The Deep Value Week – 2026/11

$HURC, $MYPS, $CRMT, $VHI, $KRO, $UEIC

Companies mentioned:

· Hurco Companies – Shareholders Approve Board, Executive Pay, and Auditor at Annual Meeting

· PLAYSTUDIOS, Inc. - Q4 and FY2025 Results, Reorganization, and Cost Reduction Plan

· America’s Car-Mart - Q3 FY2026 Results Highlight Lower Volumes Amid Funding Transition

· Valhi, Inc. - Q4 2025 Loss Driven by Chemicals Segment Weakness and Non-Cash Charges

· Kronos Worldwide - Q4 2025 Results Reflect Higher Loss on Lower TiO₂ Prices and Production Curtailments

· Universal Electronics - Q4 and FY2025 Results Show Margin Improvement, Cost Cuts, and 2026 EPS Outlook

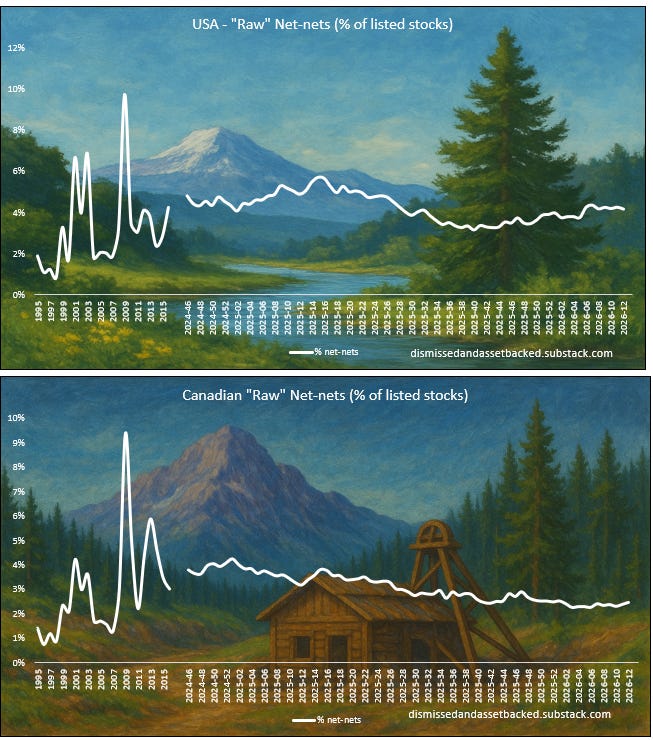

“Graham’s Geiger counter”

Benjamin Graham suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive. Today’s net-nets, however, are not the same as Graham’s net-nets. Many are un-investable being Chinese RTO’s, loss-making biopharma’s etc. But we do think it is interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable.

Hurco Companies – Shareholders Approve Board, Executive Pay, and Auditor at Annual Meeting

2026-03-12 │ P/TB 0.52 │

March 12, 2026 – Hurco Companies held its Annual Meeting of Shareholders, where investors elected all eight nominated directors to serve until the next annual meeting. The elected board members include Michael Doar, Cynthia Dubin, Timothy J. Gardner, Lawrence G. Keyler, Richard Porter, Benjamin Rashleger, Janaki Sivanesan, and Gregory S. Volovic. Shareholders also approved, on an advisory basis, the compensation of the company’s named executive officers as outlined in the proxy statement. In addition, investors ratified the appointment of Deloitte & Touche LLP as the company’s independent registered public accounting firm for the fiscal year ending October 31, 2026.

PLAYSTUDIOS, Inc. - Q4 and FY2025 Results, Reorganization, and Cost Reduction Plan

2026-03-16 │ P/TB 0.59 │ URL

March 16, 2026 – PLAYSTUDIOS reported fourth-quarter 2025 revenue of $55.4m, down from $67.8m a year earlier, with net loss improving to $13.7m from $22.4m, while consolidated AEBITDA declined to $5.1m from $12.5m as pressure continued across its legacy social casino portfolio. For full-year 2025, revenue fell to $235.1m from $289.4m, net loss was broadly unchanged at $28.6m, and consolidated AEBITDA decreased to $35.6m from $56.5m. Operating metrics also weakened, with DAU and MAU down materially, although ARPDAU improved and direct-to-consumer revenue rose strongly to $8.3m in Q4 and $27.6m for the full year, reflecting continued traction in the DTC channel. The company said it is reshaping the business around cost efficiency and future growth drivers, including Tetris Block Party and playSWEEPS, and on March 10 initiated a reorganization plan that will reduce its global workforce by about 27%, close 4 of 9 studios, and is expected to generate an additional $33.0m to $39.0m of annualized savings, on top of the prior Reinvention program’s $29.0m of annualized savings. The company expects to incur roughly $4.5m to $7.0m of restructuring-related charges, substantially in Q1 2026. As for outlook, PLAYSTUDIOS said it is not providing formal financial guidance at this time given ongoing weakness in the legacy portfolio and the early-stage nature of newer initiatives. Management highlighted late Q2 2026 as the target for POP! Slots sweepstakes integration and said it remains encouraged by early traction in The Win Zone and Tetris Block Party, while continuing to update investors as execution progresses.

America’s Car-Mart - Q3 FY2026 Results Highlight Lower Volumes Amid Funding Transition

2026-01-31 │ P/TB 0.23 │ URL

January 31, 2026 – America’s Car-Mart reported third-quarter fiscal 2026 results showing a sharp decline in sales volumes, with retail units sold down 22.1% to 10,275, as reduced origination capacity tied to the company’s ongoing capital structure transition, a smaller store base, and severe weather in the South-Central U.S. weighed on performance. Total revenue fell 12.0% to $286.8m, although interest income rose 3.1% to $64.2m, while gross profit per unit improved 8.8% to $7,762 and gross margin remained stable at 35.8%. The company posted a net loss attributable to common shareholders of $76.7m, or $9.25 per share, largely driven by a $47.0m non-cash valuation allowance against deferred tax assets, while adjusted loss per share was $1.53. Credit metrics were mixed, with net charge-offs rising to 6.5% of average finance receivables and 30+ day delinquencies increasing to 4.4%, though collections improved and management said customer demand remains robust. Car-Mart also highlighted progress on its capital structure transition, including a $300m term loan completed in October 2025 and a $161.3m ABS securitization completed in December 2025, while cash including restricted cash increased to $237.0m at quarter-end. Looking ahead, management said restoring origination capacity remains the key priority and depends on securing an additional financing source, such as further securitizations or a warehouse facility. The company said sales volumes are not reflective of underlying demand and expects its ability to restore growth to improve meaningfully once the capital structure strategy is completed, while SG&A savings from completed store consolidations should begin to be reflected from Q4 FY2026.

Valhi, Inc. - Q4 2025 Loss Driven by Chemicals Segment Weakness and Non-Cash Charges

2026-03-10 │ P/TB 0.61 │ URL

March 10, 2026 – Valhi reported a net loss attributable to stockholders of $53.2m, or $1.86 per share, in the fourth quarter of 2025, compared with net income of $22.8m, or $0.80 per share, a year earlier, while full-year 2025 swung to a net loss of $57.6m, or $2.02 per share, from net income of $108.0m in 2024. The deterioration was driven primarily by significantly weaker results in the Chemicals segment, where Q4 operating income fell to a loss of $60.1m from a profit of $32.6m, reflecting lower TiO2 selling prices, sharply reduced production rates, around $54m of unabsorbed fixed production and other manufacturing costs tied to curtailments, and about $10.3m of workforce reduction costs. Chemicals sales were broadly flat in Q4 at $418.3m and down 1% for the full year at $1.86bn, with lower pricing partly offset by volume gains and FX support, while Component Products improved with higher full-year sales and operating income, and Real Estate delivered stronger Q4 sales and operating profit helped by parcel closings and infrastructure reimbursements. Reported results were also affected by several non-cash items, including deferred tax charges tied to German tax assets and tax rate changes, a pension settlement loss of $28.7m in Q4, and prior-year gains from an environmental remediation settlement and the LPC transaction that created a tougher comparison base. On outlook, management did not provide formal guidance, but said forward results will depend on factors including TiO2 supply-demand conditions, pricing, production rates, raw material and energy costs, cost savings execution, global economic conditions, tariffs, FX, liquidity, and regulatory and litigation developments. The company also highlighted its focus on realizing strategic and operational cost savings and integrating prior acquisitions while navigating continued cyclical pressure in the chemicals business.

Kronos Worldwide - Q4 2025 Results Reflect Higher Loss on Lower TiO₂ Prices and Production Curtailments

2026-03-09 │ P/TB 0.79 │ URL

March 9, 2026 – Kronos Worldwide reported a net loss of $82.8m, or $0.72 per share, in the fourth quarter of 2025, compared with a net loss of $13.2m, or $0.12 per share, in the same period of 2024, while full-year 2025 results swung to a net loss of $110.9m, or $0.96 per share, from net income of $86.2m in 2024. Net sales declined slightly to $418.3m in Q4 and $1.86bn for the full year, primarily due to lower average TiO₂ selling prices, partially offset by higher sales volumes and favorable currency movements. The company’s TiO₂ segment recorded a loss of $59.4m in Q4 compared with a profit of $33.1m a year earlier, driven by reduced production rates that led to significant unabsorbed fixed production costs, lower pricing, and about $10.3m in workforce reduction costs. Production utilization averaged 77% in 2025 compared with 96% in 2024, reflecting curtailments implemented across facilities. Results also included non-cash tax charges related to German deferred tax assets and pension-related settlement losses, while prior-year comparables benefited from a gain tied to the Louisiana Pigment Company acquisition. On outlook, management did not provide formal guidance but noted that future performance will depend on factors including global TiO₂ supply and demand, pricing trends, raw material and energy costs, production rates, global economic conditions, tariffs, and currency movements, as well as the company’s ability to realize cost savings and maintain liquidity.

Universal Electronics - Q4 and FY2025 Results Show Margin Improvement, Cost Cuts, and 2026 EPS Outlook

2026-03-12 │ P/TB 0.43 │ URL

March 12, 2026 – Universal Electronics reported fourth-quarter 2025 net sales of $87.7m, down from $110.5m a year earlier, as both Home Entertainment and Connected Home revenues declined, but profitability improved on tighter cost control and better mix, with GAAP gross margin rising to 29.7% from 28.4% and GAAP operating income improving to $0.9m from a $4.4m loss. GAAP net loss narrowed to $1.1m, or $0.08 per share, from $4.5m, while adjusted non-GAAP net income was $2.3m, or $0.17 per diluted share, versus $2.6m last year. For full-year 2025, revenue declined to $368.3m from $394.9m, but operating performance improved materially as GAAP operating loss narrowed to $6.4m from $15.3m and adjusted non-GAAP operating income rose to $6.3m from $2.2m, delivering the company’s first profitable year since 2022 on a non-GAAP basis. Cash flow from operations was $23.6m for the year, cash ended at $32.3m, and UEI repurchased 765,201 shares in Q4 under its buyback plan, with the board also authorizing up to 1 million additional shares on March 11, 2026. On outlook, management said fiscal 2026 revenue is expected to decline year over year as Home Entertainment faces secular headwinds and Connected Home has not yet reached an inflection point. The company plans further cost reductions and working capital actions to improve profits and cash generation, and guided for adjusted non-GAAP diluted EPS of $0.45 to $0.65 in fiscal 2026 versus $0.31 in fiscal 2025.

The writer may own shares of the companies mentioned. This communication is for informational purposes only. AI helped us with this. Check important info.