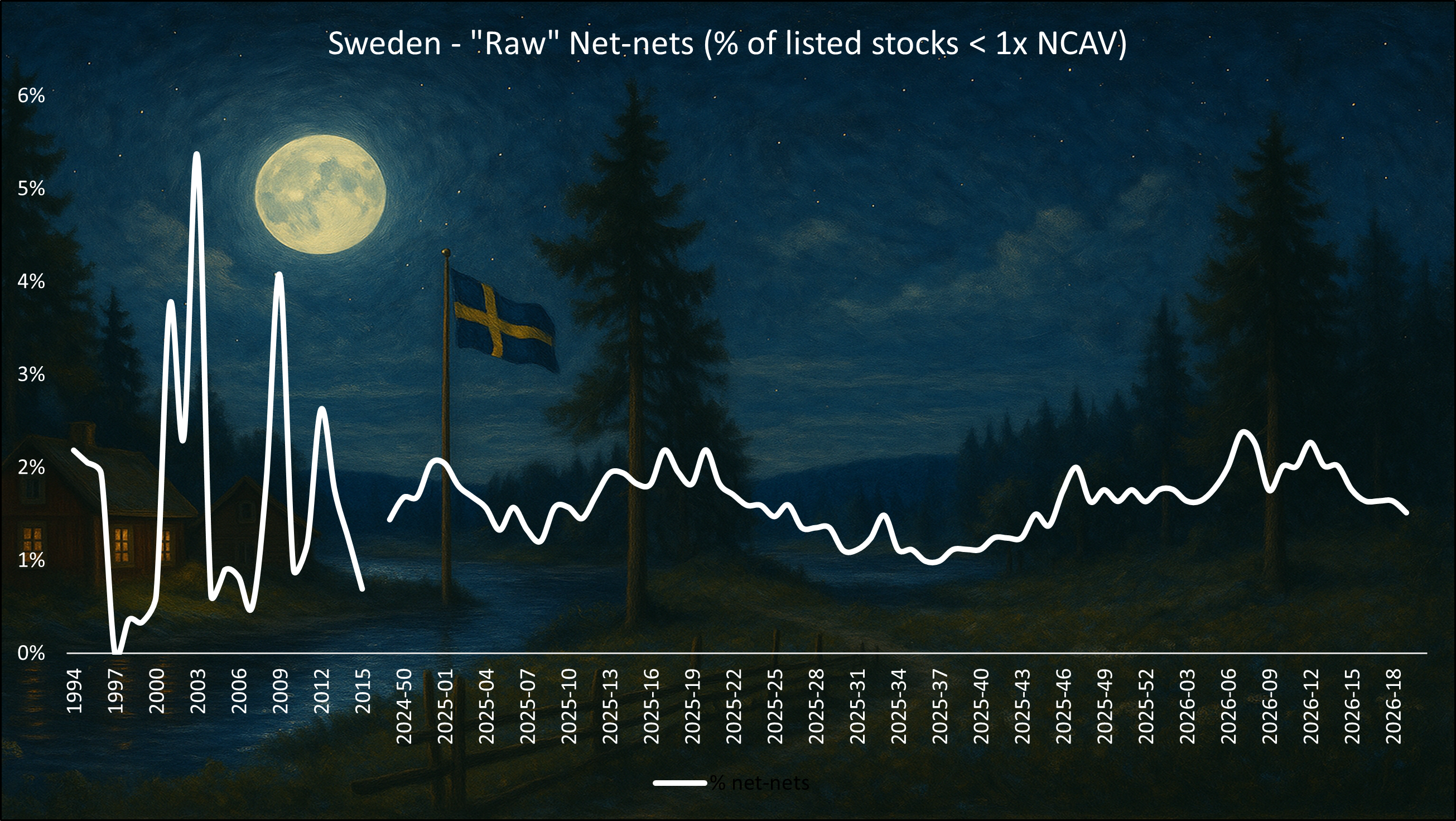

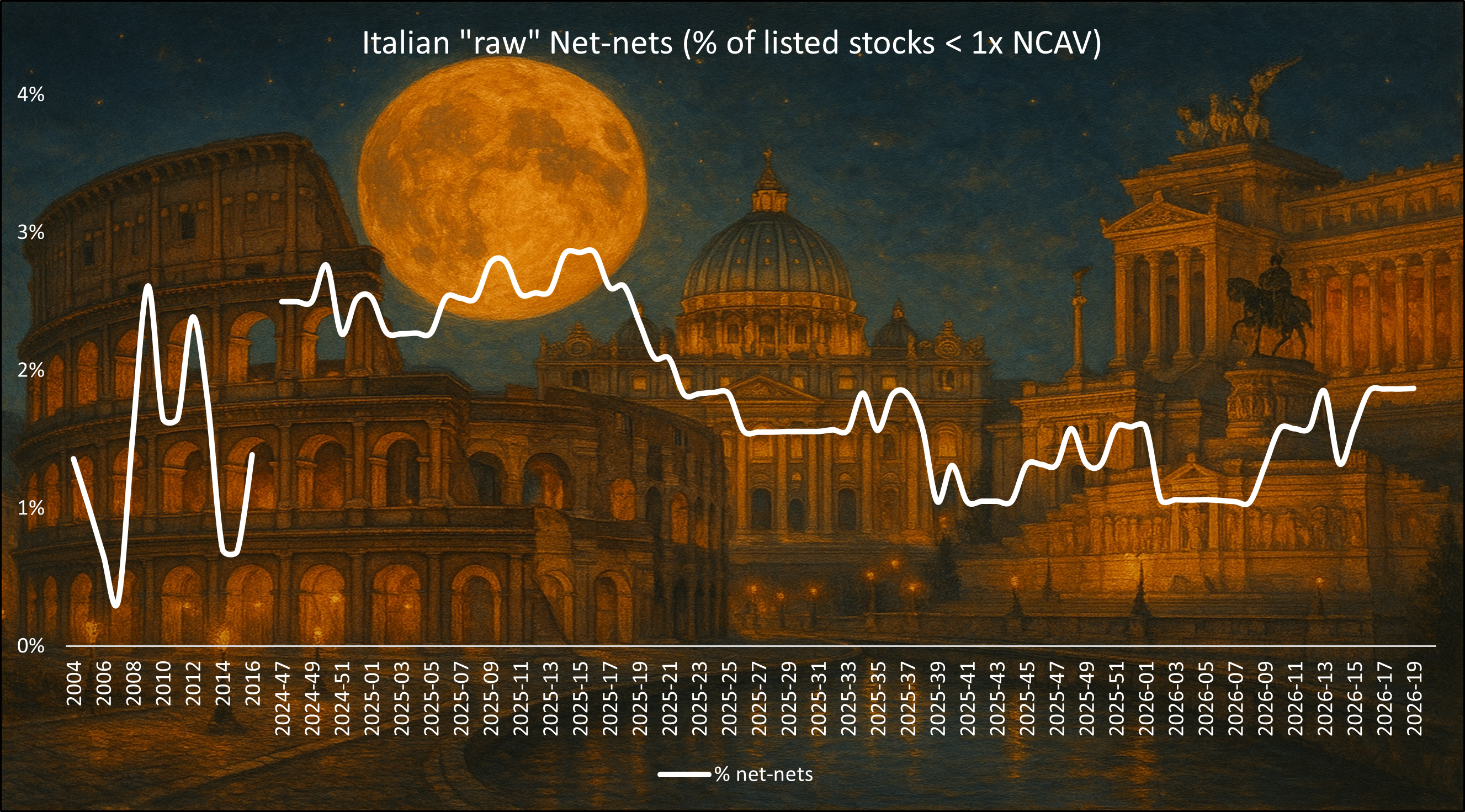

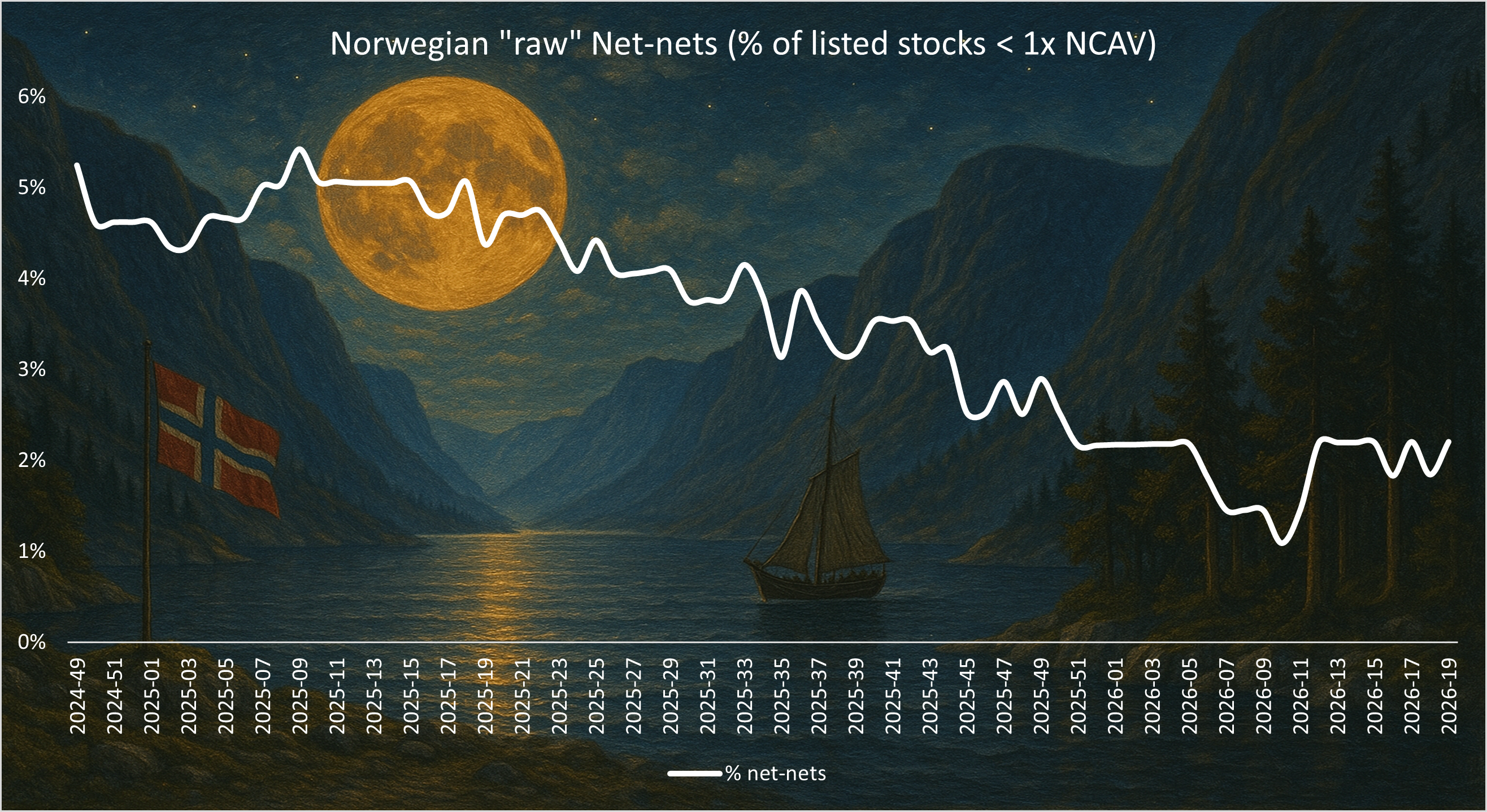

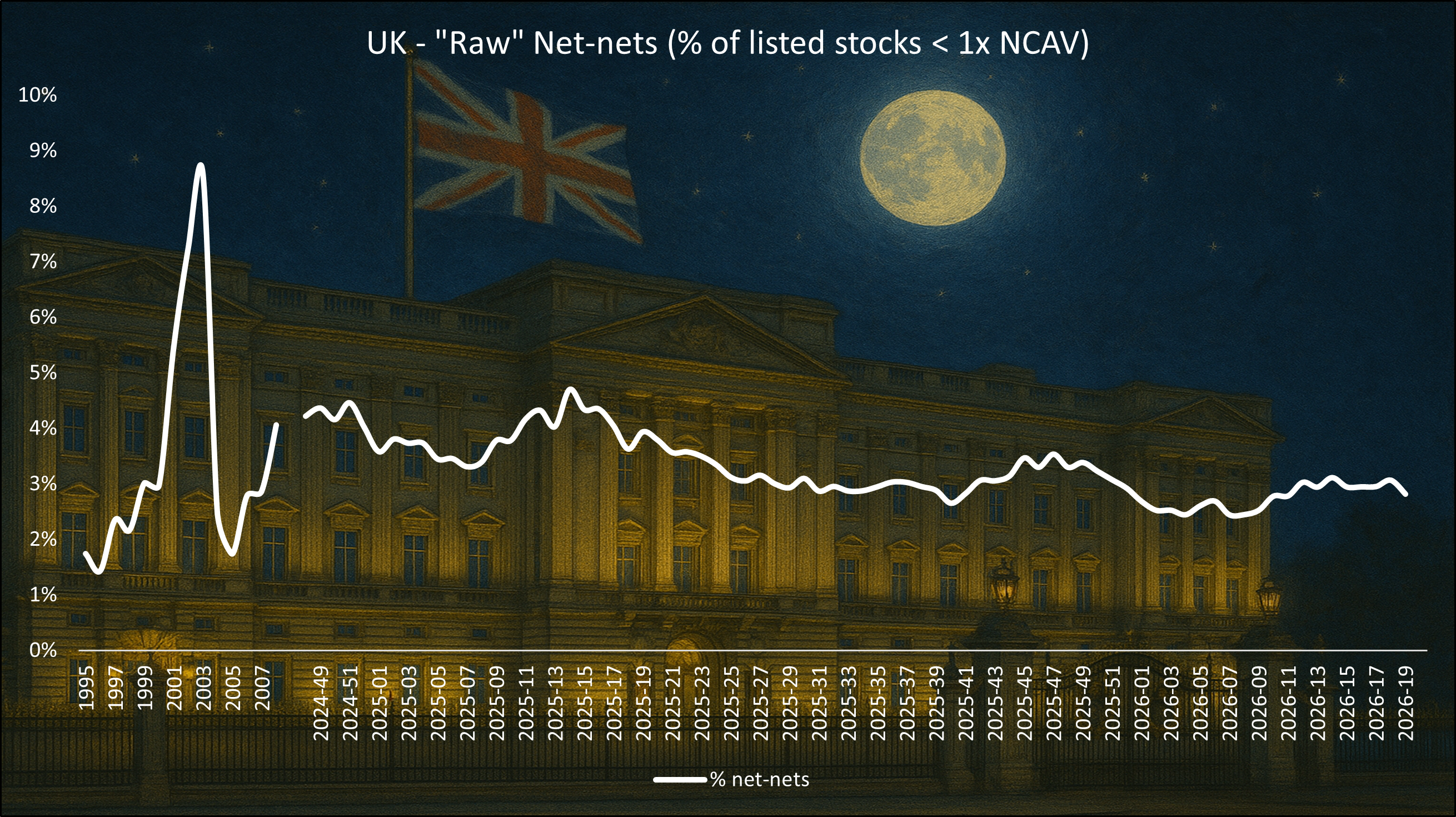

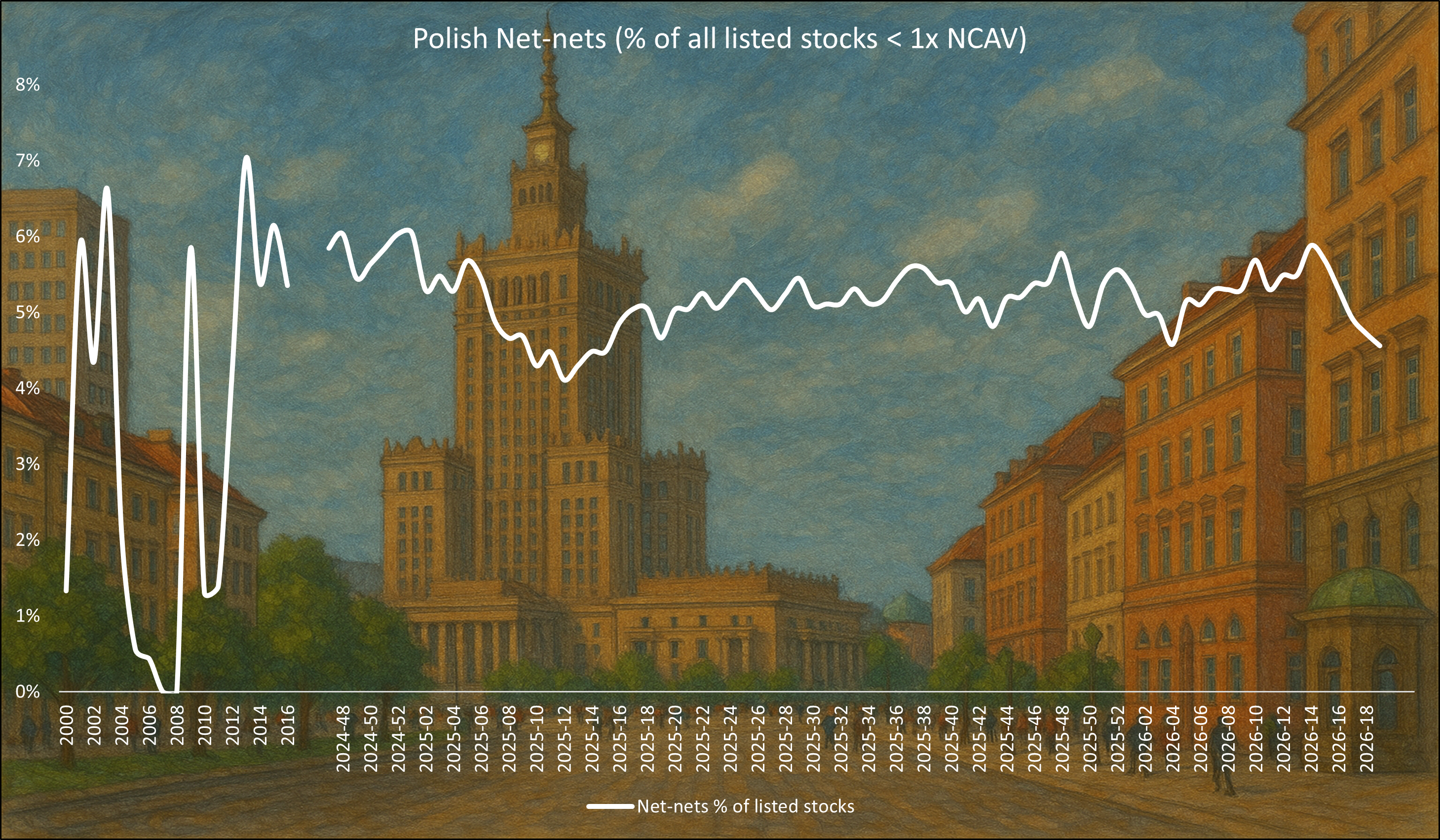

“Graham’s Geiger counter”

Benjamin Graham suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive. Today’s net-nets, however, are not the same as Graham’s net-nets. Many are un-investable being Chinese RTO’s, loss-making biopharma’s etc. But we do think it is interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable.

The writer may own shares in some the companies mentioned below. This communication is for informational purposes only. It is our way of tracking the weekly happenings in our world of deep value. AI helped us with part of this. Check important info.

Datron - New headquarters and stronger software push highlight upside potential

2026-05-08 │ P/TB 0.72 │ Market 5 │ Sector 4 │ URL

May 8, 2026 The relocation from four sites into one new facility required a record investment of around €47m, materially expanding the balance sheet, with liquidity of €5.43m versus bank debt of €30.58m, but management aims to reduce this debt through fixed annual repayments of €2m plus a variable component. While reported 2025 EBIT was only €0.56m due to relocation-related special effects, adjusted EBIT was €3.07m, and order intake rose almost 14% to €63.44m, suggesting good demand from customers in areas such as medical technology, aerospace, toolmaking and semiconductors. A key strategic lever is the broader commercialization of the “Datron next” control software, where CEO Michael Daniel said the company’s story will be that its software share should triple over the coming years; Solventis expects digital services to rise from a likely low single-digit share to 10–15% over the medium term, which should support margins. For 2026, Datron guides for revenue of €63–69m and an EBIT margin of 5.0–8.0%, equal to EBIT of €3.2–5.5m; after Q1 EBIT of €0.82m, management expects Q2 EBIT of €0.9–1.8m, implying H1 EBIT of around €1.7–2.4m. Daniel indicated that reaching the upper end of the EBIT guidance range may be possible, but also cautioned that economic conditions are changing quickly and that he may ultimately be satisfied if revenue lands around €66m. Looking further ahead, Datron could gain additional momentum from acquisitions, particularly in spindles, while management also signals sustainably attractive dividend payout ratios and plans to intensify investor-relations activity.

DATRON AG - Audited 2025 results and Q1 2026 figures confirm profitable start to the year

2026-05-07 │ P/TB 0.72 │ Market 5 │ Sector 4 │ URL

May 7, 2026 DATRON AG published its audited 2025 consolidated results and Q1 2026 figures, confirming the preliminary numbers released in February and reporting 2025 revenue of €60.2m, broadly stable versus €60.6m in 2024, with operating EBIT of €3.1m and operating EPS of €0.37. Including one-off expenses related to the move to the new headquarters in Ober-Ramstadt, reported EBIT was €0.6m and EPS was negative at €-0.07, while management and the supervisory board will propose a dividend of €0.10 per share at the virtual AGM in June 2026. Q1 2026 developed according to plan, with revenue rising to €15.5m from €14.3m, order intake increasing to €19.6m from €16.5m, EBIT improving to €0.8m from €0.8m, and EPS rising to €0.09 from €0.06. The 2026 guidance remains unchanged, targeting revenue and order intake of €63–69m, an EBIT margin of 5.0–8.0%, and EPS of €0.40–0.80. For Q2 2026, DATRON expects revenue and order intake of around €16.0–18.0m, EBIT of €0.9–1.8m, and EPS of €0.10–0.25.

DATRON AG - Related party to CEO buys shares on Xetra

2026-05-07 │ P/TB 0.72 │ Market 5 │ Sector 4 │ URL

May 7, 2026 DATRON AG disclosed a directors’ dealing by PCI Private Capital Investment GmbH, a company closely related to CEO Michael Daniel, involving the purchase of DATRON shares on Xetra. The transactions were executed at €7.30 per share and comprised three separate purchases with volumes of €12,972.10, €4,058.80 and €1,219.10, corresponding to an aggregated purchase volume of €18,250.

HERIGE Industries - Q1 revenue returns to growth despite adverse weather

2026-05-05 │ P/TB 0.54 │ Market 5 │ Sector N/A │ URL

May 5, 2026 HERIGE Industries reported Q1 2026 revenue of €100.5m, up 3.0% versus €97.6m in Q1 2025, marking a return to growth despite particularly unfavorable weather conditions at the start of the year across the group’s activities. Industrial Joinery revenue increased 1.0% to €59.0m, as early-quarter production was heavily affected by weather but partly offset by a favorable calendar effect, while construction-site activity remained broadly resilient. The Concrete Industry division grew 7.6% to €34.9m, supported by good performance in ready-mix concrete from both volumes and pricing, following tariff increases implemented at the beginning of the year to offset higher raw-material costs; prefabrication also remained well oriented in volume and benefited from the ramp-up of lower-carbon concrete ranges, with Vitaliss® ABA+ products exceeding 25% of total volumes. Looking ahead, HERIGE said the sector recovery remains closely tied to a restart in single-family housing construction and dependent on lasting structural measures, including support for energy renovation, simpler regulation and stable public schemes. The company noted that the Jeanbrun Relance Logement initiative signals support for the sector, but short-term visibility remains limited, while geopolitical tensions continue to create uncertainty around energy and raw-material costs. Against this backdrop, HERIGE will continue focusing on operational performance to support the gradual market recovery and strengthen long-term competitiveness.

ElringKlinger - Q1 margin improvement and E-Mobility growth support transformation path

2026-05-07 │ P/TB 0.76 │ Market 5 │ Sector 5 │ URL

May 7, 2026 ElringKlinger reported a solid start to 2026, with Q1 revenue increasing to €430.0m from €423.1m, while organic revenue rose 4.7% despite weaker global and European vehicle production and negative currency effects of €9.7m. Growth was driven mainly by the ramp-up of high-volume E-Mobility contracts, where sales increased to €38.1m from €26.8m, while the broader Original Equipment segment was slightly down at €280.0m, the Aftermarket business grew 7.6% to €109.8m, and Plastics Technology rose slightly to €39.9m. Profitability improved materially, supported by STREAMLINE and SHAPE30 measures, with gross margin up 260 bps to 27.2%, adjusted EBIT rising 41.9% to €29.1m, and the adjusted EBIT margin reaching 6.8% versus 4.9% a year earlier, placing the group at the upper end of its 2026 target corridor. Capex was reduced to €21.3m from €45.0m after the recent investment cycle, while operating free cash flow remained negative at €-109.4m due to the ongoing ramp-up in E-Mobility and related working-capital needs, and the adjusted net debt ratio was stable at 2.1x. ElringKlinger also launched SHAPE2EMPOWER, a new organizational phase intended to improve speed, customer proximity and efficiency by strengthening responsibility in the business areas and simplifying decision-making structures. The company confirmed its full-year 2026 outlook, expecting slight organic revenue growth, an adjusted EBIT margin of around 6–7%, slightly positive operating free cash flow, and an adjusted net debt ratio of 1.0–2.0x. Management also confirmed the group’s medium-term outlook and said the Q1 results show increasing effectiveness from the transformation measures.

EuroGroup Laminations - AGM approves 2025 accounts, new board appointments and treasury-share authorization

2026-05-04 │ P/TB 0.51 │ Market 4 │ Sector 4 │ URL

May 4, 2026 EuroGroup Laminations’ ordinary shareholders’ meeting approved the 2025 separate financial statements, reviewed the consolidated financial statements and CSRD sustainability reporting, and approved all agenda items, with shareholders representing 74.27% of total voting rights present or represented at the meeting. At group level, revenue declined to €831.0m from €869.4m, adjusted EBITDA fell to €88.7m from €116.0m, EBIT decreased to €22.6m from €65.7m, and consolidated net profit was broadly breakeven at €-0.1m versus €36.5m in 2024, while net financial debt improved slightly to €219.4m from €225.5m. The AGM appointed a new seven-member Board of Directors chaired by Sergio Iori for the period until approval of the 2028 accounts, and appointed a new Board of Statutory Auditors chaired by Luigi Emilio Garavaglia. Shareholders also approved the remuneration report, revoked the 2023–2025 stock option plan subject to waivers by option holders, revoked the Performance Shares Plan 2025–2027, and authorized the purchase and disposal of treasury shares for up to 10% of outstanding shares over 18 months, including for extraordinary transactions, incentive plans and share-liquidity support. No outlook or guidance was provided in the AGM release, although the company reiterated that it had an E-Mobility Solutions order backlog of around €2.7bn and a pipeline of €2.1bn.

Portmeirion Group - Michael Scheepers appointed CEO as Mike Raybould steps down

2026-05-06 │ P/TB 0.31 │ Market 5 │ Sector 5 │ URL

May 6, 2026 Portmeirion Group announced the appointment of Michael Scheepers as Group CEO, succeeding Mike Raybould, who will step down from the CEO role and the board on May 11, 2026 after nine years with the company. Scheepers joined Portmeirion in December 2025 as Group Brand and Commercial Director as part of the group’s succession planning and previously spent more than nine years at Le Creuset, including six years as Regional CEO across Europe, the Middle East, Africa and India, where he led brand elevation, commercial performance and transformation in the premium home and lifestyle category. At Portmeirion, he has led global ecommerce, own retail and brand marketing teams, with responsibility for the UK sales division, and has worked closely with the board as part of the senior leadership team. Chairman Peter Tracey thanked Raybould for steering the group through challenging periods including COVID and US tariffs, while highlighting Scheepers’ experience in premium brand transformation and commercial execution. Looking ahead, Portmeirion said it will continue to focus on accelerating its strategic transformation goals of returning to growth, improving performance, maintaining a “fortress balance sheet” and elevating its heritage brands to a wider global consumer base. Scheepers said he sees global opportunities ahead and aims to deliver long-term value for stakeholders as the group launches and executes its new strategic plans.

Portmeirion Group - 2025 results show transformation progress but profitability hit by US tariffs

2026-05-06 │ P/TB 0.31 │ Market 5 │ Sector 5 │ URL

May 6, 2026 Portmeirion Group reported 2025 revenue of £91.1m, broadly unchanged from £91.2m in 2024 and up 1% at constant currency, as positive trading across most of the business was offset by US tariff disruption in the group’s largest and most profitable market. Excluding the US, group sales rose 8.6% at constant currency, with International markets up 14.3% and South Korea up 25.6%, while strong Q4 sell-through of redesigned Christmas ranges, particularly online, provided early evidence of progress from the group’s onshoring and product-refresh strategy. Profitability deteriorated materially, with a headline loss before tax of £3.6m versus a £1.1m profit in 2024, and a statutory loss before tax of £7.2m after a £2.9m inventory write-down and £0.7m of restructuring costs; net debt increased to £17.5m from £12.1m, and no dividend was proposed as management prioritizes a stronger “fortress balance sheet.” The group highlighted progress under its “Elevating Portmeirion” strategy, including inventory clearance, factory improvements, the planned disposal of non-core Wax Lyrical, a new licensing deal with Ashley Wilde, bringing the US Amazon sales team in-house, and leadership changes including Michael Scheepers’ planned promotion to CEO in May 2026. Looking ahead, Q1 2026 revenue was ahead of the prior year, with growth in the US and International markets, and management said early progress against the transformation plan is encouraging. Portmeirion remains cautiously optimistic but noted continued macro uncertainty, weak consumer confidence and trade-shock risk, while any proceeds from its $3.0m US tariff refund claim and $0.8m ERC claim would be used to reduce net debt.

Taylor Wimpey - Weekly buyback transactions completed for cancellation

2026-05-07 │ P/TB 0.70 │ Market 5 │ Sector 2 │ URL

May 7, 2026 Taylor Wimpey announced that it purchased a total of 6,894,139 ordinary shares through Citigroup Global Markets during the period from April 30 to May 6, 2026, as part of its share buyback activity. The purchases were executed on the London Stock Exchange, with 914,702 shares bought on April 30 at a volume-weighted average price of 77.18p, 816,526 shares on May 1 at 78.60p, 2,904,916 shares on May 5 at 79.11p, and 2,257,995 shares on May 6 at 82.20p. The company intends to cancel the purchased shares. Following the transactions, Taylor Wimpey holds 32,084,423 ordinary shares in treasury and has 3,499,328,636 shares in issue excluding treasury shares, which also represents the total number of voting rights.

Robinson - Sale of Hipper House surplus property completed

2026-05-05 │ P/TB 0.93 │ Market 5 │ Sector N/A │ URL

May 5, 2026 Robinson announced the completion of the sale of its Hipper House surplus property, with exchange of contracts and completion both taking place on May 1, 2026. The consideration due on completion was £760k, while Robinson has committed to pay future costs of up to £30k, resulting in net proceeds of £730k that will be used to reduce current bank debt. The property generated rental income of £25k in 2025 and had a book value of £317k as of December 31, 2025, implying the sale was completed materially above carrying value. Robinson reiterated that its intention remains to realise value from surplus property disposals over time and use the proceeds to reduce indebtedness and develop its packaging business.

IG Design Group - CEO designate buys 1.27% stake

2026-05-08 │ P/TB 0.75 │ Market 5 │ Sector N/A │ URL

May 8, 2026 IG Design Group announced that Gerald Kuehr, the company’s Chief Executive Officer Designate, purchased 1,246,424 ordinary shares on May 7, 2026 at 69p per share. The transaction had a total value of approximately £860k and was conducted on the London Stock Exchange. Following the purchase, Kuehr’s beneficial holding is 1,246,424 ordinary shares, representing 1.27% of IGR’s issued share capital.

IG Design Group - Crucible Clarity Fund raises holding above 5%

2026-05-08 │ P/TB 0.75 │ Market 5 │ Sector N/A │ URL

May 8, 2026 IG Design Group disclosed a major shareholding notification showing that Crucible Clarity Fund PLC increased its voting rights in the company to 5.02% from a previously notified 4.02%. The threshold was crossed on May 7, 2026, and IG Design Group was notified on May 8, 2026. Crucible Clarity Fund now holds 4,933,668 direct voting rights attached to ordinary shares, with no reported exposure through financial instruments. The notification states that Crucible Clarity Fund is not controlled by any natural person or legal entity and does not control any other undertaking holding a direct or indirect interest in IG Design Group.

AIREA - AGM update highlights stronger 2025 profit and positive start to 2026

2026-05-06 │ P/TB 0.67 │ Market 5 │ Sector N/A │ URL

May 6, 2026 AIREA said at its AGM that 2025 was a year of progress, with sales up 1.0% despite global economic and geopolitical challenges, while operating profit increased 32.0% to £0.9m, supported by an improved product mix and continued cost discipline. Cash management was strong, and following the divestment of the group’s investment property, all bank debt was fully repaid, materially strengthening the balance sheet. AIREA is proposing a dividend of 1.0p per share, up 66.7%, in line with its progressive dividend policy. The group continued to invest in its new manufacturing facility, with total investment of £6.8m, and expects the facility to become fully operational in the coming months, initially running in parallel with the existing facility through the busy summer period before the old site is decommissioned. Looking ahead, AIREA reported an encouraging start to the new financial year, with revenue for the four months to April 30, 2026 up 7.0% year-on-year. While macroeconomic conditions remain uncertain and the board remains mindful of geopolitical risks, including in the Middle East, management said it remains confident in the group’s prospects for the year ahead and in delivering sustainable long-term shareholder value.

Duell Corporation - Tomi Virtanen appointed CEO after interim period

2026-05-07 │ P/TB 0.25 │ Market 4 │ Sector 3 │ URL

May 7, 2026 Duell Corporation announced that its Board of Directors has appointed Tomi Virtanen as CEO with immediate effect, after he had served as interim CEO since March 5, 2026 and previously led the company’s logistics operations from the beginning of the year. Virtanen holds a master’s degree in engineering and has broad international leadership experience, including CEO roles, with a track record in change management, profitable-growth execution, supply-chain management and aftermarket businesses. Duell said the CEO’s focus will be to restore profitable growth, strengthen and secure the company’s market position in target markets, and improve working-capital efficiency. The company noted that the market has been challenging in recent years, with global crises affecting demand and procurement-channel complexity, while seasonal swings and volatile consumer behaviour require agile execution and efficient supply-chain management. Chair Anna Hyvönen said Virtanen’s international operating experience and understanding of supply-chain management, distributor sales and customer-oriented operations provide a strong basis to develop the company and execute its strategy. No numerical outlook or guidance was provided, but Virtanen said Duell has a strong foundation and opportunities to further develop operations to better respond to changing market demands.

Metsä Board - Strategic collaboration with HEIDELBERG targets packaging innovation

2026-05-07 │ P/TB 0.72 │ Market 4 │ Sector 4 │ URL

May 7, 2026 Metsä Board announced a strategic collaboration with Heidelberger Druckmaschinen AG, combining Metsä Board’s expertise in premium lightweight fresh-fibre paperboards with HEIDELBERG’s offset, flexographic, digital printing and converting technologies. The partnership aims to strengthen the end-to-end packaging production value chain by developing innovative packaging solutions that improve operational performance, production workflows and the consumer experience. The collaboration will include joint R&D projects, pilot production runs and customer demonstrations at HEIDELBERG’s Print Media Centres as well as Metsä Board’s Excellence Centre and Design Studios. Metsä Board said the cooperation should give customers new opportunities in packaging design and production efficiency while maintaining sustainability and premium-quality requirements. Looking ahead, the companies aim to support customers in developing future-ready packaging solutions in a rapidly evolving market, especially as regulatory and performance requirements increase. Both parties highlighted that the combination of recyclable fresh-fibre paperboards and high-performance production technologies provides a strong platform for demanding packaging applications.

Rottneros - Q1 loss widens as lower pulp prices and weaker USD offset cost cuts

2026-05-07 │ P/TB 0.41 │ Market 5 │ Sector 3 │ URL

May 7, 2026 Rottneros reported Q1 2026 net sales of SEK 622m, down 5% from SEK 652m, as higher sales volumes were more than offset by lower market prices and a weaker USD versus SEK. The net price for NBSK in SEK was 23% lower year-on-year, while CTMP prices were relatively stable but negatively affected in SEK terms by the stronger krona. Production volume declined to 81,300 tonnes from 85,800 tonnes, mainly due to cold winter weather affecting sulphate pulp production at Vallvik, while sold volumes increased to 89,900 tonnes from 82,600 tonnes, supported by good demand in Rottneros’ priority sulphate pulp niches despite continued weakness and low margins in CTMP. EBITDA was SEK -36m versus SEK -27m, as lower selling prices in SEK outweighed lower wood raw-material costs and lower fixed costs, while net profit was SEK -81m versus SEK -69m. Cash flow after investments improved to SEK -49m from SEK -165m, helped by sharply lower capex and reduced working capital, while net debt decreased to SEK 389m from SEK 558m and the equity ratio strengthened to 62%; the board proposes no dividend for 2025. Looking ahead, Rottneros said its focus remains on cash flow, cost efficiency and high production availability, while investment levels have been reduced after recent investment programmes. Management noted that wood prices continue to decline, down around 15% from the H1 2025 peak, with a positive earnings impact expected at roughly a one-quarter lag. The company also signed an amendment to its bank agreement in March, with temporary covenants running until the end of April 2027 that management considers achievable based on current key earnings drivers.

Universal Electronics - Leviticus Partners discloses 5.1% stake

2026-05-04 │ P/TB 0.44 │ Market 5 │ Sector 5 │ URL

May 4, 2026 Leviticus Partners LP filed a Schedule 13G disclosing beneficial ownership of 655,000 shares in Universal Electronics Inc., representing 5.1% of the company’s common stock. The filing event date was May 1, 2026, and Leviticus reported sole voting and sole dispositive power over all 655,000 shares, with no shared voting or dispositive power. The filing was made under Rule 13d-1(b), with Leviticus classified as an investment adviser, and included a certification that the shares were acquired and are held in the ordinary course of business and not for the purpose of changing or influencing control of Universal Electronics.

TrueBlue - Q1 revenue growth and cost discipline offset by continued net loss

2026-05-05 │ P/TB 0.78 │ Market 5 │ Sector 5 │ URL

May 5, 2026 TrueBlue reported Q1 2026 revenue of $399m, up 8% year-on-year, or 7% organically excluding $4m of inorganic revenue from the January 2025 HSP acquisition, with management citing continued expansion in skilled verticals, stabilizing demand trends and operational discipline. PeopleReady revenue increased to $225m from $189m, while PeopleManagement declined to $127m from $136m and PeopleSolutions increased slightly to $46m from $45m. The company’s net loss widened to $20m, or $0.66 per diluted share, from a loss of $14m, or $0.48 per diluted share, including a $4m non-cash goodwill impairment charge, while adjusted net loss was $12m, or $0.41 per diluted share, broadly in line with the prior-year adjusted loss of $0.40 per share. SG&A improved 8% to $87m from $95m, adjusted SG&A fell to $83m from $91m, and adjusted EBITDA improved modestly to $-3m from $-4m. At quarter-end, TrueBlue had $24m of cash, $74m of debt and $36m available on its borrowing base, giving total liquidity of $60m. Looking ahead, TrueBlue said it is providing forward-looking information in its quarterly earnings presentation, while management remains focused on top-line growth with enhanced profitability. The company said it is using an enhanced sales model and technology and operational efficiencies to strengthen its market position and support sustainable profitable growth.

TrueBlue - Removal of Preferred Stock Purchase Rights from NYSE listing

2026-05-07 │ P/TB 0.78 │ Market 5 │ Sector 5 │ URL

May 7, 2026, the New York Stock Exchange filed a Form 25 with the SEC to remove TrueBlue, Inc.’s Preferred Stock Purchase Rights from listing and registration under Section 12(b) of the Securities Exchange Act. The removal is being made under Rule 12d2-2(a)(4), as the entire class of securities was redeemed or expired on May 6, 2026, with all rights pertaining to the class extinguished. NYSE suspended the security on May 7, 2026, and intends to complete the removal from listing and registration at the opening of business on May 18, 2026.

TrueBlue - Invesco cuts ownership below 5%

2026-05-08 │ P/TB 0.78 │ Market 5 │ Sector 5 │ URL

May 8, 2026, Invesco Ltd. filed an amended Schedule 13G/A disclosing beneficial ownership of 49,598 shares of TrueBlue, Inc. common stock as of March 31, 2026, representing 0.2% of the class. Invesco reported sole voting power over 48,698 shares and sole dispositive power over 49,598 shares, with no shared voting or dispositive power. The filing indicates ownership of 5% or less of the class and states that the securities are held in the ordinary course of business, not for the purpose of changing or influencing control of the company.

Mercer International - German lenders waive 2026 leverage covenant and tighten facility terms

2026-05-07 │ P/TB 1.56 │ Market 5 │ Sector 3 │ URL

May 7, 2026, Mercer International disclosed that certain German subsidiaries entered into a waiver and consent letter with lenders under its €370.1m German revolving credit facility, waiving the requirement to maintain a leverage ratio below 3.50x for the first three quarters of 2026 until the calculation date on December 31, 2026. In exchange, the lenders imposed tighter conditions, including a €300m utilization cap while leverage exceeds 2.00x, a rolling 13-week average liquidity requirement of $30m, a €60m cap on 2026 capex without agent consent, incremental reporting and liquidity-forecast obligations, and restrictions on distributions to the parent until September 30, 2026, with limited permitted distributions of up to €15m subject to conditions. Certain loan parties must also provide security over assets with realizable value of at least 110% of the utilized facility amount, including receivables, inventory, bank accounts, intra-group loans and pledges over shares including Mercer Stendal GmbH. The waiver also broadens events of default to include non-compliance with the new terms, certain management changes, defaults under Mercer’s senior notes or other credit facilities, and any steps toward North American bankruptcy proceedings, while the interest margin was revised to 2.50–4.25% depending on leverage.

Mercer International - Reports weaker Q1 results and outlines liquidity actions

2026-05-07 │ P/TB 1.56 │ Market 5 │ Sector 3 │ URL

May 7, 2026, Mercer International reported Q1 2026 revenues of $489.3m, down 3% year-on-year, Operating EBITDA of $7.8m versus $47.1m a year earlier, and a net loss of $52.0m, or $0.78 per share, compared with a $22.3m loss, or $0.33 per share, in Q1 2025. The weaker result was driven mainly by lower pulp sales realizations, higher fiber costs, adverse FX from a weaker dollar, and a $22.0m non-cash impairment of pulp and fiber inventories, partly offset by lower maintenance costs. Pulp segment EBITDA fell to $6.9m from $49.9m, while solid wood EBITDA was negative $5.6m versus negative $0.3m, reflecting high fiber costs despite higher revenues in most solid wood product categories. Liquidity at quarter-end was about $229.0m, including $84.5m of cash, after reflecting the waiver and reduced borrowing capacity under the German revolving credit facility. Looking ahead, Mercer expects modestly higher softwood pulp prices in Q2, relatively steady hardwood pricing, stable European lumber prices and modestly higher U.S. lumber prices, while fiber costs are expected to stabilize. Management said it expects pulp markets to become more balanced in the second half of 2026, remains on track to deliver its $100m “One Goal One Hundred” cost-savings target by year-end, and expects to regain compliance with the German facility leverage ratio by Q4 2026 while evaluating strategic alternatives and financing options to improve liquidity and the capital structure.

Tronox - Reports Q1 revenue growth but continued losses amid cost and pricing pressure

2026-05-06 │ P/TB 1.04 │ Market 5 │ Sector N/A │ URL

May 6, 2026, Tronox reported Q1 2026 revenue of $760m, up 3% year-on-year and 4% sequentially, driven by higher TiO2 and zircon volumes and favorable FX, partly offset by lower average selling prices and weaker other-product volumes. Net loss attributable to Tronox was $103m, or $0.65 per diluted share, compared with a $111m loss, or $0.70 per share, a year earlier, while adjusted EBITDA fell 45% year-on-year to $62m, with an 8.2% margin, as lower pricing, unfavorable FX, higher freight and production costs more than offset volume growth and lower corporate costs. TiO2 revenue rose 5% to $616m on 5% volume growth, while zircon revenue increased 29% to $89m on a 57% volume increase, although zircon pricing/mix was down 28%. The company ended the quarter with $406m of available liquidity, $3.2bn of net debt and net leverage of 11.1x, while free cash flow was negative $135m, reflecting operating cash use and $67m of capex. Looking ahead, Tronox expects Q2 TiO2 volumes to rise sequentially in the high-single-digit range, zircon volumes to moderate slightly, and both TiO2 and zircon prices to improve by a mid-single-digit percentage due to price increases and cost-related surcharges. Q2 adjusted EBITDA is guided at $65–85m, and the company expects positive Q2 free cash flow to largely offset Q1 cash use, with meaningful positive free cash flow still expected for full-year 2026.

Resources Connection - Announces planned board transition and governance updates

2026-05-05 │ P/TB 1.07 │ Market 5 │ Sector 5 │ URL

May 5, 2026, Resources Connection announced that A. Robert Pisano and Robert Kistinger will retire from the company’s board of directors immediately before the 2026 annual meeting of stockholders, with both directors remaining on the board until that meeting and Pisano continuing as chair until then. The company said the retirements were not related to any disagreement with Resources Connection regarding its operations, policies or practices. The board appointed CEO Roger Carlile to become chair upon Pisano’s retirement, while Susan Collyns will become lead independent director effective at the 2026 annual meeting. Following the two retirements, the board will be reduced to six directors. Separately, the board revised its director compensation policy on April 23, 2026, cutting the annual retainer for a non-employee board chair by 50% to $125,000 from $250,000, though Carlile will not receive the chair retainer because he is employed by the company.

Valhi - Q1 earnings decline as Chemicals segment profitability weakens

2026-05-07 │ P/TB 0.64 │ Market 5 │ Sector N/A │ URL

May 7, 2026, Valhi reported Q1 2026 net income attributable to stockholders of $2.0m, or $0.07 per share, down from $16.9m, or $0.59 per share, in Q1 2025, as weaker operating results in the Chemicals segment more than offset improved performance in Component Products and Real Estate Management and Development. Total net sales increased to $560.1m from $538.6m, mainly driven by the Chemicals segment, where sales rose 4% to $509.8m due to higher North American, Latin American and export volumes and favorable FX, partly offset by lower European volumes and lower average TiO2 selling prices. Chemicals operating income fell to $14.5m from $41.2m, reflecting lower TiO2 prices, lower production volumes and adverse FX, partly offset by higher sales volumes and lower production costs from cost-reduction initiatives implemented in Q4 2025. Component Products operating income increased to $7.1m from $5.9m on a more favorable security products mix and higher marine components sales, while Real Estate operating income rose to $11.3m from $3.0m, supported by the $7.3m sale of a final commercial parcel and a $5.4m tax increment infrastructure reimbursement. The quarter also included $2.0m of income tax expense related to an uncertain tax position from a German tax audit.

Unifi - Q3 profitability improves despite lower sales

2026-05-05 │ P/TB 0.35 │ Market 5 │ Sector N/A │ URL

May 5, 2026, Unifi reported fiscal Q3 2026 net sales of $130.0m, down 11.3% year-on-year but up 7.1% sequentially, as lower customer ordering linked to geopolitical, trade and tariff-related uncertainty continued to weigh on demand. Gross profit improved sharply to $9.1m, or a 7.0% margin, from a gross loss of $0.4m a year earlier, mainly driven by multi-year cost-reduction actions in the Americas segment, while SG&A fell 9.0% to $11.2m. Net loss narrowed to $2.3m, or $0.12 per share, from $16.8m, or $0.92 per share, in the prior-year period, while adjusted EBITDA improved to $4.0m from negative $4.9m. Operating cash flow was $8.0m in the quarter and $24.4m for the first nine months of fiscal 2026, while net debt declined to $68.4m from $85.3m at fiscal year-end. Looking ahead, Unifi said it will continue to leverage its improved cost base, invest in innovation and manage the balance sheet strategically, with Q4 results expected to include price increases tied to petrochemical-related inflation. Management said it is encouraged by business momentum, including traction in its beyond-apparel business, but also expects higher working capital needs to support demand and inflation.

PLAYSTUDIOS - Transfers Nasdaq listing and receives second bid-price compliance period

2026-05-05 │ P/TB 0.59 │ Market 5 │ Sector 3 │ URL

May 5, 2026, PLAYSTUDIOS disclosed that Nasdaq approved the transfer of the company’s Class A common stock and publicly traded warrants from the Nasdaq Global Market to the Nasdaq Capital Market, effective at the opening of trading on May 6, 2026, with the securities continuing to trade under the symbols MYPS and MYPSW. The transfer follows a November 2025 Nasdaq notice that the company was not in compliance with the $1.00 minimum bid price requirement, after its common stock had closed below $1.00 for 30 consecutive business days, and the company did not regain compliance during the initial 180-day period that expired on May 4, 2026. As a result of the transfer, Nasdaq granted PLAYSTUDIOS a second 180-day compliance period, expiring November 2, 2026, during which the stock must close at or above $1.00 for at least ten consecutive business days to regain compliance. The company said it will continue to monitor the share price and consider available options, including a reverse stock split if necessary, which would need to be completed at least ten business days before the deadline to allow Nasdaq to verify compliance.

Natural Alternatives - Expands TriBsyn applications across functional nutrition categories

2026-05-04 │ P/TB 0.25 │ Market 5 │ Sector 5 │ URL

May 4, 2026, Natural Alternatives announced expanded market applications for TriBsyn, its clinically supported carnosine booster, across beverage, dairy and medical nutrition categories. The company said TriBsyn is designed to deliver the benefits of beta-alanine for daily wellness without the paresthesia commonly associated with traditional forms, enabling effective dosing in consumer-friendly formats. The ingredient is now positioned for use in ready-to-drink beverages, protein drinks, dairy-based products, gummies and medical nutrition applications, allowing brand partners to develop products beyond traditional supplements. NAI said TriBsyn supports wellness benefits including healthy aging, sustained energy, cognitive function and cardiovascular health, making it suitable for both active lifestyle and general wellness positioning. The company added that the broader CarnoSyn portfolio is backed by more than 55 clinical studies and remains the only beta-alanine with New Dietary Ingredient status, with TriBsyn available to brand partners globally.

Chicago Rivet & Machine - Reports Q1 loss as sales decline

2026-05-08 │ P/TB 0.58 │ Market 5 │ Sector N/A │ URL

May 8, 2026, Chicago Rivet & Machine reported Q1 2026 net sales of $6.9m, down 5.4% from $7.2m in Q1 2025. The company posted a pre-tax loss of $0.4m compared with pre-tax income of $0.4m a year earlier. Net loss was $0.4m, or $0.37 per share, versus net income of $0.4m, or $0.42 per share, in the prior-year quarter.

Key Tronic - Q3 revenue declines but operating efficiency improves

2026-05-05 │ P/TB 0.32 │ Market 5 │ Sector 5 │ URL

May 5, 2026, Key Tronic reported fiscal Q3 2026 revenue of $89.6m, down from $112.0m a year earlier, mainly due to lower demand from a legacy customer, an end-of-life program transition and temporary site closures caused by Winter Storm Fern. Gross margin improved to 8.0% from 7.7%, and operating margin improved slightly to negative 0.3% from negative 0.4%, reflecting the benefit of cost-cutting actions despite lower sales. Net loss widened to $2.6m, or $0.24 per share, from $0.6m, or $0.06 per share, while adjusted net loss was $2.8m, or $0.26 per share, compared with adjusted net income of $0.1m, or $0.01 per share, in the prior-year quarter. For the first nine months of fiscal 2026, revenue fell to $284.6m from $357.4m, while operating cash flow remained broadly stable at about $10.0m, supporting a $14.3m year-on-year reduction in debt. Looking ahead, Key Tronic expects revenue growth in Q4 from higher demand among legacy customers and new program launches, and expects to return to profitability in the quarter. The company did not issue formal Q4 revenue or earnings guidance due to uncertainty around new program ramp timing and macroeconomic conditions, but said its China manufacturing wind-down should be completed by fiscal year-end and save about $1.2m per quarter thereafter.

AdvanSix - Q1 sales rise but earnings turn negative on cost headwinds

2026-05-07 │ P/TB 0.76 │ Market 5 │ Sector 5 │ URL

May 7, 2026, AdvanSix reported Q1 2026 sales of $404.2m, up 7% year-on-year, driven by 6% volume growth and 1% favorable pricing, with strength in Chemical Intermediates volumes and improved Plant Nutrients pricing offsetting weaker raw-material pass-through pricing. Despite the sales growth, the company posted a net loss of $15.5m, or $0.58 per share, compared with net income of $23.3m, or $0.86 per share, in Q1 2025, while adjusted EBITDA fell to $4.8m from $51.6m and adjusted EPS was negative $0.50. The decline reflected the absence of a $26m prior-year insurance benefit, higher sulfur and natural gas costs, higher plant and utility costs, and an $11m winter storm impact. Operating cash flow was negative $15.3m and free cash flow was negative $51.3m, including $35.9m of capex. Looking ahead, AdvanSix expects balanced U.S. ammonium sulfate supply-demand conditions during the domestic planting season, acetone spreads near cycle averages for 2026, and continued optimization of Nylon Solutions in a soft industrial market. The company maintained 2026 capex guidance of $75–95m, now expects plant turnaround pre-tax impact of $17–22m, and is evaluating a DEF growth project at its Hopewell ammonia platform, with a final investment decision targeted for H1 2027 and potential start-up in 2029.

AdvanSix - Assesses Hopewell ammonia expansion for DEF market

2026-05-06 │ P/TB 0.76 │ Market 5 │ Sector 5 │ URL

May 6, 2026, AdvanSix announced that it has entered into a process design and licensing agreement to assess an expansion of its integrated ammonia platform at its Hopewell, Virginia site to enable domestic production of Diesel Exhaust Fluid, or DEF. The company said DEF demand is growing, particularly from Class 8 vehicle usage in the Mid-Atlantic and Northeast U.S., and that the Hopewell site is well positioned because it already produces the required inputs: carbon dioxide, ammonia and high-purity water. The potential project would add a urea melt plant using Stamicarbon’s NX STAMI Urea technology, integrated with a DEF production unit designed to convert all urea melt into DEF, while maintaining the site’s commitment to ammonium sulfate fertilizer production. AdvanSix said the project would broaden its ammonia platform into adjacent products and support a more reliable domestic DEF supply in a market currently served partly by other regions and imports. Looking ahead, the project will move through detailed engineering and development before a final investment decision targeted for H1 2027. AdvanSix expects a multi-year capital investment with potential DEF plant start-up in 2029, subject to engineering, commercial and financial milestones as well as regulatory approvals.

Bowim - Preliminary Q1 profit improves despite lower sales

2026-05-06 │ P/TB 0.45 │ Market 5 │ Sector 5 │ URL

May 6, 2026, Bowim reported preliminary standalone Q1 2026 net sales revenue of PLN 401.2m, down PLN 30.0m year-on-year. Despite the sales decline, standalone operating profit increased by PLN 10.8m to PLN 14.5m, while standalone net profit improved by PLN 10.9m to PLN 9.3m. The company attributed the stronger profitability to stabilizing steel demand, a gradual rebound in steel prices after a prolonged correction, optimized purchasing and operating costs, and a more favorable regulatory and trade environment. Bowim specifically cited the transition of CBAM into its 2026 phase and expected tightening of EU safeguard measures for steel products as supportive factors. Looking ahead, the company said the market remains volatile, especially regarding energy costs and the pace of demand recovery in steel-consuming sectors such as construction and automotive. However, Bowim expects a gradual improvement in economic activity and EU regulatory and trade conditions to support stable sales volumes and pricing, while remaining cautious on geopolitical risks.

Lena Lighting - Supervisory Board recommends approval of 2025 reports and dividend

2026-05-07 │ P/TB 0.51 │ Market 5 │ Sector N/A │ URL

May 7, 2026. The board reviewed and accepted the standalone and consolidated 2025 financial statements and management reports, stating that they were consistent with the company’s books, documents and actual position, as confirmed by the auditor, B-think Audit. The board noted that Lena Lighting generated 2025 net profit of PLN 1.8m versus PLN 2.3m in 2024, with net margin of 1.28% versus 1.70%, while domestic sales grew 17.33% and foreign sales fell 13.53%, including a 17.51% decline in the EU and 5.90% growth outside the EU. The board supported management’s proposal to pay a dividend of PLN 0.10 per share, or PLN 2.5m in total, using the full 2025 profit and PLN 0.7m from supplementary capital, and said this should not threaten financial stability or investment plans. Looking ahead, management targets revenue and profit growth in 2026 through higher marketing activity, sales team development, new products and continued investment in production technologies, although it expects risks from geopolitical uncertainty, weak European growth, Middle East tensions, climate-related challenges and potential pressure on supply chains and input costs. The Supervisory Board concluded that Lena Lighting’s financial position is safe, liquidity is not threatened, and the company’s investment and marketing actions support its long-term growth and market diversification objectives.

The writer may own shares of the companies mentioned. This communication is for informational purposes only. AI helped us with this. Check important info.